|

市場調査レポート

商品コード

1939092

アフリカの作物保護化学品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Africa Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの作物保護化学品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

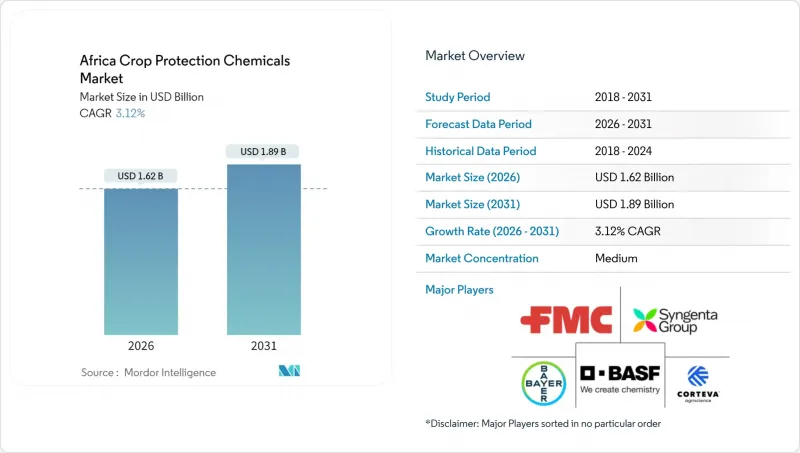

アフリカの作物保護化学品市場は、2025年の15億7,000万米ドルから2026年には16億2,000万米ドルへ成長し、2026年から2031年にかけてCAGR3.12%で推移し、2031年までに18億9,000万米ドルに達すると予測されています。

現在の成長は、害虫発生を増加させる気候変動圧力の高まり、政府による投入資材補助金の増加、小規模農家向けモバイル金融技術(フィンテック)アクセスの改善、ならびに南部・東部回廊地域における農業の着実な商業化に支えられています。秋軍虫被害の深刻化、サプライチェーンのデジタル化、バイオテクノロジー承認の進展により、製品構成はプレミアムでより選択性の高い有効成分へと再編されつつあります。一方、各国規制のばらつきや輸送コストの変動によりサービス提供コストが上昇しているため、供給業者は地域生産やパートナー主導の流通モデルを模索しています。競合の激しさは依然として中程度であり、現地の専門企業が偽造品対策、生物農薬の統合、ラストマイルにおける助言の不足といった課題に取り組む余地が残されています。

アフリカの作物保護化学品市場動向と洞察

気候変動による発生増加で害虫圧迫が深刻化

気候変動による害虫の分布域拡大と繁殖サイクルの延長秋軍虫(フォールアーミーワーム)だけで年間最大2,000万トンのトウモロコシが被害を受け、これは1億人分の食糧に相当します。農家では頻繁な葉面散布と高付加価値の全身性殺虫剤で対応しています。東アフリカにおけるサバクトビバッタの復活は季節的な変動性を増幅させています。生物的防除インフラが限られているため、総合的害虫管理(IPM)の要請に沿った選択的化学農薬への需要が高まっています。気温上昇によりライフサイクルが短縮され、散布のタイミングが狭まる中、予測的な害虫調査ツールや、対象外への飛散を最小限に抑える精密ノズルへの投資が促進されています。

投入強化プログラムに対する政府補助金

ナイジェリアの「アンカー・ボロワーズ・プログラム」やケニアの肥料補助金制度では、農薬を種子・肥料とセット化することで供給業者に確実な販売量を保証しています。バウチャーや電子財布による支払いは信用リスクを低減し、流通網の拡大と早期の在庫確保を促進します。財政制約やドナー依存により購入パターンは不安定ながら、短期的な需要急増をもたらします。補助金を農業普及指導と組み合わせたプログラムでは返済率が向上し、化学農薬の再購入を正当化する収量増加が強化されます。政府調達リストに製品を事前登録した供給業者は、これらの大量流通チャネルへの優先アクセス権を獲得します。

