|

市場調査レポート

商品コード

1684081

南米の建設用化学品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)South America Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の建設用化学品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 406 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

南米の建設用化学品市場規模は2024年に46億8,000万米ドルと推計され、2030年には65億3,000万米ドルに達し、予測期間(2024年~2030年)のCAGRは5.73%で成長すると予測されます。

Procrear 2023とMinha Casa, Minha Vida住宅計画が南米の建設用化学品需要に及ぼす影響

- 南米の建設用化学品の需要は2022年に5.89%増加したが、これは主に建設活動の急増によるものです。特にブラジルでは、2022年の新設住宅床面積が前年比4.1%増となりました。商業部門とインフラ部門が牽引役となり、南米の建設用化学品市場は2023年に金額ベースで2022年比5.55%成長すると予測されました。

- 南米ではアルゼンチンとブラジルが建設用化学品の消費を独占しています。特に、両国の住宅部門が最も需要が高く、2022年の全エンドユーザー部門に占める割合はそれぞれ30%と43%です。

- ほとんどの南米諸国では、産業部門と施設部門が建設用化学品の主要消費者です。しかしブラジルでは、住宅部門が第2位を占めており、この地域で第2位のエンドユーザー部門となっています。ブラジルとアルゼンチンを除けば、2022年の同地域の他国全体の需要に占める産業・施設部門の割合は45%でした。

- 予測では、ブラジルとアルゼンチンが、主に住宅部門を原動力として、建設用化学製品の需要が最も急増します。アルゼンチンの「Procrear 2023」やブラジルの「Minha Casa, Minha Vida」といった国家的な住宅イニシアチブは、新築住宅の建設や既存住宅の改築に拍車をかけることになります。その結果、予測期間(2023年~2030年)のCAGRは6.36%と予測され、住宅部門が最も急速な需要拡大をすることになります。

南米の建設用化学品市場におけるブラジルの優位性拡大

- 2022年には、住宅部門が南米における建設化学製品の主要な消費者に浮上し、全セクターの総需要の約35%を占めました。大規模な住宅部門を持つブラジルがこの需要の先陣を切りました。2023年を展望すると、この地域で最も需要が急増するのは商業・インフラ部門です。

- この地域最大の経済大国であり、最も人口の多い国であるブラジルは、当然ながら建設生産高でもリードしています。その結果、ブラジルは建設用化学製品の消費量も最も多いです。特に、ブラジルの住宅部門が大きなシェアを占めており、2022年の国内総消費量の約43%を占める。

- ブラジルに次いで、アルゼンチンは建設用化学品の第2位の消費国です。アルゼンチンだけで2022年に3億7,850万米ドルの需要があります。この需要は主に、2022年に2億2,330万米ドル以上を占める同国の住宅および工業/施設部門が牽引しています。

- ブラジルの住宅および工業/施設セクターでは、2030年までに新設床面積が大幅に増加すると予測されており(2022年比でそれぞれ37%、30%)、建築用化学薬品の需要が急増すると見込まれています。その結果、南米ではブラジルが建設用化学品市場の拡大をリードすると予測され、2023年から2030年までのCAGRは6.11%と予測されます。

南米の建設用化学品市場の動向

同地域における外国直接投資(FDI)の増加が今後数年間の市場需要を後押し

- 2022年、南米の商業セクターは、アルゼンチンの9.16%減に大きく牽引され、新規床面積建設が16.2%減と大幅に減少しました。しかし、このセクターは2023年には回復に向かい、生産量は4.75%増加すると予測されました。この成長は、2022年にこの地域の様々な産業が外国直接投資(FDI)を誘致したことによる経済成長と商業建築の急増に起因しています。2022年、ラテンアメリカ・カリブ海経済委員会(ECLAC)は、同地域のFDIが55.2%増加したと報告しました。

