インドの作物保護化学品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

India Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 207 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685858

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

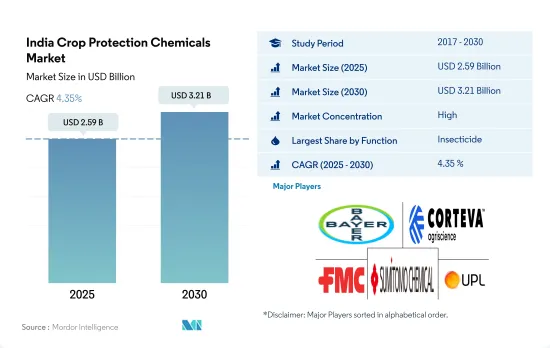

インドの作物保護化学品市場規模は2025年に25億9,000万米ドルと推定され、2030年には32億1,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは4.35%で成長すると予測されます。

殺虫剤市場は病害虫の増加によって牽引される

- インドの作物保護化学品市場は長年にわたり一貫した成長を遂げ、2022年の市場規模は23億米ドルに達します。人口増加、食糧需要の高まり、害虫、病気、雑草から作物を保護する必要性などの要因が原動力となっています。

- 最も使用されている作物保護化学物質は殺虫剤で、2022年の市場シェアは72.5%、次いで除草剤が13.4%、殺菌剤が8.9%です。これは、害虫がさまざまな種類の作物に与える経済的損害に起因しています。アブラムシ、オオヨコバイ、茎虫、アーミーワームは、インドの主要作物の生産に影響を与える主要な害虫です。

- 2022年における殺線虫剤のシェアは2.6%でした。現在の市場シェアは比較的低いが、植物寄生線虫はインドで年間21.3%の収量損失を引き起こすことが知られており、これは年間15億8,000万米ドルに相当し、同国で栽培される様々な経済的に重要な作物に影響を及ぼしているため、これらの農薬は市場成長の余地が大きいです。例えば、インドで最も栽培されているイネは根こぶ線虫Meloidogyne graminicolaの影響を受けやすく、年間2億9,610万米ドルの経済損失をもたらしています。

- 同様に、インドのコダグ州北部では、300エーカーに及ぶ約40~45の農園が軟体動物の侵入により大きな損失を被っています。しかし、コダグ州の農家は、主に軟体動物駆除剤を利用することで、蔓延を90%減少させることに成功しており、市場の成長につながる可能性があります。

- 国内における病害虫の発生率の増加や、農作物の生産性向上の必要性などの要因により、市場は予測期間中にCAGR 4.6%を記録すると推定・予測されます。

インドの作物保護化学品市場動向

主要作物における様々な病害虫による農作物損失の大幅な増加と、より高い生産性の必要性が、1ヘクタール当たりの農薬消費量に貢献

- インドの多様な気候は、農業部門がさまざまな作物を栽培するための好条件を生み出しています。しかし、多様な気候がもたらす恩恵の一方で、雑草、害虫、菌類による病害といった大きな課題にも直面しています。これらの課題により、年間作物の損失は大きく、雑草が45%、害虫が35%、菌類病が20%を占めています。

- これらの問題に対処するため、農家は農薬に頼ることが多くなりました。その結果、1ヘクタール当たりの農薬消費量全体にはあまり変化が見られないです。

- 雑草はインドの農業セクターに大きな脅威をもたらし、コメ、小麦、トウモロコシなどの主要作物で大きな損失をもたらしています。こうした損失を軽減するため、労働力不足と賃金上昇により手作業による除草がコスト高になったため、農家は除草剤に頼るようになっています。しかし、除草剤耐性の雑草の出現が問題となっており、ヘクタール当たりの除草剤散布量が増加する可能性があります。

- 殺虫剤のヘクタール当たりの消費量は、指定された期間中一定でした。殺虫剤は、カメムシ、ルーパー、アーミーワーム、アブラムシ、コナジラミなどの害虫による有害な影響と闘うことによって、作物生産を向上させる重要な手段として浮上してきました。これらの害虫は農業の収量に大きな脅威をもたらし、作物の大幅な損失につながります。これらの吸汁性害虫に対抗し、農作物の生産性を高めるため、農家は殺虫剤の使用に頼るようになっています。

- その他の要因として、農業活動の増加や農作物増産へのニーズが、国内の1ヘクタール当たりの殺虫剤消費量を増加させています。

農業部門と農村経済の改善に対する政府の支援が価格に及ぼす影響

- シペルメトリンは合成ピレスロイド系で、ノミ・カブトムシ、ハクビシン、ゴキブリ、シロアリ、テントウムシ、サソリ、イエロージャケットの駆除に使用されます。2022年の価格は2万1,000米ドル。インドでは、シペルメトリンはキャベツ、小麦、綿花、米、サトウキビ、ブリンジャール、ヒマワリ、オクラなど、指定された8種類の作物で使用するためにCIBRCによって登録されています。

- アトラジンは、インドのトウモロコシや稲作において、エキノクロア、エルシン属、アマランサスビリジスなどの広葉雑草やイネ科雑草の防除に広く使用されている除草剤です。この除草剤は2022年に1万3,500米ドルと評価されました。インドは世界最大のアトラジン技術輸入国であり、主に中国、イタリア、イスラエルから輸入しています。

- マラチオンは有機リン系殺虫剤です。2022年には1万2,500米ドルと評価されました。アブラムシ、アザミウマ、ダニ、ウロコ、ホウキムシ、ミミズ、リーフマイナー、ノミ、バッタ、虫、ウジなどの防除に使用されます。CIBRCのガイドラインでは、マラチオンはソルガム、エンドウ、ダイズ、ヒマシ、ヒマワリ、ビンディ、ブリンジャール、カリフラワー、ダイコン、カブ、トマト、リンゴ、マンゴー、ブドウにのみ使用が許されています。

- プロピネブは接触殺菌剤です。2022年には1トン当たり3,500米ドルと評価されました。リンゴ、ジャガイモ、チリ、トマトなどの作物で、かさぶたの初期病害や晩枯病、バッカイ腐敗病、べと病、果実斑点病、褐色斑点病、狭葉斑点病など、さまざまな病害の防除に使用されます。

- インド政府は、農村経済の復興と農家の収入増加に向けて、継続的に予算支援を行っています。22年度予算では、農業セクターと農村経済の改善に向けて、いくつかの施策や取り組みが提案・発表されました。これは、国内の作物保護化学品の価格にさらに影響を与えると思われます。

インドの作物保護化学品産業の概要

インドの作物保護化学品市場はかなり統合されており、上位5社で74.59%を占めています。この市場の主要企業は次のとおりです。 Bayer AG, Corteva Agriscience, FMC Corporation, Sumitomo Chemical and UPL Limited.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 除草剤

- 殺虫剤

- 軟体動物駆除剤

- 殺線虫剤

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Gharda Chemicals Ltd

- PI Industries

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 48615

The India Crop Protection Chemicals Market size is estimated at 2.59 billion USD in 2025, and is expected to reach 3.21 billion USD by 2030, growing at a CAGR of 4.35% during the forecast period (2025-2030).

The market for pesticides is driven by increasing pest and disease incidence

- The Indian crop protection chemicals market experienced consistent growth over the years, with a market value of USD 2.3 billion in 2022, driven by factors such as increasing population, rising food demand, and the need to protect crops from pests, diseases, and weeds.

- Insecticides are the most used crop protection chemicals, with a market share of 72.5% in 2022, followed by herbicides and fungicides, with a market share of 13.4% and 8.9%, respectively. This is attributed to the economic damage that insect pests can cause in a variety of crop types. Aphids, leafhoppers, stem borers, and armyworms are the dominant insect pests that affect the production of major crops in India.

- Nematicides accounted for a share of 2.6% in 2022. Although the current market share is relatively less, these pesticides have higher scope for market growth as plant parasitic nematodes are known to cause an annual yield loss of 21.3% in India, which amounts to USD 1.58 billion annually, affecting various economically important crops grown in the country. For instance, rice (the most grown crop in India) is susceptible to root-knot nematode, Meloidogyne graminicola,leading to annual economic losses of 296.1 million.

