|

市場調査レポート

商品コード

1849921

インドネシアの住宅不動産:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Indonesia Residential Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアの住宅不動産:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

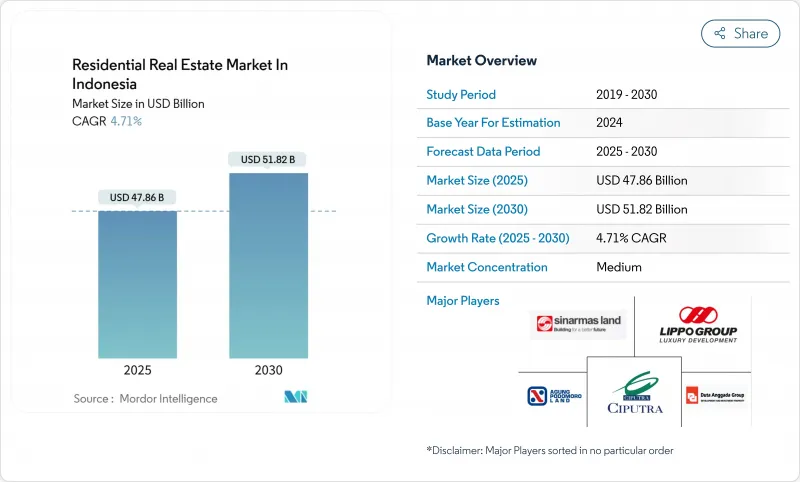

インドネシアの住宅不動産の市場規模は2025年に478億6,000万米ドルで、CAGR 4.71%を反映して2030年には518億2,000万米ドルに上昇すると予測されています。

着実な都市部への移住、政府の300万戸構想、持ち家に対する根強い需要が、インドネシア不動産市場の成長見通しを支えています。現在、郊外のタウンシップが新規供給の大部分を吸収し、中核都市の混雑を緩和する一方、周辺地区の建設活動を刺激しています。インドネシア銀行による金利緩和と、OJKの認可を受けたフィンテック・モーゲージ・レンダーの拡大が、住宅取得コストを下げ、消費者の裾野を広げています。市場開拓者は、住宅、小売、公共施設を組み合わせた交通至便な総合タウンシップ・プロジェクトに資本を再配分し、インドネシア不動産市場の次の需要を取り込む態勢を整えつつあります。

インドネシアの住宅不動産市場動向と洞察

政府が支援するTier1およびTier2都市の総合タウンシップ・マスタープランが住宅供給を拡大

公共事業省は2025年に29兆5,700億ルピーの予算を戦略的インフラ整備に投じ、土地の整備コストを削減し、990万戸と推定される国の供給不足を解消する官民タウンシップ・プラットフォームに資源を投入します。国営企業が道路や公共事業に資金を提供し、民間デベロッパーが住宅を供給することで、インドネシア不動産市場のスケールメリットと迅速な吸収が可能になります。二次都市では、土地の価格が手ごろなままであるため、建設業者は社会的住宅の目標に適合しながらも商業的な利幅を確保できるような、所得の混在した地域を展開することができ、特に上昇余地が大きいです。マスタープランによる設計は、災害への耐性や環境基準も強化し、銀行融資の基準として採用されつつあります。こうしたプロジェクトが成熟するにつれて、購入者はまとまったアメニティや明確な権利関係から恩恵を受け、意思決定サイクルが短縮され、インドネシア不動産市場の成長が持続します。

ジャボデタベックにおける交通指向型開発の拡大が中間層向けコンドミニアムを牽引

MRTジャカルタは、その最初の沿線におよそ5万戸の住宅を追加し、空地権を収益化し、乗降客数を増やす計画です。新駅の半径500メートル以内に建設されたコンドミニアムは、2024年に最大10%の価格上昇を記録し、通勤者がアクセスプレミアムを支払う意思を確認しました。設計ルールでは、床面積の少なくとも30%を住宅用として確保することが義務付けられており、所得階層別にサブクォータが設定され、包括的な分配が確保されています。デベロッパーは、鉄道建設とプロジェクトの段階を合わせることで、前売りを早期に確保し、保有コストを軽減しています。運輸当局は、このモデルを通勤鉄道運営会社PT KAIと模倣し始めており、インドネシアの不動産市場が今後10年間で、鉄道と連動した垂直型へとますます軸足を移していくことを示しています。

長引く土地の権利化とPBG許可の遅れ

2025年の改革により、補助金付き住宅については標準的な許認可が最短4時間に短縮されたにもかかわらず、断片化された地籍記録は多くの地区でいまだに手作業による照合を必要としています。デベロッパーは、建設前に何年も土地を持ち続け、資本を拘束し、最終価格をつり上げることが多いです。土地バンク機関は、社会住宅用の区画をプールするために設立されたが、人員に限りがあるため取得が遅れ、プログラムの目標と現場での提供との間にミスマッチが生じています。許認可が長引くと、利幅の薄い手ごろな価格のプロジェクトが特にダメージを受ける。スケジュールが延びると、建設業者は高級品に軸足を移し、供給の弾力性を低下させ、インドネシアの不動産市場の成長を抑制します。

