米国のホエイプロテイン原料- 市場シェア分析、産業動向、統計、成長予測(2025~2030年)

United States Whey Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 222 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690969

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

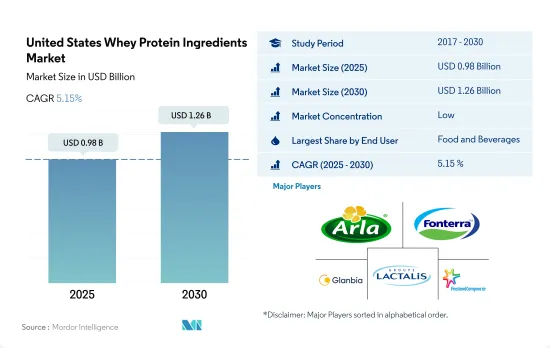

米国のホエイプロテイン原料市場規模は2025年に9億8,000万米ドルと推定され、2030年には12億6,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.15%で成長します。などです。

スポーツとパフォーマンス栄養産業の急成長と美容クリニックの増加が、市場におけるホエイプロテインの使用に貢献。

- ホエイプロテイン市場は、飲食品とサプリメントの2つの主要用途で構成されています。2019年には、サプリメントの消費量が飲食品の消費量を上回り、すべてのエンドユーザー用途の中でトップの地位を占めました。この成長は、筋肉愛好家やフィットネス愛好家の増加によるものと考えられます。この状況は、ホエイプロテインベースのスポーツ飲料、特殊な栄養製品、運動能力を最適化するように設計されたその他の製品に対する消費者の需要を高めています。2016~2019年にかけて、米国全土のフィットネスセンターの会員総数は12.04%の成長を示し、2019年には6,420万人に達します。しかし、米国の飲食品産業は2019年に10.57%の成長を遂げました。

- サプリメントセグメントは成長率で他の用途を上回りそうで、予測期間中に6.51%のCAGRで推移すると予測されています。急増するスポーツとパフォーマンス栄養産業は、最速のCAGR 6.70%を記録すると予測されています。この状況はさらに、全国のサプリメント産業におけるホエイプロテインの販売を促進すると予測されます。

- ホエイプロテインの他の急成長エンドユーザーセグメントは、パーソナルケアと化粧品であり、予測期間中に5.13%のCAGRで推移すると予測されています。ホエイプロテインは、アンチエイジング製品、ヘアケア製品、ネイルケア製品などに使用されています。美容クリニックの増加、身だしなみに対する一人当たりの支出の増加、強固な規制の枠組み、美容・化粧品産業の成長は、将来の需要全体を押し上げる可能性があります。2016~2021年にかけて、美容・パーソナルケア製品への年間平均支出額は米国全体で7.04%上昇しました。

米国のホエイプロテイン原料市場動向

スポーツ/パフォーマンス栄養は予測期間中に大きな成長が見込まれる

- 健康への関心の高まりとヘルスクラブ会員数の増加が、主にスポーツ/パフォーマンスニュートリションセグメントを牽引しています。2009~2019年にかけて、米国のジム数は39%増加しました。しかし、このセグメントは、2020年のCOVID-19パンデミックによる全国的な封鎖の間のジムの閉鎖により大幅な減少を示しました。ヘルスクラブは、スポーツサプリメントの最も人気のある流通チャネルの一つです。ヘルスクラブの閉鎖はサプリメントの販売にマイナスの影響を与えました。2020年には、ゴールドジム、フライホイール・スポーツ、タウンスポーツインターナショナル、24アワー・フィットネスといった複数のジムが破産を宣言しました。2020年のスポーツ栄養製品の売上は減少し、セグメント全体の前年比成長率は3.37%低下しました。

- アクティブなライフスタイルを送ることの重要性が、スポーツ/パフォーマンス栄養セグメントに拍車をかけています。2021年には、米国の6歳以上の消費者の67%がフィットネス活動に参加し、そのうち43.3%が個人スポーツ、52.9%がアウトドアスポーツ、22.1%がチームスポーツに従事しています。消費者は、最適な栄養とより健康的なライフスタイルの価値をより認識するようになっており、これらすべてがスポーツ/パフォーマンス栄養セグメントにプラスの影響を与えています。

