|

市場調査レポート

商品コード

1644855

インドのモバイル決済-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Mobile Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのモバイル決済-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

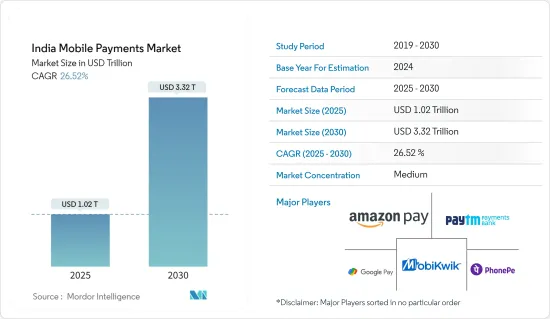

インドのモバイル決済市場規模は2025年に1兆200億米ドルと推定され、予測期間中(2025~2030年)のCAGRは26.52%で、2030年には3兆3,200億米ドルに達すると予測されます。

主要ハイライト

- eコマース事業の拡大と全国的なスマートフォンの普及が市場成長につながります。オンラインショッピングのためのインターネット利用の拡大は、予測期間を通じて市場拡大の原動力となると考えられます。全国の事業者が決済方法をモバイルフレンドリーにすることで、市場成長の可能性が生まれます。

- Worldlineによると、インドではUPIの加盟店導入が急速に進んでおり、UPIのP2M(個人対加盟店)取引の平均チケットサイズは着実に増加しているが、P2P(個人対個人)取引のATSは減少しています。しかし、これは取引量とP2M取引へのシフトによるものです。P2M取引のUPIトランザクションは、2022年1月の40.3%から2023年6月には57.5%に上昇し、UPIトランザクション全体に占める割合は今後も伸び続けると予想されています。

- さらに、RBIは施策声明「RBIが規制するPFMISの規制と施策」を通じて、CPMI(Committee on Payments and Market Infrastructures)と証券監督者国際機構(International Organization of Securities Commissions)が共同で発表したPFMISを承認しました。その結果、システム上重要な決済システム/システム包括的重要決済システムに指定されたRBI認可の決済システム、証券決済システム、ccps、中央証券保管機関、取引保管機関はすべて、PFMI基準に準拠することが義務付けられました。RBIが所有・運営するRTGSとNEFTシステムは、PFMI基準に従って定期的に評価・公表されなければならないです。

- Web 3.0は第三世代のウェブ技術であり、構造化されたデータとインテリジェントなサービスを統合し、ウェブがユーザーの目標を理解し、達成することに焦点を当てています。決済のセグメントでは、Web 3.0を活用することで、利用者によりインテリジェントでカスタマイズ型決済体験を提供することができます。例えば、Web 3.0技術を活用すれば、自然言語処理(NLP)や音声コマンドを使用してユーザーが決済を行えるようになり、端末に決済内容や金額を伝えることができるようになります。

- COVIDの流行が始まる前から、デジタル決済の導入は進んでいた。しかし、準備銀行の動きとパンデミックによる新たな後押しがこの変化を早め、非接触型決済やオンライン決済が大幅に増加する結果となりました。効果的なデジタル決済の戦略と運用は、決済エコシステムに依存または参加しているすべての組織にとって不可欠です。最新の技術が提供するデジタル決済は非接触型であり、法制上の柔軟性もあるため、何百万人ものインド人が決済時に社会的距離を置くことができます。もう一つの注目すべき動向は、小規模企業によるデジタル決済の導入です。過去2年間で、デジタル決済を利用する小売業者が500%以上増加したというデータがあります。

- さらに、インドでは、さまざまな業種の企業が世界の貿易を導入しているため、国境を越えた貿易が増加しています。しかし、クロスボーダー取引の複雑さが市場の成長を妨げています。ほとんどのクロスボーダー取引はコルレス銀行との関係を通じて処理されているため、運用コストと取引量の増加は、デジタル決済システムやモバイル決済システムなど、他の決済手段の採用をさらに加速させています。国際貿易の増加、生産の国際化、国境を越えたeコマースは、この地域で国境を越えたデジタル決済の需要が引き続き拡大することを示唆しています。しかし、ある国からによる国へのデジタル決済は、手続きが複雑なため、国内決済に比べてコストが高く、時間がかかり、透明性が低いです。

インドのモバイル決済市場動向

eコマースの活況がインド・モバイルウォレット市場の成長を促進

- インドの小売産業では、高級品のショッピングが徐々に人気を集めています。旅行がより制限されるようになり、オフラインショッピングが輝きを失う中、インドのDarveysのような老舗企業は、ファッションショッパーにとって新たな高級品の聖地となっています。オフラインからオンラインショッピングへのシフトは、高級品オンライン参入企業の売上を増加させました。消費者は今でも、高級品や珍しいものを手に入れるために新しい方法を試すことを楽しみにしています。例えば、IBEFによると、インドのeコマース市場は2026年までに2,000億米ドルに成長すると予想されています。デジタルに接続されたインドの買い物客の間では、国際的なブランドや外国製品への大きな需要があり、一般商品の流入量の増加に対応するための先進的自動倉庫への大きな注文が生み出されています。このようなオンラインショッピングの増加は、調査された市場を牽引すると予想されます。

- 政府は中小企業に対し、eコマースサイトや政府が運営・所有するGeM(Government e-Marketplace)を通じて製品を販売するよう奨励しました。多くの省庁やPSU(公共部門)はGeMから調達しています。India Brand Equity Foundationによると、2022年7月14日現在、GeMportalは、6万1,208の買い手組織に対し、473万人の登録サービス提供者と売り手から、2兆6,653億インドルピー(約332億8,000万米ドル)相当の約1,055万件の注文を提供しています。

- 政府電子市場(GeM)プラットフォームは、2022年6月、6万632の顧客に、456万人の登録売り手とサービス提供者から1,035万件、2億5,835億9,000万ルピー(330億7,000万米ドル)の注文を提供しました。DPIIT(Department for Promotion of Industry and Internal Trade)は、eコマースプラットフォームにおける小売業者のオンボーディングプロセスをシステム化するため、ONDC(Open Network for Digital Commerce)を利用して、カタログ作成、ベンダー発見、価格発見のためのプロトコルを確立する計画だと報じられています。国家と国民により大きな利益をもたらすため、同省はすべての市場参入企業にeコマース・エコシステムを最大限に活用する公平な機会を与えようとしています。

- California Life Sciencesによると2021年度にインド人がeコマースに費やした金額は410億米ドルを超えました。これは2026年度には1,290億米ドルを超えると予測されています。オンライン消費総額は、2021年度の720億米ドルから2026年度には2,370億米ドルを超えると予測されています。これらにより、国内外の参入企業が市場シェアを獲得するために新しいソリューションを開発する機会が生まれると予想されます。

- ここ数年、金融セグメントに特化した技術新興企業がいくつか登場し、私たちの購買方法を破壊しています。例えば、インドでは、アプリベースのウォレットやAadhaar/UPIと連動した即時取引からシングルウィンドウのeコマースアプリまで、フィンテックスタートアップ企業は脅威に留意し、アプリの堅牢なデータセキュリティのフレームワークの構築に投資する必要があります。このような新興企業は、資金繰りに苦労している可能性があり、一般的に、必要以上のデジタルセキュアなエコシステムに必要な多額の投資を避けているため、この問題に対処する必要があります。これは、大予算の包装に対してカスタマイズ型価値主導のサービスを提供するサイバーセキュリティ企業との協力によって対処する必要があります。

近接型決済が大きな市場シェアを占めると予想される

- 近接型決済は、決済の円滑化のために近距離無線通信(NFC)技術を使用します。NFCはスマートフォン内の小型アンテナで構成され、NFCリーダー(非接触POS)との双方向通信を可能にし、非接触決済取引を行っています。NFCの採用は、NFC対応スマートフォンのベースが拡大していることと、非接触クレジットカード/デビットカードをサポートするPOSインフラがすでに確立されていることが背景にあります。