- Similarly, around 40-45 plantations spanning 300 acres of land in the northern parts of Kodagu, India, have suffered significant losses due to mollusk infestations. However, the farmers in Kodagu have achieved a 90% reduction in the infestation by primarily utilizing molluscicides, which may result in market growth.

- Due to factors like increasing pest and disease incidence in the country and the need for higher crop productivity, the market is estimated to register a CAGR of 4.6% during the forecast period.

India Crop Protection Chemicals Market Trends

A significant increase in crop losses by various pests and diseases in major crops and the need for higher production contributed to the per-hectare pesticide consumption

- India's diverse climate creates favorable conditions for the agricultural sector to cultivate a wide range of crops. However, alongside the benefits of climatic diversity, the sector also faces significant challenges from weeds, insect pests, and fungal diseases. These challenges have resulted in substantial annual crop losses, with weeds accounting for 45% of the losses, insects for 35%, and fungal diseases for 20%.

- In response to these issues, farmers have increasingly relied on pesticides as their primary tool to combat crop losses. As a result, there has been limited change in the overall consumption of pesticides per hectare.

- Weeds pose a significant threat to the Indian agricultural sector, resulting in substantial losses for major crops such as rice, wheat, and maize. To mitigate these losses, farmers have increasingly relied on herbicides as manual weeding has become costlier due to labor shortages and rising wages. However, the emergence of herbicide-resistant weeds has become a concerning issue, leading to a potential escalation in the application of herbicides per hectare.

- The per-hectare consumption of insecticides has remained constant over the specified period. Insecticides have emerged as vital tools in enhancing crop production by combating the detrimental impact of insect pests, including stink bugs, loopers, armyworms, aphids, and whiteflies. These pests pose significant threats to agricultural yields, leading to substantial crop losses. To counter these sucking insect pests and boost their crop productivity, farmers are increasingly relying on the use of insecticides.

- Other factors like increased agricultural activities and the need for higher crop production are increasing per-hectare pesticide consumption in the country.

Influence of Government support for the improvement of the agriculture sector and the rural economy on prices

- Cypermethrin is a synthetic pyrethroid used to control flea beetles, boxelder bugs, cockroaches, termites, ladybugs, scorpions, and yellow jackets. It was priced at USD 21.0 thousand in 2022. In India, cypermethrin is registered by CIBRC for use in eight specified crops, such as cabbage, wheat, cotton, rice, sugarcane, brinjal, sunflower, and okra.

- Atrazine is an herbicide widely used for control of broadleaf and grassy weeds like Echinocloa, Elusine spp., and Amaranthus viridis in maize and rice crops in India. The herbicide was valued at USD 13.5 thousand in 2022. India is the largest importer of Atrazine technical in the world and imports majorly from China, Italy, and Israel.

- Malathion is an organophosphate insecticide. It was valued at USD 12.5 thousand in 2022. It is used to control aphids, thrips, mites, scales, borers, worms, leaf miners, fleas, grasshoppers, bugs, and maggots. As per guidelines of CIBRC, malathion is permitted to be used only in sorghum, pea, soybean, castor, sunflower, bhindi, brinjal, cauliflower, radish, turnip, tomato, apple, mango, and grape crops.

- Propineb is a contact fungicide. It was valued at USD 3.5 thousand per metric ton in 2022. It is used to control various diseases like scab early and late blight dieback, buckeye rot, downy mildew, fruit spots, and brown and narrow leaf spot diseases in apple, potato, chili, and tomato crops.

- The Government of India has been continuously providing budgetary support toward reviving the rural economy and increasing the farmers' income. Several measures and initiatives were proposed and announced during the FY22 budget for the improvement of the agriculture sector and the rural economy. This will further influence the prices of crop protection chemicals in the country.

India Crop Protection Chemicals Industry Overview

The India Crop Protection Chemicals Market is fairly consolidated, with the top five companies occupying 74.59%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Sumitomo Chemical Co. Ltd and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Gharda Chemicals Ltd

- 6.4.7 PI Industries

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

インドの作物保護化学品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 207 Pages

- 納期

- 2~3営業日