- スポーツ/パフォーマンス栄養は、米国のホエイプロテイン市場で最も急成長しているエンドユーザーセグメントであり、そのうち動物性プロテインが金額ベースで91.1%と大きなシェアを占めています。フィットネス産業では、運動後の筋肉や組織の修復に使用される栄養補助食品において、ホエイ、コラーゲン、ミルクプロテインなどの動物性プロテイン成分の使用量が急速に増加しています。プロテインサプリメントの入手可能性の増加、これらの製品のレクリエーションやライフスタイルユーザーの増加、健康意識の高まりが、予測期間中の市場成長を押し上げると予想されます。

ドライホエイの生産増加は、予測期間中のホエイプロテイン価格を安定させる可能性があります。

- ホエイ生産は主にチーズ生産工場からの供給が牽引しており、国内の液体ホエイ生産の大半を占めています。2022年4月現在、米国には500を超えるチーズ生産工場があります。ホエイ粉末がホエイ製品市場を独占し、WPCが僅差で続きます。2021年には、約9億3,400万ポンドの乾燥ホエイが国内で生産されました。この需要は主に、同国の飲食品市場全体におけるプロテインと高プロテイン製品への強い傾斜によってもたらされています。

- 大手企業は、ホエイプラントの増設に向けて取り組んでいます。ホエイは乳製品市場において不可欠な資源となっています。スポーツ・パフォーマンス栄養製品は、ハイエンド・プロテイン原料部門の力強い成長を牽引しています。WPCは、チーズ加工に由来する低温殺菌ホエイから、一定割合の非プロテイン成分を除去して製造されます。食用に利用可能なWPCの最終製品は、乳清プロテインを34%以上含むWPC34と、プロテインを80%以上含むWPC80です。

- 2020年、パンデミックの影響で全国的に生産工場が閉鎖されたため、ホエイ全体の生産量は減少しました。ドライホエイの生産量は約9億5,100万ポンドで、2.7%減少しました。WPCの生産量は約4億7,800万ポンドで、2019年の生産量から2.7%減少しました。逆に、ミルク工場の生産量はパニック買いにより急増し、2020年4月以降は安定しました。飼料セクタ向けドライホエイの生産は、価格が横ばいのため安定しています。WPCの生産は安定しているが、一部の市場関係者は今後数四半期で高濃度WPCの価格上昇を予想しており、生産にプラスの影響を与えそうです。

米国ホエイプロテイン原料産業概要

米国ホエイプロテイン原料市場は細分化されており、上位5社で22.28%を占めています。この市場の主要企業は、 Arla Foods amba、Fonterra Co-operative Group Limited、Glanbia PLC、Groupe Lactalis、Koninklijke FrieslandCampina NVなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- プロテイン消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 加水分解物

- 分離物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品及び乳製品代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Agropur Dairy Cooperative

- Arla Foods amba

- Carbery Food Ingredients Limited

- Dairy Farmers of America

- Fonterra Co-operative Group Limited

- Glanbia PLC

- Grande Cheese Company

- Groupe Lactalis

- Hilmar Cheese Company Inc.

- Hoogwegt Group

- Koninklijke FrieslandCampina NV

- MEGGLE GmbH & Co.KG

- Morinaga Milk Industry Co. Ltd

- Talley's Group Limited

- Tatua Co-operative Dairy Company Ltd

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The United States Whey Protein Ingredients Market size is estimated at 0.98 billion USD in 2025, and is expected to reach 1.26 billion USD by 2030, growing at a CAGR of 5.15% during the forecast period (2025-2030).

Surging sports and performance nutrition industry coupled with growing number of beauty clinics benefitted the use of whey proteins in the market

- The whey protein market comprises food and beverage and supplements as the two major applications. In 2019, the consumption volume of supplements surpassed the consumption volume of food and beverage to claim the top position among all end-user applications. This growth can be attributed to the rising number of muscle and fitness enthusiasts. This situation is increasing consumers' demand for whey protein-based sports beverages, specialized nutritional products, and other products designed to optimize athletic performance. From 2016 to 2019, the total number of memberships at fitness centers across the United States witnessed a growth of 12.04%, reaching 64.2 million memberships in 2019. However, the food and beverage industry in the United States grew by 10.57% in 2019.

- The supplements segment is likely to outpace other applications in terms of growth rate, recording a projected CAGR of 6.51% during the forecast period. The surging sports and performance nutrition industry is projected to register the fastest CAGR of 6.70%. This situation is further anticipated to drive the sales of whey protein in the supplements industry across the country.

- The other fastest-growing end-user segment for whey protein is personal care and cosmetics, which is projected to register a CAGR of 5.13% during the forecast period. Whey protein is used in anti-aging products, hair-care products, and nail-care products, among other things. The increasing number of beauty clinics, increasing per capita expenditure on personal appearance, a robust regulatory framework, and the growing beauty and cosmetics industry may boost overall demand in the future. Between 2016 and 2021, the average annual expenditure on beauty and personal care products rose by 7.04% across the United States.

United States Whey Protein Ingredients Market Trends

Sport/performance nutrition is expected to witness significant growth during the forecast period

- Rising health concerns and memberships across health clubs are primarily driving the sport/performance nutrition segment. From 2009 to 2019, the number of gyms in the United States rose by 39%. However, the segment witnessed a significant decline due to gym closures during the COVID-19 pandemic-induced nationwide lockdown in 2020. Health clubs are among the most popular sales channels for sports supplements. The closure of health clubs had a negative impact on the sales of supplements. In 2020, several gyms like Gold's Gym, Flywheel Sports, Town Sports International, and 24-Hour Fitness declared bankruptcy. Sales of sports nutrition products decreased in 2020, and the segment's overall Y-o-Y growth rate reduced by 3.37%.

- The importance of leading an active lifestyle is fueling the sports/performance nutrition segment. In 2021, 67% of US consumers aged six and above participated in fitness activities, of which 43.3% of consumers engaged in individual sports, 52.9% in outdoor sports, and 22.1% in team sports. Consumers are becoming more aware of the value of optimal nutrition and healthier lifestyles, all of which positively impact the sports/performance nutrition segment.

- Sports/performance nutrition is the fastest-growing end-user segment in the US whey protein market, of which animal protein accounts for a major share of 91.1% in terms of value. The fitness industry is rapidly increasing the usage of animal protein ingredients, such as whey, collagen, and milk proteins, in nutritional supplements used for muscle or tissue repair after workouts. The rise in the availability of protein supplements, a growth in the number of recreational and lifestyle users of these products, and an increase in health awareness are expected to boost market growth over the forecast period.

Increasing production of dry whey may stabilize whey protein prices during the forecast period

- Whey production is mainly driven by the supply from cheese production plants, accounting for most of the country's liquid whey production. As of April 2022, there were over 500 cheese production plants in the United States. Whey powder dominates the whey products market, closely followed by WPC. In 2021, around 934 million pounds of dry whey was produced in the country. The demand is mainly driven by a strong inclination toward protein and high-protein products across the country's food and beverage market.

- Major companies are working toward securing additional whey plants. Whey has become an essential resource in the dairy market. Sports and performance nutrition products drive strong growth in the high-end protein ingredients sector. WPC is produced by removing a certain percentage of non-protein constituents from pasteurized whey derived from cheese processing. The finished WPC products available for food aid are WPC34, which contains more than 34% whey protein, and WPC80, which contains more than 80% protein.

- In 2020, the overall whey production declined due to the pandemic because production plants had shut down across the nation. The production volume of dry whey was nearly 951 million pounds, down by 2.7%. The production volume of WPC was about 478 million pounds, down by 2.7% from that of 2019. On the contrary, production in milk plants witnessed a surge due to panic buying, which stabilized after April 2020. The production of dry whey for the animal feed sector is stable as prices remain unchanged. Although WPC production is stable, some market players expect higher prices for higher-concentration WPC in the next few quarters, which is likely to impact production positively.

United States Whey Protein Ingredients Industry Overview

The United States Whey Protein Ingredients Market is fragmented, with the top five companies occupying 22.28%. The major players in this market are Arla Foods amba, Fonterra Co-operative Group Limited, Glanbia PLC, Groupe Lactalis and Koninklijke FrieslandCampina NV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Hydrolyzed

- 4.1.3 Isolates

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 RTE/RTC Food Products

- 4.2.2.1.7 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agropur Dairy Cooperative

- 5.4.2 Arla Foods amba

- 5.4.3 Carbery Food Ingredients Limited

- 5.4.4 Dairy Farmers of America

- 5.4.5 Fonterra Co-operative Group Limited

- 5.4.6 Glanbia PLC

- 5.4.7 Grande Cheese Company

- 5.4.8 Groupe Lactalis

- 5.4.9 Hilmar Cheese Company Inc.

- 5.4.10 Hoogwegt Group

- 5.4.11 Koninklijke FrieslandCampina NV

- 5.4.12 MEGGLE GmbH & Co.KG

- 5.4.13 Morinaga Milk Industry Co. Ltd

- 5.4.14 Talley's Group Limited

- 5.4.15 Tatua Co-operative Dairy Company Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 222 Pages

- 納期

- 2~3営業日