北米のホエイたんぱく質成分:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America Whey Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 226 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683496

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

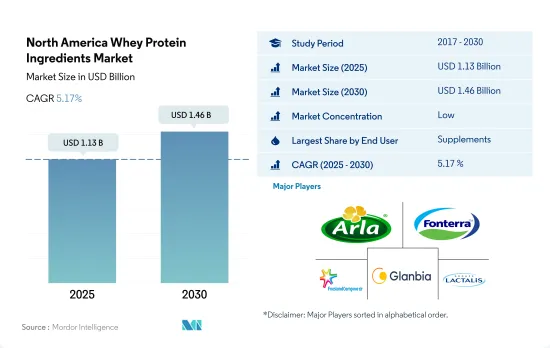

北米のホエイたんぱく質成分市場規模は2025年に11億3,000万米ドルと推定・予測され、2030年には14億6,000万米ドルに達し、予測期間(2025-2030年)のCAGRは5.17%で成長すると予測されます。

企業による戦略的投資とフィットネス意識の高い消費者の増加が、特にサプリメントとF&B分野でのホエイたんぱく質成分の応用を促進します。

- 北米ホエイプロテイン市場の最大の用途分野はF&Bとサプリメントです。スナックがF&Bセグメントを支配し、2022年の数量シェアは48.44%を占めました。Nestle、Arla Foods、Fonterra Groupなどの主要企業は、スナック業界の需要急増に対応するため、製品配合に広く投資しています。サプリメント分野では、スポーツ栄養が2022年に数量ベースで94.6%の主要シェアを占めました。この成長は、筋肉増強サプリメントとしてフィットネス業界でホエイプロテインの需要が増加していることに起因しています。2021年、カナダでは約618万人の会員がジムに登録しており、i.e.当たりおよそ938人の会員がいます。

- 飲料のサブセグメントは、予測期間中、金額ベースで最も速いCAGR 3.37%を記録すると予測され、次いで調味料/ソースが続きます。優れた栄養特性、ニュートラルな風味、消化のしやすさ(毎時10g)、飲料システムにおける特徴的な機能性により、乳清タンパク質はRTDプロテイン飲料のタンパク質源として頻繁に使用されています。WPCは、pH4.4で等電点を維持することによる乳化など、優れた脂肪代替特性を提供し、ドレッシングやソースなどでの使用を後押ししています。

- 最も急成長しているエンドユーザー分野はパーソナルケアと化粧品で、予測期間中にCAGR 4.74%を記録すると予測されています。これは、美容クリニックの数の増加と、身だしなみに対する一人当たりの支出の増加によるものです。米国のパーソナルケアとサービスに対する平均収入と支出は、2020-2021年の間に19.3%増加しました。ホエイ・プロテインは、ホエイ・プロテインに含まれるアミノ酸の助けを借りて、肌の弾力性や髪のコンディショニングといった機能性を高めており、これが同セグメントにおける需要を押し上げています。

米国は、様々な食品製造ユニットの強力な存在により、2022年にはシェアの大半を占めました。

- 米国は、高い消費者ベースと大規模な食品製造ユニットの設立に起因して、2022年に最大のシェアで北米市場をリードしました。大手企業による生産統合により、ホエイプロテインへのアクセスが容易になり、市場競争が激化しています。米国のホエイプロテイン市場は、飲食品分野(51.6%)が大きなシェアを占め、2022年にはサプリメント分野(47.6%)がそれに続きます。ホエイ・プロテインは、他のタンパク質と比較して、天然タンパク質源の優れた、分岐鎖アミノ酸含有量を有します。ホエイ・プロテインは用量依存的に筋タンパク質合成を刺激することができます。

- カナダは2022年も第2位の市場規模を維持したが、これはサプリメント・セグメントにおけるタンパク質消費の高さが要因です。カナダはホエイプロテインの新興市場です。同国では健康食の動向が活況を呈しており、ホエイ・プロテインなどの原料に大きな需要が生じています。ホエイプロテインの使用は、フィットネス愛好家やフィットネスクラブの増加により、主にスポーツ栄養で観察されました。カナダのスポーツ栄養分野は、予測期間中にCAGR 5.39%を記録すると予測されています。カナダのプロテイン市場では酪農産業が優位を占めており、ホエイプロテイン市場に良好な成長機会をもたらしています。