- 同部門の建設量は、2020年に15.9%、2021年にはさらに3.29%の顕著な伸びを示しました。この成長は、南米政府がインフラと建設部門を優先した結果です。南米政府は規制を緩和し、民間および公共事業における建設、メンテナンス、プロジェクト開発を許可しました。この動きは、重要なマイルストーン、期限、景気回復目標を達成することを目的としています。

- 南米の商業セクターでは、新規床面積の建設が堅調な伸びを示し、予測期間(2023年~2030年)のCAGRは数量ベースで4%を記録すると予測されています。同地域では、商業施設の建設状況に顕著な変化が見られます。2023年に開始されたパウリニア・データセンターやポルト・アレグレ・データセンターiのような注目すべきプロジェクトは、この地域で最大級のものです。加えて、投資家はブラジルのオフィスビル、ショッピングセンター、ロジスティックパークに注目しており、今後数年間の市場需要を促進すると予想されます。

南米では手ごろな価格の住宅制度と補助金が住宅セクターの建設増加に影響を与える

- 2022年、南米の住宅部門は前年比3.35%増となりました。しかし、アルゼンチンはこの指標で9.16%の顕著な落ち込みを見せた。2023年には、このセクターは成長軌道を維持し、建設量は2022年よりも3.3%増加すると予測されました。この成長は、都市化の進展、一人当たり所得の増加、全体的な景気拡大といった要因によるもので、これらすべてが住宅需要を煽っています。

- 2020年のCOVID-19パンデミックを背景に、南米では新規床面積建設が前年比11.83%増と大幅に増加しました。これは南米政府による意図的な動きであり、家計所得の急激な減少を踏まえ、景気後退を緩和し労働者を支援するために建設部門を優先させました。その結果、検疫を含む建設活動の制限が緩和されました。

- 南米のいくつかの国では、増加する人口のために住宅をより手頃な価格にするためのイニシアチブを展開しています。例えば、ブラジルは2023年2月、低所得者を対象とした全国的な連邦住宅プログラムを再開しました。2023年10月、世界銀行はエクアドルに対する1億米ドルの融資パッケージを承認しました。ボリビアは、低価格住宅の供給を拡大し、適正な価格を維持しようと努力しており、住宅需要をさらに喚起する構えです。その結果、南米の住宅セクターは予測期間中(2023年~2030年)に4.09%のCAGRで推移すると予測されます。

南米の建設用化学品産業の概要

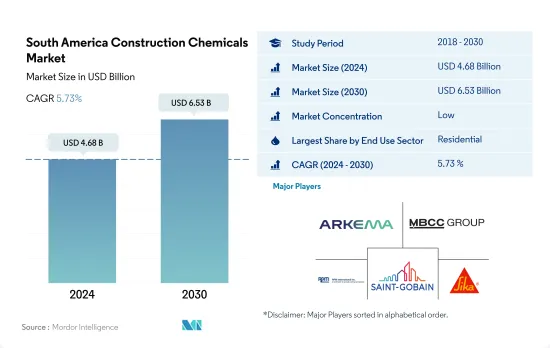

南米の建設用化学品市場は細分化されており、上位5社で26.38%を占めています。この市場の主要企業は以下の通り。 Arkema, MBCC Group, RPM International Inc., Saint-Gobain and Sika AG.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 最終用途分野の動向

- 商業

- 産業・施設

- インフラ

- 住宅

- 主要インフラプロジェクト(現在および発表済み)

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 最終用途セクター

- 商業

- 産業・施設

- インフラ

- 住宅

- 製品

- 接着剤

- サブプロダクト別

- ホットメルト

- 反応性

- 溶剤系

- 水系

- アンカーとグラウト

- サブプロダクト別

- セメント系固定材

- 樹脂固定

- その他のタイプ

- コンクリート混和剤

- サブプロダクト別

- 促進剤

- 空気混入混和剤

- 高範囲減水剤(超可塑剤)

