|

市場調査レポート

商品コード

1683843

英国の代替乳製品:市場シェア分析、産業動向、成長予測(2025年~2030年)United Kingdom Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の代替乳製品:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

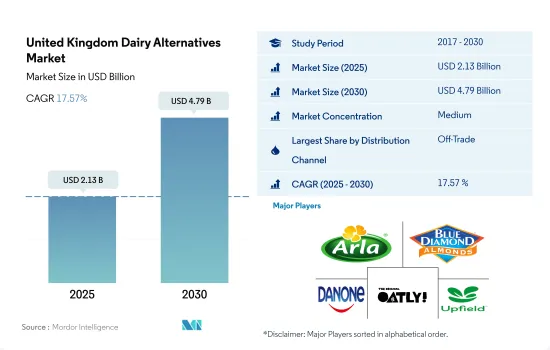

英国の代替乳製品市場規模は2025年に21億3,000万米ドルと推定され、2030年には47億9,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは17.57%で成長すると予測されます。

市場はオンライン小売チャネルが牽引する非乳製品販売の持続的成長によって牽引される

- 英国の代替乳製品市場の流通チャネルを支配しているのは、オフトレードセグメントです。主にハイパーマーケットとスーパーマーケットが非売品チャネルの高い市場シェアを牽引しています。スーパーマーケットとハイパーマーケットは、調査対象市場における代替乳製品の販売で常に強力なリードを維持しています。これらのチャネルは、特に大都市や開発途上都市において、消費者が市場で入手可能な多種多様な商品の中から購入するかどうかの意思決定に影響を与えるという付加的な利点を提供しています。英国では、スーパーマーケットとハイパーマーケットが2022年の代替乳製品販売額の72%を占めています。

- 全国のオン・トレード・チャネルを通じた代替乳製品の販売額は、2021年から2022年にかけて31%増加しました。流通チャネルに基づくと、英国における2023年の消費量は1人当たり約0.15kgで、2021年の代替乳製品の消費量は1人当たり0.13kgでした。オン・トレード・チャネルは、2024年~2027年の間に60%の成長率を記録しそうです。

- 現代の消費者は多忙なライフスタイルのため食料品のオンライン購入を好むため、オンライン小売チャネルが最も急成長する流通チャネルになると予測されます。代替乳製品のオンライン販売は、2021年~2023年の間に56.8%成長し、2023年の市場価値は3,340万米ドルに達すると予想されます。2022年には、インターネットにアクセスできる家庭の割合は2011年の72%から93%に増加しました。英国は他の国々と同様、インターネット・ユーザーの普及率が高いです。例えば、主なオンライン・チーズ小売業者には、FROMAGES.COM、The East London Cheese Board、La Gourmeta、Love Cheese、Italia Regina、Frank and Salなどがあります。オンライン小売チャネルの販売額は、2024年から2027年の間に87%の成長率を記録すると予測されています。

英国の代替乳製品市場動向

植物性タンパク質への嗜好の高まりと植物性乳製品消費拡大のための政府支援が需要を押し上げる

- 同国ではあらゆる年齢層で代替乳製品の消費が増加しています。植物性乳製品への需要は、菜食主義の拡大が牽引しています。英国の消費者の約9%が植物性食品(ヴィーガン+ベジタリアン)を食べており、これは欧州ではドイツに次いで高いです。植物性食品の中では、植物性牛乳(週に1回以上26%)、植物性牛肉(週に1回以上24%)、植物性鶏肉(週に1回以上23%)が最も頻繁に消費されています。

- 植物性チーズに関しては、英国の消費者は、スーパーマーケットで購入できる植物性スライスチーズ(38%)と植物性モッツァレラチーズ(36%)を特に好んで消費しています。英国では、植物由来の乳製品部門は植物由来の肉製品部門よりも小さいが、成長率は植物由来の牛乳と植物由来のチーズの方が高いです。植物性タンパク質に対する消費者の志向の高まりは、同国における代替乳製品の消費を促進する重要な要因のひとつです。2022年には、英国の消費者の約60%が植物性タンパク質に関心を持っています。英国の消費者の50%以上が、植物性タンパク質食品は安全だと信頼しています。

- 29%近くが乳製品の摂取を減らす予定であり、英国の消費者の21%は2022年時点でより多くの植物性乳製品を摂取する意向です。英国の消費者の約26%は、植物性チーズを定期的に購入する可能性があります。英国政府によるいくつかの取り組みが、同国における植物性乳製品の消費を高めています。

英国代替乳製品産業の概要

英国の代替乳製品市場は適度に統合されており、上位5社で51.18%を占めています。この市場の主要企業は以下の通り。 Arla Foods, Blue Diamond Growers, Danone SA, Oatly Group AB and Upfield Holdings BV(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産

- 代替乳製品-原材料生産

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- 非乳製品バター

- 非乳製品チーズ

- 非乳製品アイスクリーム

- 非乳製品ミルク

- 製品タイプ別

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘーゼルナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 非乳製品ヨーグルト

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)。

- Arla Foods

- Blue Diamond Growers

- Britvic PLC

- Coconut Collaborative Ltd

- Danone SA

- Oatly Group AB

- Plamil Foods Ltd

- The Hain Celestial Group Inc.