- 使いやすいアプリを開発することで、Appleは広く採用されています。この試みは、非接触カードの写真をクリックするだけで簡単に登録できるようにしました。また、携帯電話やスマートウォッチで利用できるため、端末を介した迅速な決済が可能になりました。また、Apple Payが機能するNFC信号と連動する新しいPOSシステムの普及により、米国で利用可能な他の決済形態(Starbucks、Android Payなど)を上回ることができました。

- 近接モバイルベースの決済は、新型スマートフォンの大半がNFCチップを搭載し、店舗数が増加するかどうかにかかっています。このような技術が主流で使用されるようになれば、消費者は携帯電話を使って売り場で商品やサービスを直接購入できるようになります。さらに、COVID-19インパクトは、決済端末に物理的に触れる必要性を減らすため、NFCベースの非接触決済の潜在的な方法となります。また、デンマークの商店では、政府当局が病気の蔓延を遅らせるためにコンタクトレスやモバイル決済を義務付けているのと並行して、現金の代わりにコンタクトレス方式で支払うことを顧客に奨励しています。

- さらに小売業者は、顧客にとっての導入と利用の相対的な容易さと、小売業者にとっての導入の容易さに基づいて、採用とサポートするモバイル決済ソリューションを決定する必要があります。小売産業全体では、スマートフォンを利用できる若い世代を含む世界の人口が、オンラインショッピングと同様に店舗でのショッピングの利便性を求める主要な原動力となっていると見ています。

- インド準備銀行によると、インドでは昨年、BHIM UPI QRコードの利用が約1億2,800万件増加しました。BHIMは、National Payments Corporation of Indiaが作成した決済ソフトウェアで、統一決済インターフェース(Unified Payment Interface)を介した簡単な取引を促進します。このような緩やかな成長は、予測期間中、調査対象市場を牽引すると予想されます。昨年度は、インド全土で約710億件のデジタル決済が記録されました。これは、過去3年間と比べて大幅に増加しました。

インドのモバイル決済産業概要

インドの決済市場は、複数の参入企業が存在するため、競争は緩やかです。同市場の参入企業は、製品ポートフォリオを拡大し、地理的範囲を広げ、市場競合を維持するために、製品革新、合併、買収などの戦略を採用しています。

2023年9月、インドの著名なオンライン決済ソリューション・プロバイダーであるPayUは、WhatsAppと提携し、WhatsApp Businessプラットフォームを利用する企業にネイティブでシームレスなオンライン決済体験を記載しています。企業は現在、カード、UPI、ネットバンキングを含む150以上の決済手段をWhatsAppプラットフォーム上で提供することができ、PayUのCheckoutエクスペリエンスを利用することでリダイレクトの必要はありません。この機能は、WhatsAppと連携している全てのPayU加盟店でご利用いただけます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- インドのモバイル決済市場の市場規模・推定

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- eコマースの活況がインドのモバイルウォレット市場の成長を促進

- スマートフォン所有者とインターネット利用者の増加が市場成長を牽引

- 政府の積極的な取り組み

- 市場課題

- 貧弱なインターネット接続性とセキュリティ問題

- 市場機会

- キャッシュレス社会への移行

- モバイル決済産業における主要規制と基準

- 産業におけるビジネスモデルの分析

- 増加するモバイルウォレットの市場浸透に関する分析

- 実現技術に関する分析(NFC、QRなどを含む範囲)

- モバイルコマースの成長と市場への影響に関する解説

第6章 市場セグメンテーション

- タイプ別(相対的な普及率による市場シェア)

- 近接型

- 遠隔型

第7章 競合情勢

- 企業プロファイル

- PAYTM PAYMENTS BANK LIMITED(Paytm)

- PhonePe

- Alphabet Inc.(Google Pay)

- Amazon Payments, Inc.(Amazon Pay)

- ICICI Bank Limited(ICICI Pockets)

- Freecharge Payment Technologies Pvt. Ltd.

- State Bank of India(Yono SBI)

- Bharti Airtel(Airtel Money)

- HDFC Bank Limited(HDFC PayZapp)

- Meta Platforms, Inc.(WhatsApp pay)

第8章 投資分析

第9章 市場の将来展望

The India Mobile Payments Market size is estimated at USD 1.02 trillion in 2025, and is expected to reach USD 3.32 trillion by 2030, at a CAGR of 26.52% during the forecast period (2025-2030).

Key Highlights

- The expanding e-commerce business and the increased prevalence of smartphones nationwide can be linked to market growth. The growing internet use for online shopping will likely drive market expansion throughout the forecast period. Businesses nationwide are making their payment methods mobile-friendly, resulting in market growth potential.

- According to Worldline, with merchant adoption of UPI rising rapidly in India, the average ticket size of UPI P2M (person to merchant) transactions is steadily increasing, while ATS for P2P (person to person) transactions is decreasing. However, this is due to the volume of transactions as well as a shift to P2M transactions. P2M transactions UPI transactions have risen to 57.5 percent in June 2023 from 40.3 percent in January 2022 and are expected to keep growing, of complete UPI transactions.

- Further, through its policy statement "Regulation and Supervision of PFMIS Regulated by RBI," the RBI has approved the PFMIS published jointly by the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions. As a result, all RBI-authorized payment systems designated as systemically important payment systems/system comprehensive vital payment systems, as well as Securities Settlement Systems, ccps, Central Securities Depositories, and Trade Repositories, are required to adhere to the PFMI standards. The RBI-owned and operated RTGS and NEFT systems must be evaluated and published regularly in accordance with the PFMI criteria.

- Web 3.0 is the third generation of web technology, focusing on integrating structured data and intelligent services for the web to comprehend and fulfill user goals. In the area of payments, Web 3.0 can be leveraged to provide users with more intelligent and tailored payment experiences. Web 3.0 technology, for example, can be leveraged to enable users to make payments using natural language processing (NLP) and voice commands, allowing them to tell their devices what and how much they intend to pay.

- The adoption of digital payments was increasing before the commencement of the COVID pandemic. Still, Reserve Bank actions and the additional thrust supplied by the pandemic have hastened the change, resulting in a substantial increase in contactless and online payments. Effective digital payments strategy and operations are critical for all organizations that rely on or participate in the payments ecosystem. Because of the contactless nature of digital modes offered by modern technologies and legislative flexibility, crores of Indians can practice social distancing when making payments. Another noteworthy trend is the adoption of digital payments by small firms. Data reveals a more than 500% growth in retailers taking digital payments over the last two years.

- Additionally, cross-border trade increases in India as companies across industries adopt global trade. However, the complexities of cross-border commerce have hampered the market's growth. As most cross-border transactions are handled through correspondent banking relationships, increasing operational costs and trade volumes further accelerate the adoption of other payment methods, such as digital and mobile payment systems. The increase in international trade, internationalization of production, and cross-border e-commerce suggest that demand for digital cross-border payments will continue to grow in the region. However, digital payments from one country to another are costlier, slower, and less transparent than domestic payments due to the complexity involved in the procedure.

India Mobile Payments Market Trends

Booming E-Commerce Sector Propelling the India Mobile Wallet Market Growth

- In India's retail industry, luxury shopping is progressively gaining traction. As travel has grown more constrained and offline shopping has lost its shine, established enterprises, such as Darveys, in India have become the new luxury sanctuary for fashion shoppers. The shift from offline to online shopping has increased the sales of luxury online players; consumers are still looking forward to trying new ways to get their hands on luxury and rare things. For instance, According to IBEF, the Indian e-commerce market is expected to grow to USD 200 billion by 2026. There is a significant demand for international brands and foreign products among digitally connected Indian shoppers, creating substantial orders for advanced automated warehouses to handle the increased inflow of general merchandise volumes. Such a rise in online shopping is expected to drive the studied market.

- The government encouraged the MSMEs to market their products on the E-commerce site and through the Government e-Marketplace (GeM), which is run and owned by the government. Many Ministries and PSUs (public sector undertakings) source their procurement from GeM. As of July 14, 2022, according to the Indian Brand Equity Foundation, the GeMportal had served about 10.55 million orders worth INR 266,533 crores (USD 33.28 billion) from 4.73 million registered service providers and sellers for 61,208 buyer organizations.