- 遅延剤

- 収縮低減混和剤

- 粘度調整剤

- 減水剤(可塑剤)

- その他のタイプ

- コンクリート保護塗料

- サブプロダクト別

- アクリル系

- アルキド

- エポキシ

- ポリウレタン

- その他の樹脂

- フローリング用樹脂

- サブプロダクト別

- アクリル

- エポキシ

- ポリアスパラギン

- ポリウレタン

- その他の樹脂タイプ

- 補修・再生ケミカル

- サブプロダクト別

- ファイバーラッピングシステム

- 注入グラウト材

- マイクロコンクリートモルタル

- 改質モルタル

- 鉄筋保護材

- シーリング材

- サブプロダクト別

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

- 表面処理薬品

- サブプロダクト別

- 硬化コンパウンド

- 離型剤

- その他の製品タイプ

- 防水ソリューション

- サブプロダクト別

- 化学製品

- メンブレン

- 接着剤

- 国名

- アルゼンチン

- ブラジル

- その他南米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ardex Group

- Arkema

- CEMEX, S.A.B. de C.V.

- Fosroc, Inc.

- Henkel AG & Co. KGaA

- Kryton International Inc.

- LATICRETE International, Inc.

- MAPEI S.p.A.

- MBCC Group

- MC-Bauchemie

- Normet

- RPM International Inc.

- Saint-Gobain

- Selena Group

- Sika AG

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50002034

The South America Construction Chemicals Market size is estimated at 4.68 billion USD in 2024, and is expected to reach 6.53 billion USD by 2030, growing at a CAGR of 5.73% during the forecast period (2024-2030).

Procrear 2023 and Minha Casa, Minha Vida housing schemes' influence over South America's construction chemicals demand

- The demand for construction chemicals in South America witnessed a 5.89% increase in 2022, primarily attributed to a surge in construction activities. Notably, Brazil saw a 4.1% rise in new residential floor areas in 2022 compared to the preceding year. With the commercial and infrastructure sectors leading the way, the construction chemicals market in South America was projected to grow by 5.55% in 2023, in terms of value, when compared to 2022.

- Argentina and Brazil dominate the consumption of construction chemicals in South America. Notably, the residential sector in both countries commands the highest demand, accounting for 30% and 43% of the total demand, respectively, across all end-user sectors in 2022.

- Across most South American countries, the Industrial and Institutional sectors are the primary consumers of construction chemicals. However, in Brazil, the residential sector takes the second spot, making it the region's second-largest end-user sector. Excluding Brazil and Argentina, the Industrial and Institutional sector held a 45% share of the overall demand in 2022 across the other countries in the region.

- Projections indicate that Brazil and Argentina will witness the swiftest surge in construction chemical demand, primarily driven by their residential sectors. National housing initiatives, such as Argentina's Procrear 2023 and Brazil's Minha Casa, Minha Vida, are set to spur the construction of new homes and the renovation of existing ones. Consequently, the residential sector is poised to witness the fastest growth in demand, with a projected CAGR of 6.36% during the forecast period (2023-2030).

The growing dominance of Brazil in South American construction chemicals market

- In 2022, the residential sector emerged as the leading consumer of construction chemicals in South America, accounting for approximately 35% of the total demand across all sectors. Brazil, with its sizable residential sector, spearheaded this demand. Looking ahead to 2023, the commercial and infrastructure sectors are poised to witness the most significant surge in demand in the region.

- Brazil, as the region's largest economy and most populous nation, naturally takes the lead in construction output. Consequently, it also boasts the highest consumption of construction chemicals. Notably, Brazil's residential sector commands the lion's share, representing about 43% of the nation's total consumption in 2022.

- Following Brazil, Argentina stands out as the second-largest consumer of construction chemicals. Argentina alone accounted for a massive demand worth USD 378.5 million in 2022. This demand is primarily driven by the country's residential and industrial/institutional sectors, which accounted for over USD 223.3 million in 2022.

- With Brazil's residential and industrial/institutional sectors projected to witness a significant increase in new floor areas by 2030 (37% and 30%, respectively, compared to 2022), the demand for construction chemicals is expected to surge. As a result, Brazil is anticipated to lead the expansion of the construction chemicals market in South America, with a forecasted CAGR of 6.11% from 2023 to 2030.

South America Construction Chemicals Market Trends

Growing foreign direct investments (FDIs) in the region to aid the market demand in the coming years

- In 2022, the commercial sector in South America saw a significant decline of 16.2% in new floor area construction, largely driven by a 9.16% drop in Argentina. However, the sector was poised for a rebound in 2023, with a projected 4.75% increase in volume output. This growth can be attributed to economic growth and a surge in commercial construction, as various industries in the region attracted foreign direct investments (FDI) in 2022. In 2022, the Economic Commission for Latin America and the Caribbean (ECLAC) reported a robust 55.2% rise in FDI in the region.

- The construction volume in the sector witnessed a notable growth of 15.9% in 2020 and a further 3.29% in 2021. This growth was a result of South American governments prioritizing the infrastructure and construction sectors. They eased restrictions, allowing construction, maintenance, and project development activities in private and public ventures. This move aimed to meet crucial milestones, deadlines, and economic recovery goals.

- The commercial sector in South America is projected to witness robust growth in new floor area construction, registering a CAGR of 4% in volume during the forecast period (2023 to 2030). The region is witnessing a notable shift in its commercial construction landscape. Notable projects like the Paulinia Data Center and Porto Alegre Data Center I, initiated in 2023, are among the largest in the region. Additionally, investors are eyeing office buildings, shopping centers, and logistic parks in Brazil, which are expected to fuel market demand in the coming years.

Affordable housing schemes and subsidies in South America to influence higher construction in the residential sector

- In 2022, the residential sector in South America witnessed a 3.35% surge in new floor area construction compared to the previous year. However, Argentina saw a notable decline of 9.16% in this metric. In 2023, the sector was projected to maintain its growth trajectory, with a construction volume expected to be 3.3% higher than in 2022. This growth can be attributed to factors like increasing urbanization, rising per capita income, and overall economic expansion, all of which are fueling the demand for housing.

- Amidst the backdrop of the COVID-19 pandemic in 2020, South America saw a significant uptick of 11.83% in new floor area construction compared to the previous year. This was a deliberate move by the South American government, which prioritized the construction sector to mitigate the economic downturn and support workers, given the sharp decline in household incomes. Consequently, restrictions on construction activities, including quarantines, were eased.

- Several South American nations are rolling out initiatives to make housing more affordable for their growing populations. For example, in February 2023, Brazil relaunched its nationwide federal housing program, targeting low-income individuals. In October 2023, the World Bank approved a USD 100 million financing package for Ecuador, specifically aimed at bolstering affordable and resilient housing. Bolivia's efforts to ramp up the supply of low-cost housing and maintain reasonable prices are poised to further stoke the demand for residential spaces. As a result, the residential sector in South America is projected to witness a CAGR volume of 4.09% during the forecast period (2023-2030).

South America Construction Chemicals Industry Overview

The South America Construction Chemicals Market is fragmented, with the top five companies occupying 26.38%. The major players in this market are Arkema, MBCC Group, RPM International Inc., Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ardex Group

- 6.4.2 Arkema

- 6.4.3 CEMEX, S.A.B. de C.V.

- 6.4.4 Fosroc, Inc.

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Kryton International Inc.

- 6.4.7 LATICRETE International, Inc.

- 6.4.8 MAPEI S.p.A.

- 6.4.9 MBCC Group

- 6.4.10 MC-Bauchemie

- 6.4.11 Normet

- 6.4.12 RPM International Inc.

- 6.4.13 Saint-Gobain

- 6.4.14 Selena Group

- 6.4.15 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms