アジア太平洋のホエイプロテイン原料- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Asia-Pacific Whey Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 246 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690994

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

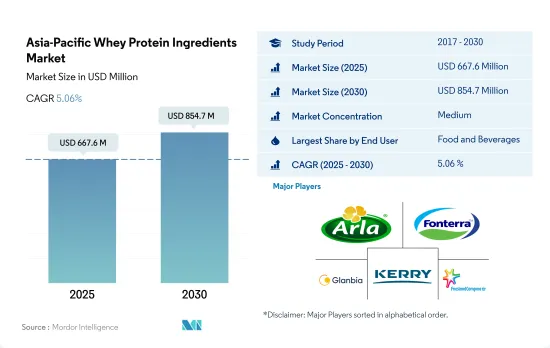

アジア太平洋のホエイプロテイン原料市場規模は、2025年には6億6,760万米ドルと推定され、2030年には8億5,470万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは5.06%で成長すると予測されます。

スナックと飲食品の消費量が市場シェアの75%以上を占め、飲食品セグメントがアジア太平洋のホエイプロテイン市場を独占しています。

- 2022年のアジア太平洋のホエイプロテイン市場は、スナックと飲料のサブセグメントによる消費が合わせて数量シェアの75%以上を占め、F&Bセグメントが支配的でした。顧客は現在、少量の食事を好んだり、従来の食事をプロテインベースのスナックバーのような、より効果的で利用しやすい代替品に置き換えたりしています。日本のF&Bセグメントでは、中食サブセグメントが最も高い成長を示し、2018年の売上高は950億米ドルでした。売上を牽引するもう一つの要因は、高プロテイン、カロリーゼロ、消化しやすいプロテインといった機能性を確認する研究が増えていることで、スナック菓子のカテゴリーで非常に望まれるプロテイン材料となっています。このため、2021年の市場成長率は金額ベースで2.79%と鈍化しました。

- F&Bセグメントは、スポーツ栄養のサブセグメントにおける用途に牽引され、サプリメントがこれに続きました。2022年にはスポーツ栄養がサプリメントセグメントを支配したが、予測期間(2023~2029年)にはベビーフードのサブセグメントが金額ベースで6.14%のCAGRを記録し、最も急成長すると予測されます。中国やインドのような国は出生率が高く、1年間に生まれる幼児の数は、インドでは年間2,400万人、中国では年間1,600万人と算出されています。この背景には、乳幼児の健康に対する関心の高まりと、これらの製品に使用されているプロテインに対する意識の向上があります。例えば、中国や香港のようなアジア太平洋諸国のヘルスクラブやジムは、2021年に1クラブ当たりの平均売上高が200万米ドルを超えました。

憂慮すべき肥満率などの健康懸念に起因するプロテイン強化食品への嗜好の高まりが地域市場を牽引しています。

- インドでは健康志向の消費者が増加しており、肥満率の増加によって健康的でプロテイン強化飲料を好む消費者が増えています。太りすぎの女性の割合は20.6%から24%に、太りすぎの男性の割合は18.9%から22.9%に増加しています。予測期間中に最も急成長を記録するのはインドで、金額ベースのCAGRは5.77%と予測されます。

- 中国は、幼児栄養、臨床食、スポーツ、ウェイトトレーニングなどの特殊製品におけるプロテインの使用量が増加しているため、2022年もトップの座を維持しました。同国では高プロテイン製品が大きな関心を集めています。2022年には、中国の消費者は約160万MTのスナックを消費します。中国は予測期間中、金額ベースで2番目に高いCAGR 4.98%を記録すると予測されます。成長を牽引するのは、プロテイン強化ミルクセーキや食事代替飲料の消費の増加であると考えられます。親和性の高い製品を発売する新規参入企業には、Smeal、ffit8、Wonderlab、Miss Zeroなどがあります。

