|

市場調査レポート

商品コード

1849972

欧州の住宅不動産市場:シェア分析、産業動向、統計、成長予測(2025年~2030年)Europe Residential Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の住宅不動産市場:シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

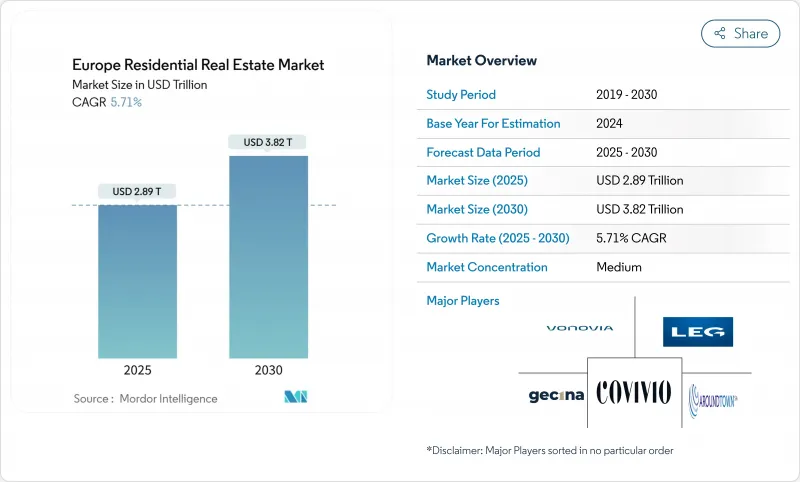

欧州の住宅不動産の市場規模は、2025年に2兆8,900億米ドルと評価され、2030年には3兆8,200億米ドルに拡大すると予測されています。

この軌跡は、金融政策の変化、エネルギー規制の強化、人口動態の変化を吸収する欧州不動産市場の能力を示しています。機関投資家は予測可能なキャッシュフローを優先するため、需要は専門的に管理された賃貸プラットフォームに引き寄せられる一方、主要都市における供給のボトルネックにより、多くのゲートウェイ都市では全体の空室率が3%を下回っています。EUのグリーン・ディールに基づく政策主導の改修義務は、建設パイプラインを再構築しており、欧州の住宅在庫は高齢者に偏っているため、二次売買が引き続き主流となっています。デジタルノマドビザプログラム、単身世帯の増加、目的別賃貸コミュニティの台頭が、欧州不動産市場のバランスの取れた、かつ弾力的な拡大路線を支えています。

欧州の住宅不動産市場動向と洞察

国境を越えたプライベート・エクイティの流入が急増、欧州のビルド・トゥ・レント・ポートフォリオがターゲットに

国境を越えたプライベート・エクイティの住宅投資額は過去10年間で3倍に増加し、大規模なビルド・トゥ・レント資産への構造的な傾斜を支えています。グローバルな年金基金や政府系ファンドからの流動性は、家計所得よりも金利サイクルの影響を受けやすい資本を注入することで、従来の賃金と価格の関係を断ち切りました。クロスボーダー資産配分では英国が首位の座を奪還し、調査対象の84%の投資家が通貨再調整後のエクスポージャーを計画しています。現在、機関投資家の「リビング・セクター」アロケーションの32%を賃貸住宅戦略が占め、産業ロジスティクスを上回っています。安定したキャッシュフロー、インフレ連動リース、改装の可能性を組み込んだこれらのポートフォリオは、オフィス市場のボラティリティに対するヘッジとなっています。その結果、資金調達コストの上昇にもかかわらず、資本の厚みが建設資金を支え、金利主導の景気減速に対する欧州不動産市場のクッションとなっています。

EUのグリーン・ディール奨励策が住宅ストック全体のディープ・レトロフィット需要を加速

改正建築物エネルギー性能指令は、2030年までにすべての住宅ストックを少なくともクラスEにすることを義務付け、2000年以前の住宅の85%を改修パイプラインに押し込みます。加盟国は「改修パスポート」を発行し、ワンストップ・アドバイス・ショップを調整し、2035年までに化石燃料ボイラーを段階的に廃止しなければならないです。2028年以降の新築住宅のゼロエミッション目標は、レガシー資産のアップグレードとエネルギーに前向きな開発という2つの需要急増を生み出します。この政策により、2025年から2027年にかけて860億ユーロの資金ギャップが生じ、金融機関は持続可能性にリンクした住宅ローンやグリーンボンドを通じてこれを埋めようとしています。格付けAまたはBの物件は現在、中核都市では最大12%のプレミアム価格で取引されており、地主が設備投資計画を加速させるインセンティブとなっています。欧州の不動産市場にとって、この指令は長期にわたる改修のキャッシュフローを固定し、前向きなオーナーには評価の上昇で報いることになります。

