|

市場調査レポート

商品コード

1698292

セリアック病治療の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Celiac Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| セリアック病治療の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月12日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

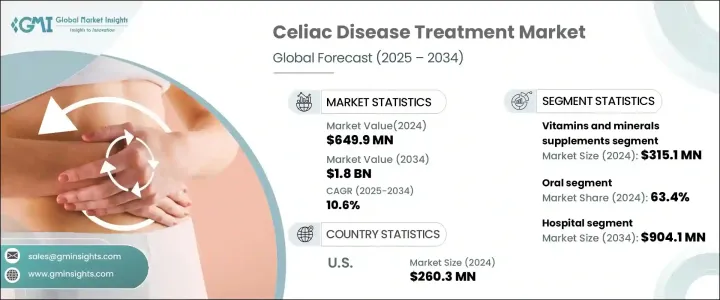

世界のセリアック病治療市場は、2024年に6億4,990万米ドルと評価され、2025年から2034年にかけてCAGR10.6%で拡大すると予測されています。

セリアック病の有病率の増加と、高度な診断ツールに関するヘルスケア専門家の意識の高まりが市場を牽引しています。検出方法の改善により診断される人が増えるにつれ、効果的な治療に対する需要も高まり続けています。研究開発の進展が医薬品による治療法の導入を加速させ、市場拡大をさらに後押ししています。セリアック病患者以外にもグルテンフリーの食生活を好む人が急増し、革新的な非侵襲的診断ツールの採用が業界を強化しています。HLAタイピングと抗体検査における技術的進歩は、診断精度の向上と検査期間の短縮をもたらし、それによって診断率を高め、治療ソリューションの需要を押し上げています。

同市場は、遺伝的素因を持つ人がグルテンを摂取することで発症する自己免疫疾患であるセリアック病の管理と治療に焦点を当てています。同市場には、症状の緩和、合併症の予防、患者の健康増進を目的とした医薬品、サプリメント、治療薬が含まれます。市場はグルテンフリー食、ビタミン・ミネラルサプリメント、医療療法に区分されます。セリアック病は栄養吸収を阻害するため、健康維持のためのサプリメント摂取が必要となります。カルシウムとビタミンDの摂取は、吸収不良に伴う骨の健康への懸念に対処するために特に重視されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 6億4,990万米ドル |

| 予測金額 | 18億米ドル |

| CAGR | 10.6% |

腸の健康をサポートする特殊なサプリメントを求める消費者が増えており、市場拡大に拍車をかけています。投与経路に基づき、市場は経口治療と非経口治療に分けられます。経口セグメントは2024年に63.4%と大きなシェアを占め、ヘルスケア提供者の支援なしに患者が病状を管理できる利便性が支持されています。酵素サプリメントや免疫調整剤を含む新規経口製剤の導入は、治療の選択肢を広げ、患者のアドヒアランスを向上させています。これらの進歩は薬効、バイオアベイラビリティ、吸収性を高め、採用率を高めています。経口療法は、注射や点滴に比べて投与が容易であるため、柔軟な治療ソリューションを必要とする多忙なライフスタイルの患者に対応できることから、依然として好まれています。

エンドユーザー市場は、病院、専門クリニック、在宅ケア環境、その他のカテゴリーに分類されます。2024年には病院が最大セグメントを占め、2034年には9億410万米ドルに達すると予測されています。治療用ワクチンと抗炎症薬の統合により、病院での治療が拡大しています。高度な診断ツールと多様な治療オプションが患者の転帰を改善し、疾病管理のための入院を増加させています。病院は、栄養療法、グルテンフリー食、生物学的製剤など、プライマリケアでは必ずしも利用できない、第一選択として不可欠な治療を提供します。生物学的製剤や酵素療法への依存が頻繁な通院を促し、市場成長に寄与しています。

2024年には、米国が2億6,030万米ドルの評価額で北米市場を独占しました。セリアック病患者の増加により、高度な治療に対する需要が高まっています。米国は北米の症例の大部分を占めており、患者基盤の拡大を強調しています。革新的な治療アプローチ、診断システムの強化、主要企業による戦略的差別化など、継続的な研究が業界の成長を促進しています。医薬品の進歩は免疫系の反応を緩和することを目的としており、最も差し迫ったアンメットメディカルニーズのひとつに対応しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- セリアック病の有病率の上昇

- 治療選択肢の技術的進歩

- グルテンフリー製品に対する需要の増加

- セリアック病診断技術の増加

- 業界の潜在的リスク・課題

- グルテンフリー製品の高コスト

- 厳しい規制当局の承認

- 成長促進要因

- 成長可能性分析

- 規制状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場マトリックス分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療別、2021年~2034年

