|

市場調査レポート

商品コード

1683118

フランスの農薬保護化学品市場:市場シェア分析、産業動向、成長予測(2025~2030年)France Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスの農薬保護化学品市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 206 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

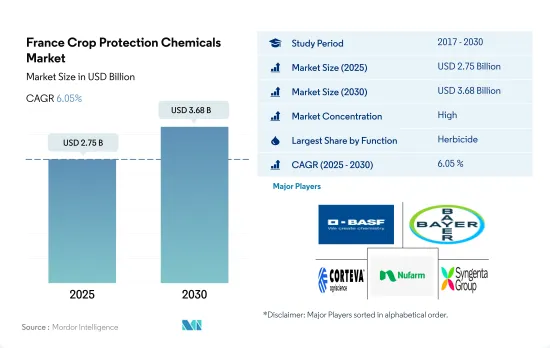

フランスの農薬保護化学品市場規模は2025年に27億5,000万米ドルと予測され、2030年には36億8,000万米ドルに達し、予測期間(2025~2030年)のCAGRは6.05%で成長すると予測されています。

フランスで除草剤の使用が増加している理由は、さまざまな社会的・経済的要因です。

- フランスは欧州の重要な農業国であり、さまざまな農産物の主要生産国・輸出国です。小麦、ライ麦、大麦、トウモロコシ、テンサイ、オート麦、果物、野菜(リンゴ、メロン、モモ、ネクタリン、トマト、カリフラワー、ニンジン、タマネギ、サラダ野菜など)が生産され、輸出されています。雑草、菌類病、害虫は農業セクターに大きな損失をもたらしています。農業従事者は、これらの課題と闘い、生産量を向上させるために、化学農薬保護化学品製品に依存しています。農薬保護化学品製品の全体的な消費量は、欧州で16.4%と第2位の市場シェアを占め、市場規模は23億2,000万米ドルでした。

- 2022年には、除草剤が農薬保護化学品消費量において最大の市場シェアを占め、総量の50.7%を占めました。この優位性は、フランスとその海外領土が合わせて約250種類の作物を生産していることに起因しています。農水省によると、フランスでは毎年平均して2万9,300トン以上の除草剤が使用されています。社会的、経済的な理由も、化学除草剤使用の増加の他の要因である可能性があります。グリホサートは国内で広く使用されている除草剤です。

- 殺菌剤と殺虫剤も除草剤に次いで大きなシェアを占めており、それぞれ28.5%と20.7%です。数多くの真菌性病害が主要作物に影響を及ぼしており、アブラムシなどの害虫がこれらの病害を作物からによる作物へと拡散させ、作物に大きな被害をもたらしています。

- 作物への蔓延の増加と生産性向上の必要性は、予測期間中にフランスの農薬保護化学品品市場をCAGR 5.8%で牽引する可能性があります。

フランスの農薬保護化学品製品市場の動向

国際的な需要と雑草を抑制する能力により、1ヘクタール当たりの除草剤の消費量は増加しています。

- フランスの農業セクターは、国家経済において非常に重要な位置を占めています。しかし、雑草、害虫、菌類感染といった形でかなりの課題に直面しており、その結果、作物の収量が毎年大幅に減少しています。こうした問題に対処するため、フランスでは2022年に農地1ヘクタール当たり平均4,800gの農薬保護化学品が使用されました。

- 除草剤は主要な化学農薬保護化学品カテゴリーとして浮上し、農業部門で広く使用されています。2022年の農地1ヘクタール当たりの除草剤平均消費量は2.2kgでした。しかし、遺伝子組み換え品種を含む除草剤耐性作物の採用や、雑草の成長を管理し収量損失を減らす必要性から、散布率や複数の除草剤の使用は増加しました。

- 殺菌剤は農業で広く使用されているため、農薬保護化学品消費量の第2位を占めています。国内の農地1ヘクタール当たりの殺菌剤の平均消費量は、2022年には2kgでした。気候環境の変化などの要因が、殺菌剤への依存度を高めています。真菌性病害の蔓延は、多様な種類の作物にとって大きな脅威となっており、収穫量の大幅な低下や収穫物の品質低下を引き起こしています。その結果、農業従事者はこれらの病害を防除するために殺菌剤に大きく依存しています。

- 害虫蔓延の増加と抵抗性を示す昆虫集団の出現は、これらの深刻化する害虫課題に対抗する殺虫剤の必要性に拍車をかけています。2022年、フランスの平均散布量は1ヘクタール当たり0.2kgでした。

グリホサートはフランスで最も使用されている農薬保護化学品で、2022年の価格は1トン当たり1,150米ドルでした。

- フランスは欧州で最も農薬保護化学品を消費する国のひとつであり、世界第3位の殺虫剤輸出国でもあります。同国は殺虫剤の大半をベルギー、オランダ、ブラジルに輸出しています。

- 最近フランスでは、特に殺虫剤において有効成分の価格が高騰しています。シペルメトリンとエマメクチン安息香酸エステルは、2022年にそれぞれ1トン当たり2万1,200米ドル、1万7,400米ドルと評価されました。これらの殺虫剤は2019~2022年の間に21.5%の大幅な価格上昇を経験しました。

- 2022年現在、メタラキシルの価格は1トン当たり4,500米ドルです。メタラキシルは真菌類に対して最も効果的な浸透性殺菌剤のひとつです。ピシウム菌やフィトフトラ菌の種子の腐敗や湿害を防除するため、土壌や種子の治療剤として広く使用されています。また、一年草や多年草のPhytophthora属の茎腐敗病やカンカ病の防除のための土壌処理剤としても使用され、特定のべと病に対しても有効です。

- グリホサートはフランスで最も広く使用されている農薬保護化学品です。2023年、スイスの化学グループであるSyngentaが製造したグリホサートを含む2種類の除草剤の販売が禁止されました。これは、同社がミツバチやその他の昆虫、土壌、水生生物への影響について義務付けられているリスクアセスメントを提出しなかったため、野生生物への害の可能性に関する分析が不十分であったためです。

- 選択的除草剤であるペンディメタリンは、穀類、トウモロコシ、イネでは出穂前に、豆類、綿花、大豆、落花生では播種前に浅く土壌に埋め込んで散布されます。野菜作物では、出穂前または移植前に散布します。注目すべきは、この除草剤の価格が2019年と比較して2022年には37.8%増の1トン当たり3,300米ドルと大幅に上昇したことです。

フランスの農薬保護化学品産業の概要

フランスの農薬保護化学品市場はかなり統合されており、上位5社で70.03%を占めています。この市場の主要企業は、 BASF SE、Bayer AG、Corteva Agriscience、Nufarm Ltd、Syngenta Groupがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬保護化学品消費量

- 有効成分の価格分析

- 規制の枠組み

- フランス

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション(市場規模(単位:米ドル、数量)、2030年までの予測、成長見込みの分析を含む)

- 機能

- 殺菌剤

- 除草剤

- 殺虫剤

- 殺軟体動物剤

- 殺線虫剤

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50670

The France Crop Protection Chemicals Market size is estimated at 2.75 billion USD in 2025, and is expected to reach 3.68 billion USD by 2030, growing at a CAGR of 6.05% during the forecast period (2025-2030).

Various social and economic factors are reasons for the increased use of herbicides in the country

- France is an important agricultural country in Europe and a major producer and exporter of various agricultural products. Wheat, rye, barley, corn, sugar beets, oats, fruits, and vegetables, including apples, melons, peaches, nectarines, tomatoes, cauliflowers, carrots, onions, and salad vegetables, are produced and exported. Weeds, fungal diseases, and insect pests pose significant losses to the agricultural sector. Farmers depend on chemical pesticide products to combat these challenges and enhance production quantities. The overall consumption of crop protection chemicals occupied the second-largest market share of 16.4% in Europe, with a market value of USD 2.32 billion.