欧州中央銀行(ECB)の利上げで広がる住宅ローンのアフォーダビリティ・ギャップ

超低金利融資の突然の終了により、フランスの平均住宅ローン金利は3.63%でピークに達した後、2024年後半には2.75%まで緩和されたが、それでも取引件数は2021年の水準から35.6%減少しました。ECBの分析では、ユーロ圏の住宅市場の80%以上が過大評価されており、金利が回復した場合、借り手は収入ストレスリスクにさらされます。ノルウェーの変動金利住宅ローンは5.56%近辺にあり、2025年の基準金利引き下げが予想されているにもかかわらず、購買力を弱めています。若年層の購入者は、ローン・トゥ・インカムの上限が厳格化され、償却期間が短縮されるため、頭金を準備するのに必要な期間が延びる。新築物件の供給は遅れているもの、与信の厳格化により、欧州の不動産市場の持ち家需要は短期的には抑制されています。

セグメント分析

2024年の欧州の住宅不動産市場シェアは、ヴィラと土地付き住宅が65%を占める一方、アパートとコンドミニアムは2030年までCAGR 5.96%を記録します。スケーラブルな集合住宅への機関投資家の関心は、資本を集中させ、建設パイプラインを加速させる一方、木造ハイブリッド設計は具体化炭素を削減し、建設期間を短縮します。

アパートの急増は、エネルギー効率の高い設計に報いるESG連動ローンの価格設定によって補強され、スポンサーが効率の低いストックよりも25~35ベーシス・ポイント狭いスプレッドで負債を確保するのに役立っています。ヴィラは屋外スペースを求める家族にとって引き続き魅力的であり、周辺交通機関のアップグレードは戸建て需要を維持します。しかし、人口動態がコンパクトな住まいを好む傾向にあることや、自治体が高密度化計画のためにブラウンフィールドの用地を解放していることから、都市部のアパートメントに関連する欧州の不動産市場規模は拡大しています。

2024年の欧州の住宅不動産市場規模に占める中間市場の取引比率は46%だが、官民パートナーシップとゾーニング・インセンティブを背景に、アフォーダブル層はCAGR 5.90%で拡大すると予測されます。政府は、ソーシャルハウジング機関によって裏付けされたインフレ連動型賃料を提供する長期リースを通じて、機関投資家の資金を活用します。

グレイスターとABPによる4億2,000万ユーロのエッセンシャル・ハウジング(Essential Housing)ベンチャーは、市場賃料以下の資産に対する資本の意欲を示しており、プライムな市場賃料ストックの利回りと比べて小幅な圧縮にとどまる利回りを実現しています。高級住宅は、グローバル都市の中心部では依然として底堅いもの、そのシェアは小さいです。このように、手頃な価格への政策的な後押しは、パイプラインの構成を再構築し、欧州の不動産市場に社会的目標を注入しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 経済と市場の概要

- 不動産購入動向ー社会経済的および人口動態的洞察

- 規制の見通し

- テクノロジーの展望

- 不動産セグメントにおける賃貸利回りに関する洞察

- 不動産融資の動向

- 政府および官民連携による手頃な価格の住宅支援に関する洞察

- 市場促進要因

- 欧州の賃貸住宅ポートフォリオをターゲットとしたクロスボーダーのプライベートエクイティ資金流入の急増

- EUグリーンディールのインセンティブが住宅ストック全体の大規模な改修需要を加速

- 単身世帯の増加が都市中心部の集合住宅の普及を促進

- デジタル遊牧民ビザの導入が南欧のセカンドハウス購入を促進

- 機関投資家は、専用賃貸コミュニティへと方向転換

- 高齢化が進むドイツと北欧では高齢者向け住宅や介護付き住宅の開発が拡大

- 市場抑制要因

- ECBの利上げで住宅ローン返済能力の格差が拡大

- より厳しいEPC規則が地主の設備投資額を膨らませている

- 南欧の賃金停滞が初めて住宅を購入する人の住宅購入能力を制限

- 都市成長の境界が中核都市における緑地供給を制限する

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者と建設業者-主要な定量的および定性的な洞察

- 不動産ブローカーとエージェント-主要な定量的および定性的な洞察

- 不動産管理会社-主要な定量的および定性的な洞察

- 評価アドバイザリーおよびその他の不動産サービスに関する洞察

- 建築資材業界の現状と主要開発業者とのパートナーシップ

- 市場における主要な戦略的不動産投資家/購入者に関する洞察

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 物件タイプ別

- アパートとコンドミニアム

- ヴィラと戸建て住宅

- 価格帯別

- 手頃な価格

- ミッドマーケット

- 高級

- 販売形態別

- プライマリー(新築)

- セカンダリー(既存住宅の再販)

- ビジネスモデル別

- 販売

- レンタル

- 国別

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- スウェーデン

- デンマーク

- ノルウェー

- その他欧州地域

第6章 競合情勢

- 戦略的動きと投資

- 市場シェア分析

- 企業プロファイル

- Vonovia SE

- LEG Immobilien AG

- Gecina SA

- Covivio SA

- Aroundtown SA

- Heimstaden Bostad AB

- Grainger PLC

- Aedifica SA

- CPI Property Group

- TAG Immobilien AG

- Consus Real Estate AG

- Bonava AB

- Nexity SA

- Barratt Developments PLC

- Taylor Wimpey PLC

- Persimmon PLC

- Skanska AB

- NCC AB

- Glenveagh Properties PLC

- Inmobiliaria Colonial SOCIMI SA

- Patrizia SE

- Adler Group SA

- Unite Group PLC(Student Housing)