- Upfield Holdings BV

- VBites Foods Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50000741

The United Kingdom Dairy Alternatives Market size is estimated at 2.13 billion USD in 2025, and is expected to reach 4.79 billion USD by 2030, growing at a CAGR of 17.57% during the forecast period (2025-2030).

Market is driven by sustainable growth in sales of non-dairy products led by online retail channels

- The off-trade segment dominates the distribution channels of the UK dairy alternatives market. Hypermarkets and supermarkets primarily drive the high market share of off-trade channels. Supermarkets and hypermarkets have always maintained a strong lead in the sales of dairy alternatives in the market studied. The proximity factor of these channels, especially in large and developed cities, provides them with an added advantage of influencing the consumer's decision to purchase among the large variety of products available in the market. In the United Kingdom, supermarkets and hypermarkets held 72% of dairy alternatives sales, by value, in 2022.

- The sales value of dairy alternatives through on-trade channels across the country increased by 31% during 2021-2022. Based on the distribution channel, the consumption in the United Kingdom was around 0.15 kg per person in 2023, with 0.13 kg/per capita consumption of dairy alternatives in 2021. The on-trade channel is likely to record a growth rate of 60% during 2024-2027.

- The online retail channel is projected to be the fastest-growing distribution channel as modern consumers prefer online grocery purchases due to their busy lifestyles. Online sales of dairy alternatives are expected to grow by 56.8% during 2021-2023 to reach a market value of USD 33.4 million in 2023. In 2022, the share of households with internet access was recorded at 93%, up from 72% in 2011. The United Kingdom, along with other countries, has a high penetration of internet users. For instance, the key online cheese retailers include FROMAGES.COM, The East London Cheese Board, La Gourmeta, Love Cheese, Italia Regina, and Frank and Sal. The online retail channel's sales value is anticipated to register a growth rate of 87% during 2024-2027.

United Kingdom Dairy Alternatives Market Trends

Increasing preference for plant-based protein and government support to increase plant-based dairy consumption boost the demand

- The consumption of dairy alternatives is increasing across all age groups in the country. The demand for plant-based dairy products is being driven by growing veganism. Around 9% of UK consumers are plant-based eaters (vegan+vegetarian), the highest after Germany across Europe. Among plant-based food, plant-based milk (26% at least once a week), plant-based beef (24% at least once a week), and plant-based poultry (23% at least once a week) are most frequently consumed.

- Regarding plant-based cheese, UK consumers especially like to consume plant-based sliced cheese (38%) and plant-based mozzarella (36%) available in supermarkets. The plant-based dairy sector is smaller than the plant-based meat sector in the United Kingdom, but growth rates are higher for plant-based milk and plant-based cheese. Increasing consumer inclination toward plant-based protein is one of the key factors driving the consumption of dairy alternatives in the country. Around 60% of UK consumers were interested in plant-based proteins in 2022. More than 50% of UK consumers trust that plant-based protein food is safe.

- Nearly 29% plan on consuming less dairy, and 21% of UK consumers intend to consume more plant-based dairy products as of 2022. About 26% of UK consumers are likely to purchase plant-based cheese regularly. Several initiatives by the UK government are raising the consumption of plant-based dairy in the country.

United Kingdom Dairy Alternatives Industry Overview

The United Kingdom Dairy Alternatives Market is moderately consolidated, with the top five companies occupying 51.18%. The major players in this market are Arla Foods, Blue Diamond Growers, Danone SA, Oatly Group AB and Upfield Holdings BV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Non-Dairy Butter

- 5.1.2 Non-Dairy Cheese

- 5.1.3 Non-Dairy Ice Cream

- 5.1.4 Non-Dairy Milk

- 5.1.4.1 By Product Type

- 5.1.4.1.1 Almond Milk

- 5.1.4.1.2 Cashew Milk

- 5.1.4.1.3 Coconut Milk

- 5.1.4.1.4 Hazelnut Milk

- 5.1.4.1.5 Hemp Milk

- 5.1.4.1.6 Oat Milk

- 5.1.4.1.7 Soy Milk

- 5.1.5 Non-Dairy Yogurt

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arla Foods

- 6.4.2 Blue Diamond Growers

- 6.4.3 Britvic PLC

- 6.4.4 Coconut Collaborative Ltd

- 6.4.5 Danone SA

- 6.4.6 Oatly Group AB

- 6.4.7 Plamil Foods Ltd

- 6.4.8 The Hain Celestial Group Inc.

- 6.4.9 Upfield Holdings BV

- 6.4.10 VBites Foods Ltd

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms