中国の農薬保護化学品市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 201 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683102

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

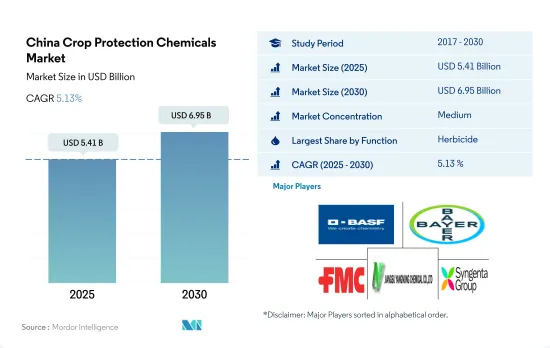

中国の農薬保護化学品市場規模は2025年に54億1,000万米ドルと推定され、2030年には69億5,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.13%で成長します。

除草剤が市場を席巻

- 中国は、多くの国で販売されている製剤化された農薬保護化学品や既製農薬保護化学品の基礎となる有効成分の主要生産国です。同国は、農薬保護化学品品の世界最大級の生産国であり、輸出国でもあります。殺虫剤は農薬保護化学品品市場の重要なセグメントを構成しています。市場の主要促進要因は、人口が多いこと、農地の規模が限られていること、食糧安全保障が高まっていること、効率的な農業生産が急務であることです。2022年のアジア太平洋農薬保護化学品品市場全体では、中国が金額ベースで20.8%と最も高いシェアを占めています。

- 2022年の中国の農薬保護化学品品市場では、除草剤が金額ベースで38.2%の最大シェアを占めました。中国では、除草剤の使用が雑草防除に役立っており、その結果、農業従事者は雑草と競合しにくい矮性稲品種をより多く栽培しやすくなり、収量が増加しています。農村部から工業地帯に移動した伝統的手作業労働者が大幅に減少している除草剤のおかげで農業従事者は雑草を防除できるようになりました。

- 2022年の市場では、殺虫剤セグメントが金額ベースで30.0%と大きなシェアを占めていました。綿花に使用登録されている農薬保護化学品で最も一般的なものは殺虫剤です。なかでもホキシムは、シペルメトリンやβ-シペルメトリンなどの活性物質の登録数が最も多いです。

- 病害虫の蔓延に対する懸念の高まりと国際的な需要の増加に伴い、企業や政府は継続的に研究プロジェクトに投資し、病害虫による作物被害を防ぐための新しい有効成分を開発しています。同市場は予測期間中にCAGR 5.4%を記録すると予測されています。

中国の作物保護剤の市場動向

IPM戦略やその他の農薬保護化学品削減施策がヘクタール当たりの農薬保護化学品消費量削減に貢献

- 過去数年間、中国の1ヘクタール当たりの農薬保護化学品消費量は顕著に減少しています。過去に、農薬保護化学品の使用量は1ヘクタールあたり約300グラムまで大幅に減少しました。2017年の消費量は1ヘクタール当たり1,700グラムだったが、2022年には1ヘクタール当たり1,400グラムまで減少しました。

- 1ヘクタール当たりの農薬保護化学品使用量が大幅に減少したのは、農薬保護化学品消費量の伸びをゼロにするという厳格な施策を実施したことが大きく影響しています。

- 中国は、さまざまな予防措置、代替技術、慎重な農薬保護化学品散布を含む総合的病害虫管理(IPM)戦略の採用を積極的に推進してきました。この総合的アプローチの結果、農薬保護化学品使用率は顕著に減少しました。

- 中国では除草剤の使用量が88.78グラムと大幅に減少したが、これは主に農業従事者が輪作などのプラクティスを取り入れたことが要因です。輪作は、成長パターンや栄養要求量の異なる作物を交互に栽培することで、雑草のライフサイクルを効果的に断ち切るものです。このプラクティスを実施することで、中国の農業従事者は雑草の生育サイクルを中断させることに成功し、その結果、雑草の個体数が減少し、除草剤への依存度が低下しました。

- 1ヘクタール当たりの農薬保護化学品使用量のその他の大幅な減少は、特に殺虫剤のカテゴリーで観察され、2017~2022年にかけて58.31グラム減少しました。この減少は主に、有害な殺虫剤の禁止を目的とした政府の施策と、遺伝子組み換え作物の採用に起因します。

- 殺虫剤の使用に関する最大残留基準値の設定など、その他の要因も国内の1ヘクタール当たりの消費量を減少させました。

有効成分の価格は、国内の天候、害虫の発生、エネルギー価格、人件費などの要因に大きく影響されます。

- 中国は、製剤化された農薬保護化学品のベースとなる有効成分の主要生産国のひとつです。殺虫剤は殺虫剤生産の主要シェアを占めています。

- シペルメトリンはピレスロイド系殺虫剤の中で最も広く使用されており、野菜や果実のミバエ、ホウキムシ、メアリ虫など多くの害虫を駆除します。2022年には1トン当たり2万900米ドルと評価されました。

- アトラジンは、様々な広葉雑草や草の防除に広く使用されている除草剤です。中国では年間1万6,000トン以上(技術的に97%)のアトラジンが消費されています。アトラジンは主にトウモロコシやサトウキビ畑の一年生雑草の防除に使用されます。中国は世界のアトラジンの主要供給国のひとつです。2022年の価格は1トン当たり1万3,700米ドルでした。

- Mancozebは広スペクトル接触殺菌剤で、ナタネ、レタス、小麦、リンゴ、トマト、テーブルブドウ、ワインブドウ、球根タマネギ、ニンジン、パースニップ、エシャロット、デュラム小麦の炭疽病、ピシウム病、葉斑病、うどんこ病、ボトリティス病、さび病、かさぶた病など、多くの真菌病害の防除に使用されます。2022年の価格は1トン当たり7,700米ドルでした。

- グリホサートは有機リン系広域スペクトラム浸透性除草剤と作物乾燥剤で、2022年の価格は1トン当たり1,100米ドルでした。グリホサートは主に、イネ科、スゲ科、広葉樹などの雑草の防除に使用されます。中国は世界最大のグリホサート生産・輸出国です。2017年、中国は30万トン以上のグリホサート技術を輸出し、世界のグリホサート需要の半分以上を満たしました。

- 国内の天候、害虫の発生、エネルギー価格、人件費などの要因が有効成分の価格に大きく影響しています。

中国の農薬保護化学品産業概要

中国の農薬保護化学品品市場は適度に統合されており、上位5社で52.57%を占めています。この市場の主要参入企業は、BASF SE、Bayer AG、FMC Corporation、Jiangsu Yangnong Chemical、Syngenta Groupです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬保護化学品消費量

- 有効成分の価格分析

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション(市場規模(単位:米ドル、数量)、2030年までの予測、成長見込みの分析を含む)

- 機能

- 殺菌剤

- 除草剤

- 殺虫剤

- 殺軟体動物剤

- 殺線虫剤

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 49061

The China Crop Protection Chemicals Market size is estimated at 5.41 billion USD in 2025, and is expected to reach 6.95 billion USD by 2030, growing at a CAGR of 5.13% during the forecast period (2025-2030).

Herbicides dominate the market

- China is a major producer of active ingredients that serve as the foundation for formulated agrochemicals and ready-made pesticides sold in many countries. The country is one of the world's largest producers and exporters of crop protection chemicals. Insecticides comprise an important segment in the crop protection chemicals market. The key drivers of the market are a high number of people, limited size of farms, rising food security, and an urgent need for efficient agricultural production. China occupied the highest share of 20.8% by value of the overall Asia-Pacific crop protection chemicals market in 2022.

- Herbicides accounted for the largest share of 38.2% by value in the Chinese crop protection chemicals market in 2022. In China, the use of herbicides has helped in weed control and, thus, increased yields by making it easier for farmers to grow more dwarf rice varieties that are less likely to compete with weeds. Even though there has been a large decline in traditional hand laborers who have moved out of rural areas to industrial zones, herbicides have allowed farmers to control weeds.

- In 2022, the insecticide segment held a significant share of 30.0% by value in the market. The most common pesticides registered for use in cotton are insecticides. Among them, phoxim has the highest number of registered active substances, including cypermethrin and beta-cypermethrin.

- With the increasing concern over the infestation of pests and diseases and the rise in international demand, companies and the government are continuously investing in research projects and developing new active ingredients to prevent crop damage from pests. The market is anticipated to register a CAGR of 5.4% during the forecast period.

China Crop Protection Chemicals Market Trends

IPM strategies and other pesticide reduction policies contributed to reduction in per hectare pesticides consumption

- Over the past few years, there has been a notable reduction in pesticide consumption per hectare in the country. During the historical period, there was a significant decline in pesticide usage to approximately 300 grams per hectare. In 2017, the consumption stood at 1,700 grams per hectare; however, by 2022, it had dropped to 1,400 grams per hectare.

- The considerable reduction in pesticide utilization per hectare can be largely attributed to the country's implementation of a stringent policy of zero growth in pesticide consumption.

- China has proactively promoted the adoption of Integrated Pest Management (IPM) strategies, encompassing a range of preventive measures, alternative techniques, and careful pesticide applications. As a result of this holistic approach, there has been a notable reduction in pesticide usage rates.

- China witnessed a significant decline in herbicide usage by 88.78 grams, primarily driven by the adoption of practices such as crop rotation by farmers. Crop rotation involves alternating different crops with varying growth patterns and nutritional requirements, effectively breaking the lifecycle of weeds. By implementing this practice, Chinese farmers have successfully disrupted weed growth cycles, resulting in reduced weed populations and a decreased reliance on herbicides.

- The other substantial decrease in pesticide usage per hectare was observed specifically in the category of insecticides, with a reduction of 58.31 grams from 2017 to 2022. This decline can be primarily attributed to government policies aimed at banning harmful insecticides and the adoption of transgenic crops.

- Other factors like setting limits on the maximum residue levels on the usage of pesticides reduced the per hectare consumption in the country.

The active ingredients' prices are majorly influenced by factors like weather conditions, pest outbreaks, energy prices, and labor costs in the country

- China is one of the major producers of active ingredients that form the base of formulated crop protection chemicals. Insecticides constitute the major share of pesticide production.

- Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at USD 20.9 thousand per metric ton in 2022.

- Atrazine is a herbicide widely used to control various broadleaved weeds and grasses. China consumes more than 16,000 ton (97% technical) of atrazine annually. Atrazine is mainly used to control annual weeds in corn or sugarcane fields. China is one of the major suppliers of atrazine worldwide. It was priced at USD 13.7 thousand per metric ton in 2022.

- Mancozeb is a broad-spectrum contact fungicide used to control a number of fungal diseases, such as anthracnose, Pythium blight, leaf spot, downy mildew, Botrytis, rust, and scab in oilseed rape, lettuce, wheat, apples, tomatoes, table grapes, wine grapes, bulb onions, carrot, parsnip, shallot, and durum wheat. It was priced at USD 7.7 thousand per metric ton in 2022.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant, priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves. China is the largest producer and exporter of glyphosate in the world. In 2017, China exported over 300,000 ton of glyphosate technical, which met more than half of the global glyphosate demand.

- Factors like weather conditions, pest outbreaks, energy prices, and labor costs in the country majorly influence the prices of active ingredients.

China Crop Protection Chemicals Industry Overview

The China Crop Protection Chemicals Market is moderately consolidated, with the top five companies occupying 52.57%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Jiangsu Yangnong Chemical Co. Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

中国の農薬保護化学品市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 201 Pages

- 納期

- 2~3営業日