セグメント分析

ヴィラ&土地付き住宅は2024年のインドネシア不動産市場シェアの65%を占め、これは私有地所有と大家族レイアウトを好む文化的嗜好を反映しています。しかし、マンション・サブセクターは、乗り換え指向のプロジェクトや都市部の用地縮小に引っ張られ、CAGR 4.90%と全体の成長を上回っています。2024年のジャカルタのプレミアム・コンドミニアムの平均価格は1平方メートル当たり5,770万ルピアで、香港やシンガポールのベンチマークよりまだ低く、キャピタルゲインのアップサイドを維持しています。デベロッパーは、コワーキングスペース、屋上庭園、デジタルコンシェルジュサービスを組み合わせ、若いプロフェッショナルや駐在員を誘致し、入居率を高め、賃貸利回りを8%近くに安定させています。現在、多くの地方自治体がグリーンビルディングへの適合を建築高さ許可の条件としており、エネルギー効率の高いファサードやスマートホームシステムの採用に拍車がかかり、垂直型物件の差別化が進んでいます。

戸建住宅を対象とした土地優遇措置は、高層住宅の勢いを減速させていないです。50億ルピア以下の戸建住宅に対する政府の付加価値税減免措置は、参入コストを削減し、売れ残り在庫を減らします。郊外地区への通勤鉄道の延伸により、CBDへの移動時間が短縮され、ジャカルタの外環を越えても中層棟の建設が可能になっています。その結果、インドネシアでは2030年まで、アパートメントが垂直居住の不動産市場規模を年率4.90%押し上げると予測され、長らく地上型が主流だったセクターのバランスが徐々に回復していきます。

5億ルピアから20億ルピアの中間価格帯の住宅は、2024年のインドネシア不動産市場規模の46%を占める。ホワイトカラーの所得が増加し、フィンテック金融機関による柔軟な頭金支払スキームと相まって、この層の吸収が維持されています。逆に、アフォーダブル住宅は、ジャワ島では1億6,600万ルピーが上限で、パプア州では2億4,000万ルピーまで上昇し、財政上の優遇措置が2025年12月まで延長されるため、CAGR 4.85%で成長する見込みです。購入者は100%の付加価値税免除とBPHTB免除を享受でき、実質的な取得コストを最大13%削減できるため、住宅所有に必要な貯蓄期間を短縮できます。

外資規制では、マンションは最低30億ルピア、土地付き住宅は最低50億ルピアと規定されているため、海外からの購入者は当然、より高い階層に向かうことになり、大衆市場の大部分は国内市場にとどまる。しかし、カタールとUAEが社会住宅ベンチャーに数十億米ドルを投じたことで、資金調達ルートが広がり、デベロッパーは生産規模を拡大したり、資材の一括割引を確保したりできるようになりました。固定金利5%、頭金1,000万ルピアまでの補助金付き住宅ローンは、参入障壁をさらに狭めています。このような仕組みが総合的に、初めて住宅を購入する層を拡大し、インドネシア不動産市場の長期的な拡大を支えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 経済と市場の概要

- 不動産購入動向- 社会経済的・人口統計的洞察

- 規制の見通し

- テクノロジーの展望

- 不動産セグメントの賃貸利回りに関する洞察

- 不動産融資の動向

- 政府と官民パートナーシップによる廉価住宅支援に関する洞察

- 市場促進要因

- Tier-1およびTier-2都市における政府支援の総合タウンシップ・マスタープランが住宅供給を拡大する

- ジャボデタベックにおける交通指向型開発の拡大が中間層向けコンドミニアムを牽引

- OJKが承認したデジタル住宅ローン・プラットフォームの急速な普及

- 産業回廊で増加するミレニアル世代の世帯形成(カラワンーブカシ)

- IDR20億未満のユニットに対するVAT免除がファーストホーム購入を加速させる

- 外国人所有権の制限が緩和され、駐在員やディアスポラの需要に拍車がかかる

- 供給が多様化する二級都市(マカッサル、バタム)のタウンシップ・プロジェクト

- 市場抑制要因

- 土地の権利化とPBG許可の遅れ

- 建設資材インフレはニッケル主導のセメントと鉄鋼価格に連動する

- プレミアムCBDアパートメントの持続的供給過剰(ジャカルタ中心部)

- ジャカルタ北部の開発を制限する沿岸洪水リスク

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者と請負業者- 定量的・定性的な主な洞察

- 不動産ブローカーとエージェント- 主要な定量的・定性的洞察

- 不動産管理会社- 主要な定量的・定性的洞察

- バリュエーション・アドバイザリーおよびその他の不動産サービスに関する洞察

- 建築資材業界の現状と主な開発業者とのパートナーシップ

- 市場における主要な戦略的不動産投資家/バイヤーに関する洞察

- ポーターのファイブフォース

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 物件タイプ別

- アパート・マンション

- ヴィラ・土地付き住宅

- 価格帯別

- 手頃な価格

- ミッドマーケット

- 高級

- 販売形態別

- プライマリー(新築)

- セカンダリー(中古住宅再販)

- ビジネスモデル別

- 販売

- 賃貸

- 地域別

- ジャワ

- スマトラ

- カリマンタン

- スラウェシ

- その他の地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Agung Podomoro Land Tbk

- Sinar Mas Land(BSD, BSD City)

- Ciputra Development Tbk

- Pakuwon Jati Tbk

- Lippo Homes/PT Lippo Karawaci Tbk

- Summarecon Agung Tbk

- Paramount Land

- Agung Sedayu Group

- Intiland Development Tbk

- Duta Anggada Realty Tbk

- PP Properti Tbk

- Tokyu Land Indonesia

- JABABEKA Tbk

- Wijaya Karya Realty

- Metropolitan Land Tbk

- Paramount Enterprise International

- Greenland Indonesia

- Perumnas(National Housing Corp.)

- PT HK Realtindo

- Trans Property

- MNC Land Tbk