高毒性有効成分に対する厳格な地域規制

ケニア農業食品庁は2024年、違法農薬340万ケニアシリング(約2万6,000米ドル相当)を押収しました。南アフリカの規制当局は現在、環境アセスメントの拡充を義務付けており、新規登録の所要期間が最大18カ月延長されています。西アフリカ諸国経済共同体(ECOWAS)の農薬調和化草案では、30種類以上の有効成分を段階的に廃止する計画です。再配合により調査コストが増加し、特にニッチな害虫を対象とする低分子化合物の製品ポートフォリオが縮小します。低毒性代替品が容易に入手できない、あるいは手頃な価格でない場合、移行期間中の収量減少リスクが生じます。

セグメント分析

2025年、殺虫剤はアフリカの作物保護化学品市場シェアの39.50%を占めました。これは西・東アフリカでトウモロコシやソルガムを脅かすアオムシの深刻な被害が要因です。殺虫剤市場規模は着実に拡大する見込みですが、遺伝子組み換え害虫抵抗性作物の普及に伴い相対的シェアは低下すると予測されます。除草剤は2031年までCAGR3.55%と最も高い伸びを示します。これは商業農場における低耕起栽培や除草剤耐性品種の採用が背景にあります。殺菌剤は輸出志向型園芸分野で依然として重要であり、残留基準値遵守のため精密な散布計画と高品質有効成分が求められます。線虫防除剤などのニッチ分野は、線虫による収量損失が12%に迫る根菜・塊茎生産地で需要が高まっています。

バイオテクノロジーは完全な代替ではなく、微妙な変化をもたらします。TELAトウモロコシの承認により、季節ごとの殺虫剤散布回数は最大3回削減されましたが、より均一な生育状態を保護するため除草剤の使用量は増加しています。供給業者はこれに対応し、発芽前除草剤と生物学的種子コーティングを統合した複合パックを提供しています。デジタルスカウティングプラットフォームへの投資により、閾値に基づく殺虫剤散布が可能となり、管理ガイドラインに沿った運用が実現します。最終的には、耐性発生を遅らせ将来の規制基準に適合する、二重または多重作用機序を持つ分子を軸とした製品ポートフォリオへの移行が進みます。

アフリカの作物保護化学品市場レポートは、機能別(殺菌剤、除草剤、殺虫剤など)、適用方法(化学灌漑、葉面散布、燻蒸など)、作物タイプ(商業作物、果実・野菜、穀物・シリアル、豆類・油糧種子、芝生・観賞植物)、地域(南アフリカ、その他のアフリカ諸国)で構成されています。市場予測は金額(米ドル)と数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリーおよび主要な調査結果

第4章 主要な業界動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制枠組み

- 南アフリカ

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 気候変動による発生増加に伴う害虫圧力の増大

- 投入集約化プログラムに対する政府補助金

- 除草剤耐性作物品種の急速な普及

- 南部・東部アフリカにおける商業農業クラスターの拡大

- EUのMRL改定による輸出業者の高品質農薬への移行

- モバイル農業資材フィンテックプラットフォームによる資材アクセスの改善

- 市場抑制要因

- 高毒性農薬成分に対する厳格な地域規制

- 害虫・雑草の耐性化が加速

- 偽造農薬の蔓延

- 紅海・スエズ運河の輸送不安定化による輸入コスト上昇

第5章 市場規模と成長予測(金額および数量)

- 機能

- 殺菌剤

- 除草剤

- 殺虫剤

- 軟体動物駆除剤

- 殺線虫剤

- 適用方法

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果樹・野菜

- 穀物・穀類

- 豆類・油糧種子

- 芝生および観賞植物

- 国別

- 南アフリカ

- その他アフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業概況

- 企業プロファイル

- Syngenta Group

- Bayer AG

- Corteva Agriscience

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- UPL Limited

- Wynca Group(Zhejiang Xinan Chemical Industrial Group Co., Ltd.)

- Koppert B.V.

- Andermatt Group AG

- Albaugh LLC

- Rotam Global AgroSciences Ltd.

- Bioceres Crop Solutions Corp.

- Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.