- オーストラリアでは、調査期間中にホエイプロテインの消費が大幅に増加し、同国での利用量は数量ベースでCAGR 2.51%を記録しました。2022年、同国におけるホエイプロテインの消費量の72%はスポーツ栄養セグメントによるものであり、ベーカリーやスナックなどのエンドユーザーセグメントはそれぞれ26.6%、13.8%のシェアでした。この成長は、国内で24時間営業のジムが増加していることに起因しています。この動向が、プロテインサプリメント、特にホエイプロテインを主原料とするサプリメントの消費を刺激しています。2022年には、オーストラリアのスポーツ栄養セグメントで使用される動物性プロテインの77%以上がホエイタンパクでした。

アジア太平洋のホエイプロテイン原料市場の動向

ヘルス&フィットネスセンターの増加が市場を牽引

- 健康関連への関心の高まりとヘルスクラブの会員数拡大が産業を牽引しています。フィットネスクラブ/ヘルスクラブの増加は、消費者の利用可能性とその関与率をさらに促進します。例えば、2020年には中国が2万7,000クラブと、この地域で最も多くのヘルスフィットネスクラブを有していました。韓国と日本のフィットネスクラブはそれぞれ6,590と4,950でした。

- フィットネスクラブはこの地域のスポーツ栄養製品の主要市場であるため、フィットネスクラブ数の増加は市場に大きな影響を与えます。International Health, Racquet, and Sportsclub Association(IHRSA)によると、この地域ではフィットネスフランチャイズが増加しており、スポーツ栄養セグメントの売上を牽引しています。IHRSAは、ヘルスクラブの再開から、COVID-19救済策にヘルス&フィットネス産業を含めるよう議員に促すことまで、国や州レベルの草の根キャンペーンを展開し、7万9,000人以上のフィットネス関係者や消費者がパンデミックに関連するIHRSAのキャンペーンで行動を起こしました。

- 健康的なライフスタイルを送ることの重要性が、スポーツ栄養市場を活性化。ここ数年のインドのスポーツ栄養市場の加速度的な成長は、主にインドのスポーツ産業の大きな成長、アスリートやボディビルダーにおける各種健康サプリメントやエナジードリンクへの強い需要、高いレベルのフィットネスと栄養を必要とするスポーツや活動への若者の参加の増加によって拍車がかかっています。プロテインサプリメントは市場をリードしており、このセグメントにおける消費全体の70%のシェアを占めています。インドのスポーツ栄養市場は現在、未組織部門に属しており、市場規模は1,300億インドルピー以上、前年比成長率は約25%です。

乾燥ホエイ生産量の増加により、予測期間中のホエイプロテイン価格は安定すると予想されます。

- 乾燥ホエイ粉末は、ホエイプロテイン製造の基本原料と考えられています。原料の受け入れが増加していることが、主にこの地域におけるホエー生産の原動力となっています。中国のチーズ市場は2021年に前年比10%増の5万3,000MTに達し、チーズ製造の製品別としての乾燥ホエイの放出に影響を与えています。米国国務院関税委員会は、中国が固形態のミルクとクリーム、ホエー、改良ホエーを含む特定の荷物の関税除外を申請できる関税除外プロセスを開始しました。中国政府は、グレード付けと評価基準を実施することで、酪農産業の標準化と改善に取り組んでいます。

- チーズ、ひよこ豆、その他の加工乳産業の生産量の増加は、アジア太平洋のホエイ生産に大きな影響を与えています。インドでは、Paragのような乳業会社が乳製品加工産業の製品別であるホエイの生産を開始しました。同企業は、第一段階でおよそ1億1,000万インドルピーを投資し、時間をかけて7億インドルピーまで引き上げる計画です。現在、製薬会社やベビーフード会社に脱塩乳清プロテイン(DWP 28)を供給しています。70%や80%の濃縮乳清プロテインを含む、より多くの製剤が開発中です。月産量は約450トンと予測されています。

- 牛乳は、世界的に乳清プロテインの生産に使用される主要商品です。アジア太平洋は牛乳の生産を増加させました。2019年、アジアにおける全生乳の生産量は3億6,800万トンに増加し、前年比3.8%増となりました。生産高の全般的なプラス動向は、生産動物数の緩やかな増加と収量数値の目に見える拡大によるところが大きいです。

アジア太平洋のホエイプロテイン原料産業概要

アジア太平洋のホエイプロテイン原料市場は適度に統合されており、上位5社で52.26%を占めています。この市場の主要企業は、Arla Foods amba、Fonterra Co-operative Group Limited、Glanbia PLC、Kerry Group PLC、Koninklijke FrieslandCampina N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- プロテイン消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 加水分解物

- 分離物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品及び乳製品代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- タイ

- ベトナム

- その他のアジア太平洋

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arla Foods amba

- Fonterra Co-operative Group Limited

- Freedom Foods Group Limited

- Glanbia PLC

- Groupe LACTALIS

- Hilmar Cheese Company Inc.

- Kerry Group PLC

- Koninklijke FrieslandCampina N.V.

- Lacto Japan Co. Ltd

- Morinaga Milk Industry Co. Ltd

- Olam International Limited

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Asia-Pacific Whey Protein Ingredients Market size is estimated at 667.6 million USD in 2025, and is expected to reach 854.7 million USD by 2030, growing at a CAGR of 5.06% during the forecast period (2025-2030).

With consumption by the snack and beverage categories together accounting for more than 75% of the market share, the food and beverage segment dominated the Asia-Pacific whey protein market

- The F&B segment dominated the Asia-Pacific whey protein market in 2022, with consumption by the snack and beverage sub-segments together accounting for more than 75% of volume share in 2022. Customers now prefer smaller meals or replacing traditional diets with more effective and accessible alternatives, like protein-based snack bars. In Japan's F&B segment, the home meal replacement sub-segment, or Sozai, showed the highest growth, with sales of USD 95 billion in 2018. Another factor driving the sales is the rising number of studies confirming its functionalities like high protein, calorie-free, and easily digestible protein, which makes it a highly desired protein ingredient in the snacks category. Thus, the market witnessed a slower growth rate of 2.79% by value in 2021.

- The F&B segment was followed by supplements, driven by applications in the sports nutrition sub-segment. Although sports nutrition dominated the supplements segment in 2022, the baby food sub-segment is anticipated to register the fastest-growing CAGR of 6.14% by value during the forecast period (2023-2029). Countries like China and India have high birth rates, and the number of children born per year was calculated at 24 million births per year in India and 16 million births per year in China. This is due to increased interest in infant health and increasing awareness of the protein used in these products. For instance, health clubs and gyms in Asia-Pacific countries, like China and Hongkong, generated average revenue per club of more than USD 2 million in 2021, which was the highest among all the countries in the world.

Increasing preference for protein-fortified foods owing to health concerns, such as alarming obesity rates, is driving the regional market

- India witnessed a rise in health-conscious consumers, with the growing obesity rates increasing the population's acceptance of healthy and protein-fortified drinks. The percentage of overweight women rose from 20.6% to 24%, and of overweight men grew from 18.9% to 22.9%. India is projected to record the fastest growth during the forecast period, with a CAGR of 5.77% by value.

- China retained its top position in 2022 due to the rising usage of protein in specialized products, such as infant nutrition, clinical diets, sports, and weight training. High-protein products have garnered considerable interest in the country. In 2022, Chinese consumers consumed around 1.6 million MT of snacks. China is projected to record the second-highest CAGR of 4.98% by value during the forecast period. The growth will likely be driven by the increasing consumption of protein-fortified milkshakes and meal-replacement beverages. New entrants launching relatable products include Smeal, ffit8, Wonderlab, and Miss Zero.

- Australia saw a significant rise in the consumption of whey proteins during the study period, with its utilization in the country registering a CAGR of 2.51% by volume. In 2022, 72% of the volume of whey protein consumed in the country was through the sports nutrition segment, while end-user segments like bakery and snacks had 26.6% and 13.8% of volume shares, respectively. The growth can be attributed to the growing number of 24-hour gyms in the country. This trend has, in turn, stimulated the consumption of protein supplements, especially the ones that have whey proteins as a major ingredient. Over 77% of the animal proteins used in the Australian sports nutrition segment were whey proteins in 2022.

Asia-Pacific Whey Protein Ingredients Market Trends

Increasing number of health and fitness centers is driving the market

- The industry is driven by increased health-related concerns and expanding membership at health clubs. The increasing number of fitness clubs/health clubs further fosters the availability of consumers and their involvement rate. For instance, in 2020, China had the most health and fitness clubs in the region, with 27,000 clubs. South Korea and Japan had 6,590 and 4,950 fitness clubs, respectively.

- The increase in the number of health and fitness clubs majorly impacts the market as they are the major marketplace for sports nutrition products in the region. According to the International Health, Racquet, and Sportsclub Association (IHRSA), there is an increase in fitness franchises in the region, driving sales of the sports nutrition segment. The IHRSA launched national and state-level grassroots campaigns, ranging from reopening health clubs to urging lawmakers to include the health and fitness industry in any COVID-19 relief package, as more than 79,000 fitness professionals and consumers took action on IHRSA campaigns relating to the pandemic.

- The importance of leading a healthy lifestyle fuels the sports nutrition marketplace. The accelerated growth of the Indian sports nutrition market in the last few years has been spurred primarily by the huge growth in the Indian sports industry, strong demand for various health supplements and energy drinks among athletes and bodybuilders, and increasing youth participation in sports and activities that require a high level of fitness and nutrition. Protein supplements lead the market, accounting for a share of 70% of the overall consumption in this segment. The Indian sports nutrition market currently lies in the unorganized sector, with a market size of over INR 1,300 crore and a Y-o-Y growth of about 25%.

Increasing dry whey production is expected to stabilize whey protein prices during the forecast period

- Dry whey powder is considered the basic raw material for whey protein production. The increasing acceptance of ingredients mainly drives whey production in the region. China's cheese market reached 53,000 MT in 2021, an increase of 10% compared to the previous year, impacting the release of dry whey as a by-product from cheese production. The US State Council Tariff Commission launched a tariff exclusion process that allows China to apply for tariff exclusion for specific consignments, which includes milk and cream in solid form, whey, and modified whey. The Chinese government is taking steps to standardize and improve the dairy industry by implementing grading and evaluation standards.

- The rise in the production of cheese, chickpeas, and other processed milk industries is majorly impacting whey production in Asia-Pacific. In India, dairy companies like Parag started producing whey, a by-product of their dairy processing industry. The corporation invested roughly INR 110 crore in the first phase, with plans to raise it to INR 70 crore over time. Currently, it supplies pharmaceutical and baby food companies with demineralized whey protein (DWP 28). More formulations are being developed, including 70% and 80% whey protein concentrates. The monthly production volume is projected to be around 450 tons.

- Milk is the primary commodity used to produce whey protein globally. Asia-Pacific increased the production of milk. In 2019, the production of whole fresh milk in Asia rose to 368 million tons, an increase of 3.8% over the previous year. The generally positive trend in output was largely a result of the moderate increase in the number of producing animals and a tangible expansion in yield figures.

Asia-Pacific Whey Protein Ingredients Industry Overview

The Asia-Pacific Whey Protein Ingredients Market is moderately consolidated, with the top five companies occupying 52.26%. The major players in this market are Arla Foods amba, Fonterra Co-operative Group Limited, Glanbia PLC, Kerry Group PLC and Koninklijke FrieslandCampina N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 China

- 3.4.3 India

- 3.4.4 Japan

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Hydrolyzed

- 4.1.3 Isolates

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 RTE/RTC Food Products

- 4.2.2.1.7 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 New Zealand

- 4.3.8 South Korea

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.3.11 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Arla Foods amba

- 5.4.2 Fonterra Co-operative Group Limited

- 5.4.3 Freedom Foods Group Limited

- 5.4.4 Glanbia PLC

- 5.4.5 Groupe LACTALIS

- 5.4.6 Hilmar Cheese Company Inc.

- 5.4.7 Kerry Group PLC

- 5.4.8 Koninklijke FrieslandCampina N.V.

- 5.4.9 Lacto Japan Co. Ltd

- 5.4.10 Morinaga Milk Industry Co. Ltd

- 5.4.11 Olam International Limited

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 246 Pages

- 納期

- 2~3営業日