NMC電池パック:市場シェア分析、産業動向・統計、成長予測(2025年~2029年)

NMC Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029)- 発行日

- ページ情報

- 英文 335 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683881

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

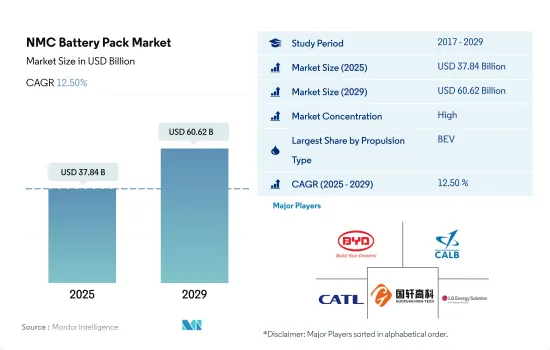

NMC電池パックの市場規模は2025年に378億4,000万米ドルと推定され、2029年には606億2,000万米ドルに達すると予測され、予測期間中(2025-2029年)のCAGRは12.50%で成長すると予測されます。

電気自動車へのシフトに伴い、NMC電池の需要が増加

- 世界各国の電動モビリティはここ数年で大きく成長し、様々なタイプの電池需要にプラスの影響を与えています。NMC電池タイプは、BEVやPHEVで様々な自動車メーカーに採用されています。しかし、この電池タイプは徐々に成長しており、主な需要は欧州メーカーから来ています。政府の厳しい規制と近い将来の化石燃料車の禁止の結果、人々はBEVとPHEVを選ぶようにシフトしています。これらの要因により、NMC電池タイプは2021年に世界全体で2017年比109.56%の成長を記録しました。

- PHEVおよびBEV用NMC電池の主な需要は、NMC電池の著名なユーザーの1つであるイタリアなどの欧州諸国からもたらされ、BEVおよびPHEVにおける電池使用量全体の25%以上を占め、フランス、ドイツがこれに続きます。アジア太平洋や北米などの様々な地域でも、BEVとPHEVの需要が大きく伸びており、世界のNMC電池の需要拡大に貢献しています。その結果、電気自動車に使用されるNMC電池は、2022年に世界全体で2021年比115.66%の成長を遂げました。

- さまざまな自動車メーカーが、電池業界の強化が期待される新製品を発表しています。2022年11月、アウディは新型バッテリー電気SUV「q8 e-tron」を欧州市場向けに発売しました。同車は114kWhのNMC電池を搭載し、1回の充電で600kmの航続距離を実現します。このような他国での発売により、予測期間中、BEVとPHEVにおけるNMC電池の需要と販売が世界的に加速すると予想されます。

EVの成長と消費者の性能重視車へのシフトが見られる

- NMCを含む数種類の電池の需要は、近年幅広い国々で急速に進む自動車の電動化の影響を受けています。歴史的な期間におけるEVの著しい成長は、政府による電気自動車に対する厳しい基準の導入、従来の燃料自動車に対するEVの多くの利点、政府による補助金、減税、リベートに起因します。急速充電と高密度バッテリーを搭載した自動車を選ぶ人が増えたため、NMC電池の需要が高まりました。このため、NMC電池の需要は2017~2023年にかけて世界全体で109.56%増加し、その大部分は南北アメリカと欧州からの需要です。

- 電気自動車は、電池パック販売全体におけるNMC電池の需要に大きく貢献している1つであり、小型トラックとバスがこれに続きます。世界各国における2022年のEV需要の伸びは、電池需要を増加させ、主に中国と米国が2022年に約70%牽引しました。その結果、NMC EVバッテリーパックの世界需要は2022年に前年比115.78%の伸びを示しました。イタリアやタイなど、さまざまな新興市場がEVの販売を増やすと予想されており、近い将来、世界的にNMC電池の需要がさらに高まるとみられます。

- 世界的に、多くの企業がゼロ・エミッション目標をサポートするために様々な目標を設定しています。2023年4月、アメリカの自動車メーカーであるフォードは、2023年末までに60万台、2026年末までに200万台の電気自動車を生産する計画を発表しました。各国のこうした目標は、2024~2029年の間にNMC電池の需要を促進すると予想されます。

NMC電池パック市場動向

BYDとテスラがEV市場をリードし、未来を形作る

- 2022年、BYDは電気自動車販売で市場をリードし、13.3%のシェアを占めました。BYDの主導的地位にはいくつかの要因があります。BYDは、電気自動車と関連技術の生産に重点を置き、EV業界で早くから有力なプレーヤーとして活躍してきました。BYDは早くから市場に参入していたため、確固たる基盤を築き、消費者の間で認知されるようになりました。BYDはまた、積極的に世界に事業を拡大し、パートナーシップを結び、研究開発に投資しており、これらすべてが主導的地位に貢献しています。

