|

市場調査レポート

商品コード

1906988

北米の作物保護用化学品:市場シェア分析、業界動向、統計、成長予測(2026年~2031年)North America Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の作物保護用化学品:市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

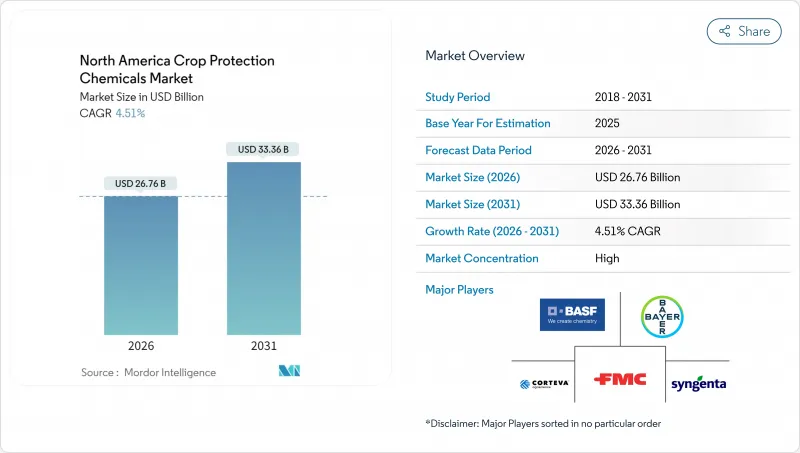

北米の作物保護用化学品市場規模は、2026年に267億6,000万米ドルと推定され、2025年の256億米ドルから成長が見込まれます。

2031年の予測では333億6,000万米ドルに達し、2026年から2031年にかけてCAGR4.51%で拡大する見通しです。

雑草の耐性化、真菌病の急増、低リスク活性成分への規制上の選好拡大が化学薬品需要を後押ししています。一方、精密農業ツールによる無駄の削減が進んでいます。生産者は広大な農地での効率性から合成除草剤を依然として好んでいますが、米国環境保護庁(EPA)の迅速承認プロセスにより、生物学的・生物学的合理性に基づく製品が急速に拡大しています。同地域における大規模な穀物生産基盤、米国・メキシコ・カナダ協定(USMCA)に基づく安定した輸出ルート、保全耕作に対する炭素クレジット優遇措置などが、従来型化学物質をめぐる訴訟にもかかわらず支出を持続させています。主要企業が種子・化学製品・デジタル農学を統合して顧客シェアを獲得すると同時に、厳格化する残留基準値への対応を進める中、競合の激しさは依然として高い水準にあります。

北米作物保護用化学品市場の動向と洞察

除草剤耐性形質の採用加速

除草剤耐性大豆の採用率は主要生産地域で95%を超え、トウモロコシは89%に達しています。これらの形質はより広い発芽後処理の適用期間を可能とし、季節的な除草剤使用量を増加させるとともに輪作の柔軟性を拡大します。グリホサート耐性雑草(パルマーアマランサスなど)が深刻化する中、EPAによるディカンバ及び2,4-Dベースのプラットフォーム認可は新たな作用機序をもたらしました。コルテバ社のエンリストE3やバイエル社のエクステンドフレックスといった複合技術は、プレミアム価格の形成を促進し、化学品と種子のバンドルパッケージを後押ししています。統合された可変率散布技術は区域ごとの投与量を最適化し、これらの形質を現代農学にさらに定着させています。遺伝子技術と精密機器の相乗効果により、ジェネリック製品による価格圧力にもかかわらず、選択性除草剤への需要は持続しています。

精密散布機器による1エーカーあたりのコスト削減

ジョンディア社の「See and Spray」実証試験が示すように、コンピュータービジョン搭載散布機は雑草を個別識別し、防除効果を維持しながら薬剤使用量を最大77%削減します。米国農務省(USDA)のFARMER助成金による公的支援は、設備コストを相殺することで普及を加速させています。搭載センサーが散布量をリアルタイムで調整し、重複散布やドリフトを最小限に抑えることで、投入コストを削減するとともに、対象外への移動に関する規制当局の監視にも対応します。補充作業時間の短縮と労働力削減により、数千エーカーを管理する大規模農場の運営効率が向上します。機器販売店では現在、データ分析サービスのサブスクリプションをバンドル提供しており、生産者が節約効果を検証できるため、互換性のある薬剤の継続購入を促進しています。