- In 2022, herbicides held the largest market share in terms of pesticide consumption, accounting for 50.7% of the total volume. This dominance can be attributed to France and its overseas territories together producing around 250 varieties of crops. According to the Ministere de l'Agriculture et de l'Alimentation, every year, on average, the country utilizes more than 29,300 metric ton of herbicides. Social and economic reasons could be other factors for the increased use of chemical herbicide products. Glyphosate is a widely used herbicide in the country.

- Fungicides and insecticides also occupy the largest market shares after herbicides, i.e., 28.5% and 20.7%, respectively. Numerous fungal diseases are affecting major crops, and insect pests such as aphids are spreading these diseases from one crop to another, resulting in significant crop damage.

- The increasing crop infestations and the need for higher productivity may drive the French crop protection chemicals market at a CAGR of 5.8% during the forecast period.

France Crop Protection Chemicals Market Trends

The consumption of herbicides per hectare is increasing due to their international demand and their ability to control weeds

- The agricultural sector in France holds great importance within the nation's economy. However, it faces considerable challenges in the form of weeds, insect pests, and fungal infections, resulting in considerable annual reductions in crop yield. To address these issues, France used an average of 4.8 thousand g of crop protection chemicals per hectare of agricultural land in 2022.

- Herbicides emerged as the primary chemical pesticide category, experiencing widespread use in the agricultural sector. The average herbicide consumption per hectare of agricultural land stood at 2.2 kg in 2022. However, the application rates and the employment of multiple herbicides increased due to the adoption of herbicide-resistant crops, including genetically modified varieties, and the need to manage weed growth and reduce yield losses.

- Fungicides hold the second position in terms of pesticide consumption, as they are extensively used in the agricultural industry. The average consumption of fungicides per hectare of agricultural land in the country was 2 kg in 2022. Factors such as changing climatic circumstances have contributed to an escalated dependence on fungicides. The prevalence of fungal diseases presents a significant threat to diverse crop types, causing a substantial decline in yield and the compromised quality of harvested produce. As a result, farmers heavily depend on fungicides to control these diseases.

- The increasing prevalence of insect infestations and the emergence of insect populations displaying resistance have spurred the need for insecticides to counter these escalating pest challenges. In 2022, the mean application rate in France stood at 0.2 kg per hectare.

Glyphosate is the most used pesticide in France, and it was priced at USD 1.15 thousand per metric ton in 2022

- France is one of the highest pesticide-consuming countries in Europe and the third-largest exporter of insecticides globally. The country exports most of its insecticides to Belgium, the Netherlands, and Brazil.

- Recently, France witnessed an escalation in the prices of active ingredients, particularly in the case of insecticides. Cypermethrin and emamectin benzoate were valued at USD 21.2 thousand per metric ton and USD 17.4 thousand per metric ton in 2022, respectively. These insecticides experienced a significant price increase of 21.5% between 2019 and 2022.

- As of 2022, metalaxyl was priced at USD 4.5 thousand per metric ton. It is one of the most effective systemic fungicides against oomycetes. It is widely used as a soil or seed treatment to control Pythium and Phytophthora seed rot and damping-off. It also serves as a soil treatment for controlling Phytophthora stem rots and cankers in annuals and perennials and offers efficacy against certain downy mildews.

- Glyphosate retains its position as the most extensively used pesticide in France. In 2023, the country banned the sale of two weedkillers containing glyphosate produced by Swiss chemical group Syngenta due to a lack of analysis on the chemical's potential harm to wildlife, as the company did not submit the mandatory risk assessment on the impacts on bees, other insects, soil, and water life.

- Pendimethalin, a selective herbicide, is applied before emergence in cereals, maize, and rice and with shallow soil incorporation before seeding beans, cotton, soybeans, and groundnuts. In vegetable crops, it is applied before emergence or transplanting. Notably, the price of this herbicide saw a substantial increase of 37.8% to USD 3.3 thousand per metric ton in 2022 compared to 2019.

France Crop Protection Chemicals Industry Overview

The France Crop Protection Chemicals Market is fairly consolidated, with the top five companies occupying 70.03%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms