欧州のホエイプロテイン原料- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Whey Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 240 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690982

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

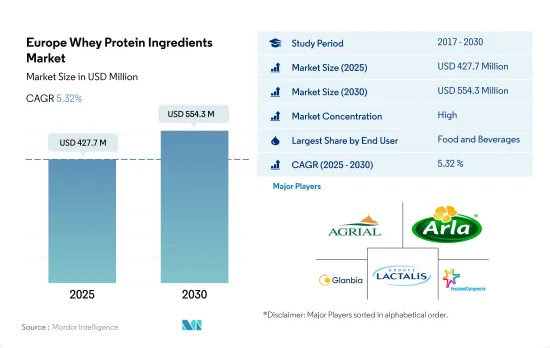

欧州のホエイプロテイン原料市場規模は2025年に4億2,770万米ドルと推定され、2030年には5億5,430万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.32%で成長する見込みです。

若年層におけるフィットネス動向の高まりにより、地域全体でサプリメントの市場シェアが拡大

- 2022年、飲食品は欧州におけるホエイプロテイン市場の最大消費者であり続けた。このセグメントの大きなシェアは、主にスナック、ベーカリー、飲料といったサブセグメントによるもので、2022年の同セグメントの数量シェアは37%に達しました。スナックカテゴリーを後押しするように、2021年には欧州の消費者の46%がプロテインバーを健康的なスナックと考えており、消費者の16%がプロテインバー、粉末、シリアル、パンケーキなどのプロテイン強化スナックを週に1回利用しています。このような需要増加要因が、スナックのサブセグメントにおけるホエイプロテイン市場を牽引しており、予測期間中に金額ベースで2.30%のCAGRで推移すると予測されています。

- 市場は、COVID-19パンデミックによる全国的な封鎖をきっかけに、消費者がフードサービスから小売チャネルに移行するのを示しました。消費者は食品のまとめ買いを行い、これが2022年の飲食品セグメントの市場シェアを押し上げました。同セグメントにおけるホエイ・プロテイン需要は、2022年に12%成長し、これは前年の成長率の約4倍でした。

- 飲食品セグメントに続き、サプリメントセグメントは主にスポーツ/パフォーマンス栄養サブセグメントが牽引しました。2022年には、サプリメントセグメントで消費されるホエイ・プロテインの約80%はスポーツ栄養だけによるものです。欧州では、フィットネスクラブの総数は2021年に63,173となりました。スポーツは、多くの消費者が求める活動的で健康的なライフスタイルのコンポーネントとなっています。この活動的な生き方は、ジムの利用やスポーツ栄養製品の消費を後押しする効果があります。ホエイプロテインの補給は、筋肉の損傷を軽減し、激しいトレーニングからの筋肉の回復を促進し、それによってスポーツのパフォーマンスを補助します。

消費者の機能性飲料への志向の高まりが、ホエイ・プロテイン原料の需要増につながっています。

- 国別では、英国が2022年の欧州市場で数量ベースでトップの座を維持しました。同国におけるホエイプロテイン需要は、フィットネス愛好家の増加とジムやフィットネスクラブへの消費者の流入が主要因となっています。例えば、2021年現在、1,030万人がジムの会員となっており、これは英国総人口の15%以上であり、消費者のパフォーマンス向上サプリメントへの依存度が年々高まっていることを表しています。英国のホエイプロテイン市場は、サプリメントセグメントが64%と大きなシェアを占め、次いで飲食品産業が2022年に33.1%のシェアを獲得しました。したがって、ホエイプロテインの使用は、フィットネス愛好家やフィットネスクラブの増加により、主にスポーツ栄養で観察されました。

- ドイツは、飲食品セグメントにおける高いプロテイン消費量に牽引され、2022年には市場のもう一つの主要国となりました。飲料は最も急成長しているサブセグメントであり、予測期間中のCAGRは7.09%と予想されます。国内での健康意識の高まりに伴い、飲料におけるホエイプロテインの需要が高まっています。消費者が炭酸飲料からより健康的な選択肢を選ぶようになり、プロテインウォーターやエナジードリンクといった製品が動向になりつつあります。

- トルコはホエイプロテインで最も急成長している国であり、予測期間中のCAGRは6.02%と予測されています。大多数の参加者の健康的な食事態度は高く理想的なレベルにあります。特に、ホエイプロテインを含む製品は、その健康上の利点から重要性を増しています。同国における健康食のブーム傾向は、ホエイ・プロテインなどの原料に対する大きな需要を生み出しています。

欧州のホエイプロテイン原料市場の動向

消費者層の拡大がスポーツサプリメントセグメントに利益をもたらす可能性

- 欧州のスポーツ栄養市場は、2016~2019年にかけて15%成長しました。しかし、2020年には前年比成長率で4.33%の急減を示しました。ヘルスクラブはサプリメントの一般的な流通チャネルの1つであるが、パンデミックがフィットネスクラブの運営者、従業員、消費者に厳しい打撃を与えたため、スポーツサプリメントの販売に悪影響を与えました。2020年には、政府の規制により、フィットネスクラブ、ヘルスクラブ、スポーツジムは閉鎖を余儀なくされ、クラブの会員数は前年比で10~15%減少しました。パンデミックの影響でクラブ数も減少。2020年後半に市場を回復させるため、フィットネスサービスにも適用される一般付加価値税率19%を年末までの期間限定で16%に引き下げ、経済需要を強化しました。

- フィットネス愛好者の増加により、スポーツサプリメントの利用範囲はメインユーザー以外にも広がっています。消費者がジムの必需品を買い求めるようになり、特にイタリア、フランス、ドイツなどの先進国では、健康・フィットネス用品への需要が高まっています。これらの国々は、ジムの会員権、サプリメント、トレーニングなどにお金をかける主要な消費者としても浮上しています。この地域には約63,000のフィットネスセンターがあり、これらのクラブはすべて共同で毎年3~4%の会員数の増加を確認しています。

- 天然原料を使用したスポーツ栄養製品に対する需要は、メーカーに製品の付加価値を高める機会を提供することで、市場の成長を支えています。欧州のスポーツ栄養市場は、英国、ドイツ、スペイン、フランスが70%以上を占めています。スポーツドリンクセグメントでは、英国とドイツが市場シェアの50%以上を占めています。

乾燥ホエイ生産量の増加により、予測期間中のホエイプロテイン価格は安定します。

- ホエイは酪農産業の製品別で栄養価が高いです。ホエイ粉末はチーズ製造装置から得られます。それらはスプレードライされる前に脱脂され濃縮されます。欧州の乾燥ホエー価格は堅調かやや低いです。産業筋によると、ホエイ粉末は買い手のニーズを満たすのに十分な量があり、生産も活発だといいます。2022年、オランダのホエイ生産量はEU全体の約15%と2番目に高く、チーズ生産量はEU全体の約9%と4番目に高かったです。

- 主要国全体でチーズの生産が大規模かつ広範囲に行われていることが、この地域の乾燥ホエー生産に寄与しています。2022年には、全生乳生産量のうち、大半の生乳(1億4,990万トン)が欧州の酪農場に納入されます。2022年時点で、この地域では5,920万トンの全乳と1,690万トンの脱脂乳から1,040万トンのチーズが生産されています。2022年時点でEU最大のチーズ生産国はドイツで、全体の22%を占めます。第2位はフランスで全体の18%を占め、第3位はイタリアでした。液体ホエイはチーズ工場で処理され、乾燥ホエイに変換されます。この地域の他の著名なチーズ生産国には、イタリア、オランダ、ポーランド、スペイン、デンマークなどがあります。

- ドイツは欧州連合における生乳の主要生産国で、2020年の生乳出荷量の21%以上を占めます。生乳生産量の増加は、同国がドライホエイの原料を生産することを可能にする牛1頭当たりの生乳生産量の増加に起因しています。

欧州のホエイプロテイン原料産業概要

欧州のホエイプロテイン原料市場はかなり統合されており、上位5社で83.71%を占めています。この市場の主要企業は、 Agrial Enterprise、Arla Foods amba、Glanbia PLC、Groupe Lactalis、Koninklijke FrieslandCampina N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- プロテイン消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 加水分解物

- 分離物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品及び乳製品代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Agrial Enterprise

- Arla Foods amba

- Carbery Food Ingredients Limited

- Glanbia PLC

- Groupe Lactalis

- Koninklijke FrieslandCampina N.V.

- Lactoprot Deutschland GmbH

- MEGGLE GmbH & Co. KG

- Morinaga Milk Industry Co. Ltd

- Sodiaal Union SCA

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Europe Whey Protein Ingredients Market size is estimated at 427.7 million USD in 2025, and is expected to reach 554.3 million USD by 2030, growing at a CAGR of 5.32% during the forecast period (2025-2030).

The rising fitness trend among the young population resulted in an increased market share of supplements across the region

- In 2022, food and beverage remained the largest consumer of the whey protein market in Europe. The segment's large share was primarily contributed by its sub-segments, such as snacks, bakery, and beverages, which contributed to the segment's share of 37% by volume in 2022. Boosting the snacks category, in 2021, 46% of European consumers considered protein bars healthy snacks, and 16% of consumers used protein-fortified snacks, such as protein bars, powders, cereals, and pancakes once a week. These factors boosting demand drive the whey protein market in the snacks sub-segment, which is projected to register a CAGR of 2.30% by value during the forecast period.

- The market witnessed consumer diversion from the foodservice to the retail channel in the wake of nationwide lockdowns imposed due to the COVID-19 pandemic. Consumers were engaged in the bulk purchase of food products, which boosted the food and beverage segment's market share in 2022. The demand for whey protein in the segment grew by 12% in 2022, which was about four times the growth rate of the previous year.

- The food and beverages segment was followed by the supplements segment, primarily driven by the sports/performance nutrition sub-segment. In 2022, about 80% of whey protein consumed in the supplements segment was by sports nutrition alone. In Europe, the total number of fitness clubs was 63,173 in 2021. Sports have become a component of an active, healthy lifestyle that is sought after by many consumers. This active way of life has an effect in boosting the use of gyms and the consumption of sports nutrition products. Whey protein supplementation reduces muscle damage and facilitates muscle recovery from strenuous training, thereby assisting sports performance.

Consumers' growing inclination toward functional beverages has resulted in higher demand for whey protein ingredients

- By country, the United Kingdom retained its top position in the European market by volume in 2022. The demand for whey protein in the country is majorly led by an increasing number of fitness enthusiasts and a heavy consumer influx in gyms and fitness clubs. For instance, as of 2021, 10.3 million people held a gym membership, which was over 15% of the total UK population, representing consumers' increasing reliance on performance-boosting supplements over the years. The whey protein market in the United Kingdom is highly driven by the supplements segment, which held a significant share of 64%, followed by the food and beverage industry with a 33.1% share in 2022. Thus, whey protein usage was mainly observed in sports nutrition due to the increasing number of fitness enthusiasts and fitness clubs.

- Germany was another leading country in the market in 2022, driven by high protein consumption in the food and beverage segment. Beverages is the fastest-growing sub-segment, with an expected CAGR of 7.09% during the forecast period. The demand for whey protein in beverages is rising with the growing health awareness in the country. Products such as protein water and energy drinks are becoming a trend as consumers are choosing to move away from carbonated beverages toward healthier options.

- Turkey is the fastest-growing country for whey protein and is projected to register a CAGR of 6.02% during the forecast period. The healthy eating attitudes of the majority of participants are at high and ideal levels. In particular, products containing whey protein have gained importance due to the health benefits they offer. The booming trend of healthy food in the country has created a significant demand for ingredients such as whey protein.

Europe Whey Protein Ingredients Market Trends

The expanding consumer base may benefit the sports supplements segment

- The European sports nutrition market grew by 15% during 2016-2019. However, in 2020, it witnessed a steep decline of 4.33% in the Y-o-Y growth rate. Health clubs, being one of the common sales channels for supplements, impacted the sales of sports supplements adversely as the pandemic took a harsh toll on fitness club operators, employees, and consumers. In 2020, due to government regulations, fitness clubs, health clubs, and gyms were forced to close, and club memberships declined by 10-15% in 2020 compared to the previous year. The number of clubs also decreased under the influence of the pandemic. To regain the market in the second half of 2020, the general VAT rate of 19%, which also applies to fitness services, was reduced to 16% for a limited period until the end of the year to strengthen economic demand.

- The growing number of fitness enthusiasts expands the scope of sports supplements beyond their mainstream users. As consumers flock to buy gym requisites, the demand for health and fitness products is growing, especially in developed countries like Italy, France, and Germany. These countries also emerged as the major spenders on gym memberships, supplements, training, etc. There are around 63,000 fitness centers in the region, and all these clubs jointly witness an increase of 3-4% in memberships yearly.

- The demand for sports nutrition products with natural ingredients supports market growth by providing an opportunity for manufacturers to add value to their products. The United Kingdom, Germany, Spain, and France dominate more than 70% of the European sports nutrition market. In the sports drinks segment, the United Kingdom and Germany capture over 50% of the market share.

Increasing dry whey production to stabilize whey protein prices during the forecast period

- Whey is a highly nutritional byproduct of the dairy industry. Whey powders are obtained from cheese manufacturing units. They are skimmed and concentrated before being spray-dried. European dry whey prices are steady to slightly lower. Industry sources suggest plenty of whey powder is available to meet buyer needs, and production is active. In 2022, the Netherlands had the second-highest production level for whey (about 15% of the EU total) and the fourth-highest for cheese (about 9% of the EU total).

- The significant and widespread production of cheese across major countries contributes to the dry whey production in the region. In 2022, out of the total raw milk production, a vast majority of raw milk (149.9 million tonnes) was delivered to European dairies. As of 2022, 10.4 million tonnes of cheese from 59.2 million tonnes of whole milk and 16.9 million tonnes of skimmed milk were produced in the region. Germany was the biggest producer of cheese in the EU in 2022, accounting for 22% of the total. France placed second, accounting for 18% of the total, with Italy in third. Liquid whey is processed from cheese factories and then converted to dry whey. Other prominent cheese-producing countries in the region include Italy, the Netherlands, Poland, Spain, and Denmark, among others.

- Germany is the leading producer of milk in the European Union, accounting for more than 21% of milk deliveries in 2020. The rise in milk production is attributed to the escalated volume of milk production per cow, which enables the country to produce the raw material for dry whey.

Europe Whey Protein Ingredients Industry Overview

The Europe Whey Protein Ingredients Market is fairly consolidated, with the top five companies occupying 83.71%. The major players in this market are Agrial Enterprise, Arla Foods amba, Glanbia PLC, Groupe Lactalis and Koninklijke FrieslandCampina N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 France

- 3.4.2 Germany

- 3.4.3 Italy

- 3.4.4 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Hydrolyzed

- 4.1.3 Isolates

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 RTE/RTC Food Products

- 4.2.2.1.7 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Belgium

- 4.3.2 France

- 4.3.3 Germany

- 4.3.4 Italy

- 4.3.5 Netherlands

- 4.3.6 Russia

- 4.3.7 Spain

- 4.3.8 Turkey

- 4.3.9 United Kingdom

- 4.3.10 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agrial Enterprise

- 5.4.2 Arla Foods amba

- 5.4.3 Carbery Food Ingredients Limited

- 5.4.4 Glanbia PLC

- 5.4.5 Groupe Lactalis

- 5.4.6 Koninklijke FrieslandCampina N.V.

- 5.4.7 Lactoprot Deutschland GmbH

- 5.4.8 MEGGLE GmbH & Co. KG

- 5.4.9 Morinaga Milk Industry Co. Ltd

- 5.4.10 Sodiaal Union SCA

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 240 Pages

- 納期

- 2~3営業日