カナダが提案する残留基準値(MRL)引き下げが輸出を制限

カナダ保健省は、海外の買い手がより厳しい基準を採用した場合に輸出リスクが生じる農産物について、2,4-Dなど複数の有効成分のMRL(最大残留基準値)を半減させることを提案しています。基準の相違により、生産者は最低基準を満たす必要が生じ、分析試験コストが増加するとともに、残留量の少ない農薬への移行が促進されます。輸出依存度の高いブリティッシュコロンビア州およびオンタリオ州の生産者は、出荷期間の短縮化とコンプライアンス文書の増加を見込んでいます。化学メーカーは残留研究や表示修正に追加予算を割り当てており、新製品の投資回収期間が長期化する見込みです。

セグメント分析

除草剤は2025年、北米の作物保護用化学品市場収益の51.65%を占めました。これは1億8,000万エーカーに及ぶトウモロコシ・大豆畑における化学的雑草防除への広範な依存を反映しています。精密散布技術と形質駆動型選択性が、生育期間を通じた収量ポテンシャルを保護する発芽後処理製品への生産者の継続的な選好を支えています。抵抗性管理には複数の作用機序が必要であり、保全耕作による除草剤使用量の増加も相まって、本セグメントは2031年までCAGR4.88%で拡大すると予測されます。同時に、タール斑病や大豆さび病の発生地域拡大により殺菌剤の使用が加速し、全体的な支出の多様化が進んでいます。殺虫剤は生物学的競合製品や花粉媒介者保護規制の強化による圧力に直面していますが、西部トウモロコシ根虫の散発的な発生に対する統合防除プログラムにおいて依然として不可欠です。

特に残留基準値が課される果樹・野菜栽培面積において、スタック可能な生物学的除草剤への移行が進んでいます。主要企業は合成活性成分と微生物活性成分を組み合わせたマイクロカプセル製剤を発売し、環境基準を満たしつつ効果持続期間を延長しています。製品管理イニシアチブでは、抵抗性発生抑制のため化学物質のローテーションや被覆作物の導入について生産者への啓発活動を実施中です。これらの動向が相まって、除草剤は全体的な薬剤構成が変化する中でも市場の要としての地位を維持しています。

北米の作物保護用化学品市場レポートは、機能別(殺菌剤、除草剤、殺虫剤など)、適用方法別(化学灌漑、葉面散布、燻蒸、種子処理など)、作物種別(商業作物、果樹・野菜、穀類など)、地域別(カナダ、メキシコなど)に分類されています。市場予測は、金額(米ドル)と数量(メトリックトン)の両方の観点から提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリーおよび主要な調査結果

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 除草剤耐性形質の採用加速

- 精密散布機器による1エーカー当たりのコスト削減

- 大豆さび病およびタール斑病の発生急増

- 米国環境保護庁(EPA)による生物学的活性成分の迅速承認

- 低耕起を奨励するカーボンクレジット制度

- メキシコ政府によるIPMツールへの補助金

- 市場抑制要因

- グリホサート訴訟に伴う小売店での取り扱い中止

- カナダにおける残留基準値(MRL)引き下げ案が輸出を制限

- 生物学的代替品増加による合成農薬の利益率圧迫

- 西海岸港湾の混雑による投入資材価格の上昇

第5章 市場規模と成長予測(金額および数量)

- 機能別

- 殺菌剤

- 除草剤

- 殺虫剤

- 殺貝剤

- 殺線虫剤

- 適用方法別

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ別

- 商業作物

- 果樹・野菜

- 穀物・雑穀

- 豆類および油糧種子

- 芝生・観賞植物

- 地域別

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業動向

- 企業プロファイル

- Corteva Agriscience

- Syngenta Group

- Bayer AG

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co. Ltd.

- UPL Limited

- Nufarm Ltd.

- Albaugh LLC

- American Vanguard Corp.

- Bioceres Crop Solutions

- Gowan Company LLC

- Atticus LLC

- Helm Agro US Inc.

- Certis Biologicals