|

市場調査レポート

商品コード

1850122

米国住宅不動産:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)United States Residential Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国住宅不動産:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

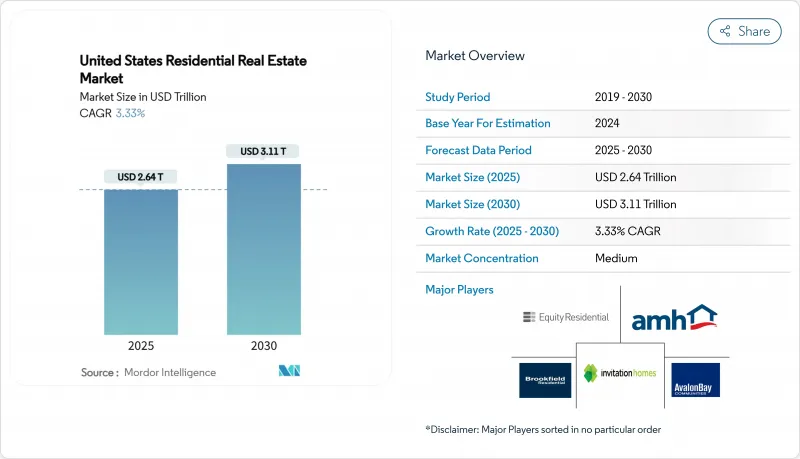

米国住宅不動産の市場規模は、2025年に2兆6,400億米ドル、2030年には3兆1,100億米ドルに達すると予測され、CAGRは3.33%です。

成長率は小幅に見えるが、これは機関投資家の急増、サンベルト州における賃貸住宅建設ブーム、過去の値ごろ感の壁を乗り越えつつあるミレニアル世代の購入者という人口動態の波など、決定的な構造的変化を覆い隠しています。テクノロジー主導の雇用創出、極端な供給不足、持続的な遠隔地からの労働移民の流れが原動力となっています。機関投資家は、ブラックストーン、インビテーション・ホームズ、その他のREITに牽引されながら、ポートフォリオを拡大し続け、専門的な運用基準を加速させ、資産クラス全体の流動性を高めています。同時に、連邦政府によるエネルギー効率化奨励策、先進的な不動産管理ツール、分譲オーナーシップ・プラットフォームが、需要パターンを再構築し、個人投資家に新たなエントリー・ポイントを開こうとしています。特に、住宅ローン金利の変動、建設労働者の不足、気候変動リスク地帯における保険料の急上昇など、逆風は依然として残っており、手頃な価格帯の住宅と高級住宅が相反する方向に動く、二分化した市場を形成しています。

米国住宅不動産市場動向と洞察

サンベルト地帯で加速する一戸建て賃貸需要

テキサス州、フロリダ州、アリゾナ州、ジョージア州、ノースカロライナ州では、開発業者が需要に応えようと奔走し、一戸建て賃貸住宅(BTR)の引き渡しが2019年から2023年にかけて3倍に増加し、307%急増しました。2023年には、前年比75%増の2万7495戸のBTR住宅が竣工し、2024年から2026年にかけて4万5400戸の追加供給が予定されています。アメリカン・ホームズ4・レントは最近、目的別に建設された住宅が1万戸を突破し、さらに1万戸を計画中であることを明らかにしました。フェニックス、ダラス、アトランタは、BTRコミュニティーの中心地となっており、所有の負担がない一戸建て住宅への消費者の嗜好の変化を反映しています。手ごろな価格の制約とライフスタイルの柔軟性がテナント需要を強化するため、このセグメントは2030年まで主要な成長エンジンであり続けると予想されます。

リモートワークによる第二級都市への移住の急増

2024年初頭には、有給労働日の約28%がリモートワークで占められており、世帯は雇用と住居の場所を切り離し、より手頃な都市に移転することができます。人口25万人未満の小さな町は2023年に29万1,400人の新規人口を獲得し、1970年代以来初めて大都市への人口流入を上回りました。移転労働者は年間住宅費を1,200米ドルから1万2,000米ドル節約し、多くの場合、移転元の都市よりも7,500米ドル安い価格の住宅を購入しています。シャーロット、ローリー、オーランドは、雇用創出と低コストを両立させた受益者として浮上しています。この移動動向は、資本と労働力を、持続的な需要が見込まれる第二級都市に振り向けることで、米国住宅不動産市場を構造的に拡大しています。

住宅ローン金利の変動が値ごろ感を損なう

2025年1月の30年固定住宅ローン平均金利は6.93%近辺で推移し、この水準は歴史的な金利と実勢金利のギャップを広げ、多くの所有者を既存のローンに固定しました。フレディマックは、2024年後半に一般的な従来型住宅ローンを借り入れた場合、このロックインの金額を4万7,800米ドルと算出しました。ロックインに起因する在庫不足が価格上昇圧力となり、初回購入者のシェアは2024年に24%まで低下し、1981年以来最低となりました。予想では、金利は2025年第4四半期には6.5%まで低下する可能性があるが、2021年からの4%以下の水準をはるかに上回っており、米国住宅不動産市場の活動を和らげる摩擦が続いていることを示しています。

セグメント分析

2024年の米国住宅不動産市場では、アパートとマンションが81%を占め、別荘や土地付き住宅を上回り、2030年までのCAGRは2.10%で成長するとみられます。BlackstoneがAIR Communitiesを100億米ドルで買収し、安定した賃貸収入への自信を強めたことで、金融機関は集合住宅の供給を加速させました。賃貸住宅建設の勢いは賃貸プールをさらに拡大し、2023年には27,495戸のBTR専用住宅が供給されます。したがって、世帯形成が柔軟でアメニティに富んだコミュニティへとシフトするにつれて、アパートの米国住宅不動産市場規模は拡大する傾向にあります。

ヴィラと土地付き住宅は在庫の19%を占めるが、特に保険料が高騰するリスクの高い沿岸部の郡部では、気候保険と値ごろ感という逆風に直面しています。富の流入が旺盛な高級住宅地では需要が持続しているが、新規供給は土地の希少性とゾーニングに制約されたままです。一戸建ての賃貸住宅は、所有のハードルなしに一戸建ての生活を提供し、米国住宅不動産市場をさらに多様化させる。

2024年の米国住宅不動産市場シェアは販売チャネルが78%を占めるが、住宅ローンの高止まりにより、賃貸収入は2030年までCAGR 2.26%で拡大します。インビテーション・ホームズだけでも、2025年までに6億米ドルから10億米ドルの買収を計画しています。機関投資家の資金調達能力と専門的な管理が入居者の経験を向上させ、賃貸住宅への需要を強化しています。

米国住宅不動産の市場規模では、依然として持ち家取引が大半を占めているが、ロックイン効果と信用基準の厳格化により、より多くの世帯がより長く賃貸するようになっています。人口動態の動向は、ミレニアル世代が所有に踏み切る前にオプショナリティを求めるため、このシフトを増幅させ、賃貸シェアが徐々に、しかし持続的に上昇することを示唆しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 経済と市場の概要

- 不動産購入動向-社会経済的および人口動態的洞察

- 規制の見通し

- テクノロジーの展望

- 不動産セグメントにおける賃貸利回りに関する洞察

- 不動産融資の動向

- 政府および官民連携による手頃な価格の住宅支援に関する洞察

- 市場促進要因

- サンベルト州における賃貸用一戸建て住宅の需要増加

- リモートワークをきっかけに第二大都市圏への移住が急増

- 住宅REITとPEファンドを通じた機関投資家の資本流入

- ネットゼロ住宅およびエネルギー効率の高い住宅に対する連邦政府のインセンティブ

- テクノロジーを活用した販売チャネル(iBuying、分割所有)

- 購買意欲の高い年齢に突入したミレニアル世代による人口動態の追い風

- 市場抑制要因

- 住宅ローン金利の変動が住宅購入の負担を弱める

- 建設労働者不足と資材費の高騰

- 新規供給を制限する地域規制

- 気候リスク地域における保険料の上昇

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者と建設業者- 主要な定量的および定性的な洞察

- 不動産ブローカーとエージェント- 主要な定量的および定性的な洞察

- 不動産管理会社- 主要な定量的および定性的な洞察

- 評価アドバイザリーおよびその他の不動産サービスに関する洞察

- 建築資材業界の現状と主要開発業者とのパートナーシップ

- 市場における主要な戦略的不動産投資家/購入者に関する洞察

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 物件タイプ別

- アパートとマンション

- ヴィラと戸建て住宅

- 価格帯別

- 手頃な価格

- ミッドマーケット

- 高級

- ビジネスモデル別

- 販売

- レンタル

- 販売形態別

- プライマリー(新築)

- セカンダリー(既存住宅の再販)

- 地域別

- 北東

- 中西部

- 南東

- 西

- 南西

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Invitation Homes Inc.

- Equity Residential

- AvalonBay Communities Inc.

- American Homes 4 Rent

- Brookfield Residential Properties Inc.

- Greystar Real Estate Partners LLC

- Lennar Corporation

- D.R. Horton Inc.

- PulteGroup Inc.

- KB Home

- Toll Brothers Inc.

- Mill Creek Residential Trust LLC

- Alliance Residential Company

- Lincoln Property Company

- The Michaels Organization

- Essex Property Trust Inc.

- Simon Property Group(Residential Arm)

- RE/MAX Holdings Inc.

- Keller Williams Realty Inc.

- Redfin Corporation

- Opendoor Technologies Inc.