- 主要動向

- ビタミンとミネラルのサプリメント

- グルテンフリーの食事療法

- 医療療法

第6章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 非経口

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門クリニック

- 在宅医療

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- ActoBio

- Amgen

- Amneal Pharmaceuticals

- BioLineRx

- Calypso Biotech

- General Mills

- Glenmark Life Sciences

- Hikma Pharmaceuticals

- Innovate Biopharmaceutical

- Novartis

- Takeda Pharmaceutical Company

- Teva Pharmaceutical

- Viatris

- Zydus Pharmaceuticals

The Global Celiac Disease Treatment Market was valued at USD 649.9 million in 2024 and is projected to expand at a CAGR of 10.6% from 2025 to 2034. The increasing prevalence of celiac disease and growing awareness among healthcare professionals regarding advanced diagnostic tools are driving the market. As more people are diagnosed due to improved detection methods, the demand for effective treatment continues to rise. Advancements in research and development are accelerating the introduction of pharmaceutical treatments, further propelling market expansion. The surge in gluten-free dietary preferences beyond the celiac population and the adoption of innovative non-invasive diagnostic tools are strengthening the industry. Technological advancements in HLA typing and antibody testing are enhancing diagnostic accuracy and reducing test duration, thereby increasing diagnosis rates and boosting demand for therapeutic solutions.

The market focuses on the management and treatment of celiac disease, an autoimmune disorder triggered by gluten ingestion in genetically predisposed individuals. It includes pharmaceutical products, supplements, and therapies designed to alleviate symptoms, prevent complications, and enhance patient well-being. The market is segmented into gluten-free diets, vitamin and mineral supplements, and medical therapies. The vitamins and minerals supplements category dominated, contributing USD 315.1 million in 2024, as celiac disease impairs nutrient absorption, necessitating supplementation to maintain health. Calcium and vitamin D intake is particularly emphasized for addressing bone health concerns associated with malabsorption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $649.9 Million |

| Forecast Value | $1.8 Billion |

| CAGR | 10.6% |

Consumers are increasingly seeking specialized supplements that support gut health, fueling market expansion. Based on administration routes, the market is divided into oral and parenteral treatments. The oral segment held a significant share of 63.4% in 2024, favored for its convenience, allowing patients to manage their condition without healthcare provider assistance. The introduction of novel oral formulations, including enzyme supplements and immune modulators, is broadening treatment options and improving patient adherence. These advancements enhance drug efficacy, bioavailability, and absorption, increasing adoption rates. Oral therapies remain preferred due to their ease of administration compared to injections and infusions, accommodating patients with busy lifestyles who require flexible treatment solutions.

The end-user market is classified into hospitals, specialty clinics, homecare settings, and other categories. Hospitals accounted for the largest segment in 2024, with projections reaching USD 904.1 million by 2034. The integration of therapeutic vaccines and anti-inflammatory drugs is expanding hospital-based treatment offerings. Advanced diagnostic tools and a diverse range of therapeutic options improve patient outcomes, increasing hospital admissions for disease management. Hospitals provide essential first-line treatments, including nutrition therapy, gluten-free diets, and biologics, which are not always available in primary care settings. The reliance on biologic agents and enzyme therapies drives frequent hospital visits, contributing to market growth.

In 2024, the United States dominated the North American market with a valuation of USD 260.3 million. Rising celiac disease cases are intensifying the demand for advanced treatments. The U.S. accounts for a significant portion of North American cases, highlighting an expanding patient base. Ongoing research into innovative treatment approaches, enhanced diagnostic systems, and strategic differentiation by key market players is fostering industry growth. Pharmaceutical advancements aim to mitigate immune system reactions, addressing one of the most pressing unmet medical needs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of celiac disease

- 3.2.1.2 Technological advancements in therapeutic options

- 3.2.1.3 Increasing demand for gluten-free products

- 3.2.1.4 Increasing diagnostic technologies for celiac disease diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of gluten-free products

- 3.2.2.2 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Vitamins and mineral supplements

- 5.3 Gluten-free diet

- 5.4 Medical therapies

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Parenteral

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Homecare settings

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ActoBio

- 9.2 Amgen

- 9.3 Amneal Pharmaceuticals

- 9.4 BioLineRx

- 9.5 Calypso Biotech

- 9.6 General Mills

- 9.7 Glenmark Life Sciences

- 9.8 Hikma Pharmaceuticals

- 9.9 Innovate Biopharmaceutical

- 9.10 Novartis

- 9.11 Takeda Pharmaceutical Company

- 9.12 Teva Pharmaceutical

- 9.13 Viatris

- 9.14 Zydus Pharmaceuticals