- メキシコは北米におけるホエイプロテインの急成長国で、予測期間中のCAGRは6.11%と予測されます。メキシコでは、機能性食品とベーカリー産業が活況を呈しており、乳製品原料の需要が急増しています。ホエイプロテイン入りのプロテインバーは、その機能的特性から消費者の間で人気となっており、市場を牽引しています。

北米のホエイたんぱく質成分市場動向

スポーツ/パフォーマンス栄養が予測期間中に大幅な成長を遂げる

- 北米の植物性タンパク質ベースのスポーツ栄養市場は、2016年から2019年にかけて金額で23.65%成長しました。2020年には、前年比成長率で3.35%の急減を示しました。この減少は、米国、カナダ、メキシコなどの主要国におけるロックダウンやCOVID-19関連の規制によるジムの閉鎖に起因します。例えば、サプリメントの一般的な販売チャネルの1つであるヘルスクラブは、パンデミックがフィットネスクラブの経営者、従業員、消費者に厳しい打撃を与えたため、サプリメントの販売に悪影響を与えました。2020年、米国ではフィットネス施設の17%以上が永久閉鎖となりました。

- 北米は世界有数のスポーツ・パフォーマンス栄養市場であり、その背景にはアスリート志向の高まりと健康意識の高まりがあります。健康効果のある新しいフレーバーのイノベーションは、予測期間(2023-2029年)中に18%の市場成長をサポートすると予測されます。消費者の栄養維持志向の高まりは、植物性タンパク質の需要を押し上げています。強化オーガニック製品も2019年から2021年にかけて約40%の成長を示しました。

- 北米では、コアユーザーやアクティブなライフスタイルを送る消費者からスポーツ栄養製品の需要が急速に高まっています。ライトユーザーは、エネルギー、体重管理、筋肉サポート、健康的な間食に重点を置いたスポーツ栄養アイテムを消費しています。筋肉の成長、筋力パフォーマンス、持久力、回復に不可欠なスポーツサプリメントは、主にコアユーザーやヘビーユーザーに好まれています。例えば、2021年、米国内では、ユーザーの41.7%がプロテイン製品を摂取しており、植物ベースの食事への嗜好が2019年から2020年にかけて27%増加したため、植物性プロテインの売上を押し上げています。

ドライホエイ生産量の増加が予測期間中のホエイプロテイン価格を安定させる

- 米国はこの地域における主要なドライホエイ生産国です。ホエー生産は主にチーズ生産工場からの供給が牽引しており、同国の液体ホエー生産の大半を占めています。2022年4月現在、米国には500を超えるチーズ生産工場があります。ホエイパウダーがホエイ製品市場を独占し、WPCが僅差で続きます。2021年には、国内で約9億3,400万ポンドの乾燥ホエーが生産されます。

- 大手企業はホエイ工場の増設に取り組んでいます。スポーツおよびパフォーマンス栄養製品は、ハイエンドタンパク質原料分野の力強い成長を牽引しています。WPCは、チーズ加工に由来する低温殺菌ホエーから、一定割合の非タンパク質成分を除去して製造されます。食用に利用可能なWPCの最終製品は、ホエイ蛋白質を34%以上含むWPC34と、蛋白質を80%以上含むWPC80です。

- 2020年、パンデミックの影響で全国的に生産工場が閉鎖されたため、ホエー全体の生産量は減少しました。ドライホエイの生産量は約9億5,100万ポンドで、2.7%減少しました。WPCの生産量は約4億7,800万ポンドで、2019年の生産量から2.7%減少しました。逆に、ミルク工場の生産量はパニック買いにより急増し、2020年4月以降は安定しました。飼料セクター向けドライホエイの生産は、価格が横ばいのため安定しています。WPCの生産は安定しているが、一部の市場関係者は今後数四半期で高濃度WPCの価格が上昇すると予想しており、生産にプラスの影響を与えそうです。

北米のホエイたんぱく質成分産業概要

北米のホエイたんぱく質成分市場は細分化されており、上位5社で27.29%を占めています。この市場の主要企業は以下の通りです。 Arla Foods amba, Fonterra Co-operative Group Limited, FrieslandCampina Ingredients, Glanbia PLC and Groupe Lactalis(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場数量

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 加水分解物

- 分離物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品及び乳製品代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Agropur Dairy Cooperative

- Arla Foods amba

- Carbery Food Ingredients Limited

- Cooke Inc.

- Fonterra Co-operative Group Limited

- FrieslandCampina Ingredients

- Glanbia PLC

- Groupe Lactalis

- Hilmar Cheese Company Inc.

- Milk Specialties Global

- Saputo Inc.

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Whey Protein Ingredients Market size is estimated at 1.13 billion USD in 2025, and is expected to reach 1.46 billion USD by 2030, growing at a CAGR of 5.17% during the forecast period (2025-2030).

Strategic investments by companies, coupled with growing fitness-conscious consumers, driving the application of whey protein ingredients, especially in the supplements and F&B segments

- The North American whey protein market's largest application segments are the F&B and supplements segments. Snacks dominated the F&B segment, accounting for a 48.44% volume share in 2022. Key players like Nestle, Arla Foods, and Fonterra Group are widely investing in product formulations to cater to the snack industry's surge in demand. In the supplements segment, sports nutrition held a major share of 94.6% by volume in 2022. The growth can be attributed to the increasing demand for whey protein in the fitness industry as a muscle-building supplement. In 2021, Canada had about 6.18 million members registered in the gym, i.e., roughly 938 members per gym.

- The beverage sub-segment is projected to register with the fastest CAGR of 3.37% by value during the forecast period, followed by condiments/sauces. Owing to its superior nutritional attributes, neutral flavor, ease of digestion (10g/hr), and distinctive functioning in beverage systems, whey protein is frequently used as the protein source for RTD protein beverages. WPC offers excellent fat replacement properties, such as emulsification by maintaining an isoelectric point at pH 4.4, boosting its use in dressings, sauces, etc.

- The fastest-growing end-user segment is personal care and cosmetics, which is projected to register a CAGR of 4.74% over the forecast period. This is due to the rising number of beauty clinics and rising per capita spending on personal appearance. The average income and expenditure on personal care and services in the United States increased by 19.3% during 2020-2021. Whey protein has increased functionalities, like skin elasticity and hair conditioning, with the help of amino acids found in whey protein, which is boosting its demand in the segment.

The United States held a majority of the share in 2022 due to the strong presence of various food manufacturing units

- The United States led the North American market with the largest share in 2022, attributed to a high consumer base and the extensive food manufacturing units being established. The production consolidation practiced by major players results in easy accessibility and competitive whey protein prices, boosting market value. The whey protein market in the United States is highly driven by the food and beverage segment (51.6%), which held a significant share, followed by the supplements segment (47.6%) in 2022. Whey protein has a superior, branched-chain amino acid content of natural protein sources compared to other proteins. It can stimulate muscle protein synthesis in a dose-dependent manner.

- Canada remained the second-largest market in 2022, driven by high protein consumption in the supplements segment. Canada is an emerging market for whey protein. The booming trend of healthy food in the country has created significant demand for ingredients such as whey protein. Whey protein usage was mainly observed in sports nutrition due to the increasing number of fitness enthusiasts and fitness clubs. The Canadian sports nutrition segment is projected to register a CAGR of 5.39% during the forecast period. The dominance of the dairy industry within Canada's protein market has provided favorable growth opportunities for the whey protein market.

- Mexico is the fastest-growing country for whey protein in North America, projected to register a CAGR of 6.11% during the forecast period. The booming functional food and bakery industries spiked the demand for dairy ingredients in Mexico, with whey protein being the best alternative. Protein bars with whey protein are becoming popular among consumers due to their functional properties, thus driving the market.

North America Whey Protein Ingredients Market Trends

Sport/performance nutrition to witness significant growth during the forecast period

- The North American plant protein-based sports nutrition market grew by 23.65% in value from 2016 to 2019. In 2020, it witnessed a steep decline of 3.35% in its Y-o-Y growth rate. This decline was attributed to gym closures due to lockdowns and COVID-19-related restrictions in major countries like the United States, Canada, and Mexico. For instance, health clubs, one of the common sales channels for supplements, impacted the sales of supplements adversely as the pandemic took a harsh toll on fitness club operators, employees, and consumers. In 2020, more than 17% of fitness facilities were permanently closed in the United States.

- North America is one of the world's leading sport and performance nutrition markets, owing to the increasing trend of athleticism and rising health awareness. The innovation of new flavors with health benefits is predicted to support the market growth by 18% during the forecast period (2023-2029). The increased consumers' proclivity to maintain nutrition boosts the demand for plant proteins. Fortified organic products also witnessed a growth of around 40% from 2019 to 2021.

- In North America, the demand for sports nutrition products is rising quickly from core users and consumers who lead active lifestyles. Light users consumed sports nutrition items focused on energy, weight control, muscle support, and healthy snacking. Sports supplements essential for muscular growth, strength performance, endurance, and recovery are mainly preferred by core or heavy users. For instance, in 2021, within the United States, 41.7% of users were consuming protein products, boosting plant protein sales as the preference for a plant-based diet increased by 27% from 2019 to 2020.

Increasing dry whey production to stabilize whey protein prices during forecast period

- The United States is the major dry whey producing country in the region. Whey production is mainly driven by the supply from cheese production plants, accounting for most of the country's liquid whey production. As of April 2022, there were over 500 cheese production plants in the United States. Whey powder dominates the whey products market, closely followed by WPC. In 2021, around 934 million pounds of dry whey is produced in the country.

- Major companies are working toward securing additional whey plants. Sports and performance nutrition products drive strong growth in the high-end protein ingredients sector. WPC is produced by removing a certain percentage of non-protein constituents from pasteurized whey derived from cheese processing. The finished WPC products available for food aid are WPC34, which contains more than 34% whey protein, and WPC80, which includes more than 80% protein.

- In 2020, the overall whey production declined due to the pandemic because production plants had shut down across the nation. The production volume of dry whey was nearly 951 million pounds, down by 2.7%. The production volume of WPC was about 478 million pounds, down by 2.7% from that of 2019. On the contrary, production in milk plants witnessed a surge due to panic buying, which stabilized after April 2020. The production of dry whey for the animal feed sector is stable as prices remain unchanged. Although WPC production is stable, some market players expect higher prices for higher-concentration WPC in the next few quarters, which will likely positively impact production.

North America Whey Protein Ingredients Industry Overview

The North America Whey Protein Ingredients Market is fragmented, with the top five companies occupying 27.29%. The major players in this market are Arla Foods amba, Fonterra Co-operative Group Limited, FrieslandCampina Ingredients, Glanbia PLC and Groupe Lactalis (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 Canada

- 3.4.2 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Hydrolyzed

- 4.1.3 Isolates

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 RTE/RTC Food Products

- 4.2.2.1.7 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.3.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agropur Dairy Cooperative

- 5.4.2 Arla Foods amba

- 5.4.3 Carbery Food Ingredients Limited

- 5.4.4 Cooke Inc.

- 5.4.5 Fonterra Co-operative Group Limited

- 5.4.6 FrieslandCampina Ingredients

- 5.4.7 Glanbia PLC

- 5.4.8 Groupe Lactalis

- 5.4.9 Hilmar Cheese Company Inc.

- 5.4.10 Milk Specialties Global

- 5.4.11 Saputo Inc.

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 226 Pages

- 納期

- 2~3営業日