- テスラは電気自動車の技術革新の最前線に立ち、EVの世界の普及に重要な役割を果たしてきました。テスラは2022年のEV業界において、12.2%の市場シェアを持つ重要なプレーヤーでした。テスラの強力なブランドイメージ、最先端技術、広範なスーパーチャージャー・ネットワークがその成功に寄与しています。

- EV市場のその他の主要企業の中にも、大きな市場シェアを持つ企業がいくつかあります。BMWは、サブブランド「BMW i」による電動モビリティへのコミットメントと相まって、自動車業界における定評を確立しており、市場での存在感を高めています。同様に、2022年に3.9%の市場シェアを占めたフォルクスワーゲンは、「フォルクスワーゲン・グループ」傘下で電動モビリティに積極的に投資しています。これらの企業は、メルセデス・ベンツ、起亜自動車、現代自動車といった他の企業とともに、既存のブランド認知度を活用し、魅力的な電気自動車モデルを投入し、電気自動車の航続距離と性能を向上させる技術に投資することで、EV業界を再植民地化しています。

テスラとBYDが2022年のベストセラーEVモデルを独占

- 2022年に最も売れたEVモデルは、2つの主要OEMが独占した:テスラとBYDです。テスラはModel YとModel 3の2モデルでそれぞれ1位と3位を獲得し、市場で確固たる地位を築いた。テスラのモデルYは最も人気のあるプラグイン電気自動車で、2022年の世界販売台数は約77万1,300台でした。同年、テスラのモデル3とモデルYの販売台数は120万台を突破し、テスラのベストセラーモデルは前年比36.77%増となりました。プラグイン電気自動車(PEV)のベストセラー5モデルのうち2モデルはテスラブランドだったが、バッテリー電気自動車メーカーは2022年にアジアブランドとの競争に直面しました。中国を拠点とするBYDは、プラグイン・ハイブリッド電気自動車モデルの豊富なラインアップを武器に、2022年にテスラを抜いてPEVのベストセラー・ブランドとなりました。テスラ・モデルYに僅差で続いたのは、BYDソング・プラス(BEV+PHEV)で、販売台数は47万7,090台に達し、2位の座を確保しました。BYDは中国市場で確固たる地位を確立しており、信頼性が高く技術的に先進的な電気自動車を生産しているという評判が、Song Plusモデルの好調な販売実績に貢献したと思われます。

- フォルクスワーゲンID.4は、欧州のPEV(プラグイン電気自動車)の中で唯一トップ10に入り、ベストセラーEVモデルの中で際立っていました。2022年の販売台数は17万4,090台で、ID.4はフォルクスワーゲンの電動モビリティに対するコミットメントと、EV市場におけるプレゼンスの高まりを実証しました。

- 全体として、TeslaとBYDのこれら上位のEVモデル、およびWuling Hong Guang MINI EVやVolkswagen ID.4などの他の注目すべき競合モデルは、電気自動車に対する消費者の需要が高まっていることを示しています。

NMC電池パック業界の概要

NMC電池パック市場はかなり統合されており、上位5社で78.67%を占めています。この市場の主要企業は以下の通りです。BYD Company Ltd., China Aviation Battery(CALB), Contemporary Amperex Technology(CATL), Guoxuan High-tech and LG Energy Solution Ltd.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 電気自動車販売台数

- OEM別電気自動車販売台数

- 売れ筋EVモデル

- 選好されるバッテリーケミストリーを持つOEM

- 電池パック価格

- 電池材料コスト

- 各バッテリーケミストリーの価格表

- 誰が誰に供給するか

- EVバッテリーの容量と効率

- EVの発売モデル数

- 規制の枠組み

- ベルギー

- ブラジル

- 中国

- コロンビア

- フランス

- ドイツ

- ハンガリー

- インド

- インドネシア

- 日本

- ポーランド

- タイ

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車体タイプ

- バス

- LCV

- M&HDT

- 乗用車

- 推進タイプ

- BEV

- PHEV

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 80kWh以上

- 15kWh未満

- バッテリー形状

- 円筒形

- パウチ

- 角型

- 方式

- レーザー

- ワイヤー

- コンポーネント

- アノード

- カソード

- 電解液

- セパレーター

- 材料タイプ

- コバルト

- リチウム

- マンガン

- 天然黒鉛

- ニッケル

- その他の材料

- 地域

- アジア太平洋

- 国別

- 中国

- インド

- 日本

- 韓国

- タイ

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- ハンガリー

- イタリア

- ポーランド

- スウェーデン

- 英国

- その他欧州

- 中東&アフリカ

- 北米

- 国別

- カナダ

- 米国

- 南米

- アジア太平洋

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BYD Company Ltd.

- China Aviation Battery Co. Ltd.(CALB)

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Guoxuan High-tech Co. Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Primearth EV Energy Co. Ltd.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- SVOLT Energy Technology Co. Ltd.(SVOLT)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The NMC Battery Pack Market size is estimated at 37.84 billion USD in 2025, and is expected to reach 60.62 billion USD by 2029, growing at a CAGR of 12.50% during the forecast period (2025-2029).

NMC battery demand is rising with a shift toward battery electric passenger cars

- Electric mobility in various countries globally has grown significantly over the past few years, positively impacting the demand for various types of batteries. NMC battery type is being opted for by various auto manufacturers in BEV and PHEV. However, the battery type is growing gradually, and major demand is coming from European manufacturers. As a result of the government's stringent norms and banning of fossil fuel vehicles in the near future, people are shifting to opt for BEVs and PHEVs. Due to these factors, the NMC battery type registered a growth of 109.56% in 2021 over 2017 globally.

- The major demand for NMC batteries for PHEV and BEV comes from European countries such as Italy, one of the prominent users of NMC batteries, accounting for more than 25% of overall battery usage in BEV and PHEV, followed by France and Germany. Various regions, such as Asia-Pacific and North America, are also witnessing a significant growth in the demand for BEV and PHEV, contributing to the growth of NMC battery demand globally. As a result, NMC batteries used in electric vehicles grew by 115.66% in 2022 over 2021 globally.

- Various automakers are launching new products expected to enhance the battery industry. In November 2022, Audi launched its all-new battery electric SUV q8 e-tron for the European market. The car is equipped with a 114 kWh NMC battery, offering a range of 600 km on a single charge. Such launches in other countries are expected to accelerate the demand and sales of the NMC batteries in BEV and PHEV during the forecast period globally.

There is growth in EVs and a shift in consumers toward performance-oriented vehicles

- The demand for several kinds of batteries, including NMC, was affected by the rapid increase in the electrification of vehicles in recent years across a wide range of countries. The tremendous growth of EVs during the historical period can be attributed to the introduction of stringent norms by the government for electric vehicles, the many advantages of EVs over conventional fuel vehicles, and government subsidies, tax offs, and rebates. The demand for NMC batteries has risen as more people choose vehicles with fast-charging and high-density batteries. This led to a global rise in the demand for NMC batteries of 109.56% over 2017-2023, with the demand mostly from the Americas and Europe.

- Electric cars are one of the major contributors to the demand for NMC batteries in the overall battery pack sales, followed by light trucks and buses. The growth in the demand for EVs in 2022 in various countries globally increased the demand for batteries, majorly driven by China and the United States by around 70% in 2022. As a result, the global demand of NMC EV battery packs witnessed a growth of 115.78% in 2022 over the previous year. Various emerging markets, such as Italy and Thailand, are expected to increase the sales of EVs, which further will increase the demand for NMC batteries in the near future globally.

- Globally, many companies are setting various objectives to support the zero-emission goal. In April 2023, the American automaker Ford announced plans to produce 600,000 electric vehicles by the end of 2023 and 2 million vehicles by the end of 2026. Such objectives in various countries are expected to drive the demand for NMC batteries during 2024-2029.

NMC Battery Pack Market Trends

BYD AND TESLA ARE LEADING THE CHARGE IN THE EV MARKET AND SHAPING THE FUTURE

- In 2022, BYD was the market leader in electric vehicle sales and held a share of 13.3%. BYD's leading position can be attributed to several factors. It has been an early and prominent player in the EV industry, with a strong focus on producing electric vehicles and related technologies. The company's early entry into the market allowed it to establish a solid foundation and gain recognition among consumers. BYD has also been actively expanding its operations globally, forging partnerships, and investing in research and development, all of which contribute to its leading position.

- Tesla has been at the forefront of electric vehicle innovation and has played a crucial role in popularizing EVs worldwide. Tesla was a significant player in the EV industry in 2022, with a market share of 12.2%. Tesla's strong brand image, cutting-edge technology, and extensive Supercharger network have contributed to its success.

- Among the other players in the EV market, there are several notable companies that hold significant market shares. BMW's established reputation in the automotive industry, coupled with its commitment to electric mobility through its "BMW i" sub-brand, has contributed to its market presence. Similarly, Volkswagen, which held a market share of 3.9% in 2022, has been actively investing in electric mobility under its "Volkswagen Group" umbrella. These companies, along with others like Mercedes-Benz, Kia, and Hyundai, are recolonizing the EV industry by leveraging their existing brand recognition, introducing compelling electric vehicle models, and investing in technology to enhance the range and performance of their electric offerings.

TESLA AND BYD DOMINATED THE BEST-SELLING EV MODELS OF 2022

- The best-selling EV models in 2022 were dominated by two key OEMs: Tesla and BYD. Tesla held a strong market position with two of its models, the Model Y and Model 3, capturing the first and third spots, respectively. The Tesla Model Y was the most popular plug-in electric vehicle, with global unit sales of roughly 771,300 in 2022. That year, deliveries of Tesla's Model 3 and Model Y surpassed 1.2 million, a Y-o-Y increase of 36.77% for Tesla's best-selling models. While two of the five best-selling plug-in electric vehicle (PEV) models were Tesla-branded, the battery electric vehicle manufacturer faced competition from Asian brands in 2022. China-based BYD overtook Tesla as the best-selling PEV brand in 2022, relying on a large offering of plug-in hybrid electric models. Following closely behind the Tesla Model Y, the BYD Song Plus (BEV + PHEV) secured the second spot, with sales reaching 477,090 units. BYD's established presence in the Chinese market, along with its reputation for producing reliable and technologically advanced electric vehicles, likely contributed to the strong sales performance of the Song Plus models.

- The Volkswagen ID.4 stood out among the best-selling EV models as the only European PEV (Plug-in Electric Vehicle) in the top ten. With a sales volume of 174,090 units in 2022, the ID.4 demonstrated Volkswagen's commitment to electric mobility and its growing presence in the EV market.

- Overall, these top-performing EV models from Tesla and BYD, along with other notable contenders like the Wuling Hong Guang MINI EV and Volkswagen ID.4, demonstrate the increasing consumer demand for electric vehicles.

NMC Battery Pack Industry Overview

The NMC Battery Pack Market is fairly consolidated, with the top five companies occupying 78.67%. The major players in this market are BYD Company Ltd., China Aviation Battery Co. Ltd. (CALB), Contemporary Amperex Technology Co. Ltd. (CATL), Guoxuan High-tech Co. Ltd. and LG Energy Solution Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 Brazil

- 4.11.3 China

- 4.11.4 Colombia

- 4.11.5 France

- 4.11.6 Germany

- 4.11.7 Hungary

- 4.11.8 India

- 4.11.9 Indonesia

- 4.11.10 Japan

- 4.11.11 Poland

- 4.11.12 Thailand

- 4.11.13 UK

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Capacity

- 5.3.1 15 kWh to 40 kWh

- 5.3.2 40 kWh to 80 kWh

- 5.3.3 Above 80 kWh

- 5.3.4 Less than 15 kWh

- 5.4 Battery Form

- 5.4.1 Cylindrical

- 5.4.2 Pouch

- 5.4.3 Prismatic

- 5.5 Method

- 5.5.1 Laser

- 5.5.2 Wire

- 5.6 Component

- 5.6.1 Anode

- 5.6.2 Cathode

- 5.6.3 Electrolyte

- 5.6.4 Separator

- 5.7 Material Type

- 5.7.1 Cobalt

- 5.7.2 Lithium

- 5.7.3 Manganese

- 5.7.4 Natural Graphite

- 5.7.5 Nickel

- 5.7.6 Other Materials

- 5.8 Region

- 5.8.1 Asia-Pacific

- 5.8.1.1 By Country

- 5.8.1.1.1 China

- 5.8.1.1.2 India

- 5.8.1.1.3 Japan

- 5.8.1.1.4 South Korea

- 5.8.1.1.5 Thailand

- 5.8.1.1.6 Rest-of-Asia-Pacific

- 5.8.2 Europe

- 5.8.2.1 By Country

- 5.8.2.1.1 France

- 5.8.2.1.2 Germany

- 5.8.2.1.3 Hungary

- 5.8.2.1.4 Italy

- 5.8.2.1.5 Poland

- 5.8.2.1.6 Sweden

- 5.8.2.1.7 UK

- 5.8.2.1.8 Rest-of-Europe

- 5.8.3 Middle East & Africa

- 5.8.4 North America

- 5.8.4.1 By Country

- 5.8.4.1.1 Canada

- 5.8.4.1.2 US

- 5.8.5 South America

- 5.8.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BYD Company Ltd.

- 6.4.2 China Aviation Battery Co. Ltd. (CALB)

- 6.4.3 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.4 Guoxuan High-tech Co. Ltd.

- 6.4.5 LG Energy Solution Ltd.

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Primearth EV Energy Co. Ltd.

- 6.4.8 Samsung SDI Co. Ltd.

- 6.4.9 SK Innovation Co. Ltd.

- 6.4.10 SVOLT Energy Technology Co. Ltd. (SVOLT)

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 335 Pages

- 納期

- 2~3営業日