- The Government e-Marketplace (GeM) platform provided 60,632 customers with 10.35 million orders of Rs. 258,359 crores (USD 33.07 billion) from 4.56 million registered sellers and service providers in June 2022. The Department for Promotion of Industry and Internal Trade (DPIIT) is reportedly planning to use the Open Network for Digital Commerce (ONDC) to establish protocols for cataloging, vendor discovery, and price discovery in an effort to systematize the onboarding process of retailers on e-commerce platforms. For the nation's and its citizens' greater benefit, the department seeks to give all market participants equitable chances to utilize the e-commerce ecosystem to its fullest potential.

- According to California Life Sciences. Indians spent more than USD 41 billion on e-commerce in the fiscal year 2021. This was predicted to exceed USD 129 billion by the fiscal year 2026. Total online consumption is predicted to rise from 72 billion dollars in 2021 to more than 237 billion dollars in the fiscal year 2026. These are expected to create an opportunity for the local and international players to develop new solutions to capture the market share.

- Over the past few years, several technology start-ups specializing in the financial segment have emerged, disrupting how we make purchases. For instance, in India, from app-based wallets and Aadhaar/UPI-linked instant transactions to single-window e-commerce apps, fintech start-ups need to be mindful of the threats and invest in creating a robust data security framework for the apps. This needs to be addressed as these may be boot-strapped start-ups and generally avoid the hefty investment needed for a more than essential digitally secure ecosystem. This needs to be addressed by collaboration with cybersecurity firms that provide customized and value-driven services against the big-budget packages.

Proximity Payment is Expected to Hold Major Market Share

- Proximity payment uses Near Field Communication (NFC) technology for payment facilitation. It consists of a small antenna within a smartphone that allows bi-directional communication with NFC readers (contactless POS) to perform contactless payment transactions. Its adoption is favored by the growing NFC-enabled smartphone base and by the already established underlying POS infrastructure supporting contactless credit/debit cards.

- By developing a user-friendly app for the same, Apple is adopted widely. The attempt made the registration easy by clicking a picture of the contactless card. And availability over the phone or smartwatch enables swift payments over the terminal. The company also has been able to surpass the other payment forms available in the US (Starbucks, Android Pay, etc.) from the spread of new point-of-sale (POS) systems that work with the NFC signals Apple Pay functions on.

- Proximity mobile-based payment depends on the vast majority of new smartphones being equipped with an NFC chip and an increasing number of outlets. The mainstream usage of such technology will enable consumers to purchase goods and services directly at the point of sale using their mobile phones. Further, the COVID-19 impact is a potential way for NFC-based contactless payments as it will reduce the need to touch a payment terminal physically. Also, shops in Denmark are encouraging customers to pay with contactless methods instead of cash, alongside government officials mandating contactless and mobile payments to slow the spread of disease.

- Retailers, in addition, are required to decide on the mobile payment solution to adopt and support based on the relative ease of adoption and use for customers and on the ease of implementation for the retailer. The overall retail industry observes that the global population with the younger generation of smartphone-enabled consumers are among the prime drivers demanding shopping convenience in-store as they enjoy online.

- According to the Reserve Bank of India, in the last year, acceptance of the BHIM UPI QR code had increased by approximately 128 million in India. BHIM is a payment software created by the National Payments Corporation of India to facilitate simple transactions over the Unified Payment Interface. Such gradual growth is expected to drive the studied market over the forecasted period. In the last financial year, around 71 billion digital payments were recorded across India. This was a significant increase compared to the previous three years.

India Mobile Payments Industry Overview

The Indian payment market is moderately competitive owing to the presence of multiple players. The players in the market are adopting strategies like product innovation, mergers, and acquisitions to expand their product portfolio, expand their geographic reach, and primarily stay competitive in the market.

In September 2023, PayU, a prominent online payment solutions provider in India, partnered with WhatsApp to offer native and seamless online payment experiences for companies using the WhatsApp Business platform. Businesses can currently offer clients 150+ payment choices, including cards, UPI, and net banking, all within the WhatsApp platform without needing redirection by using PayU's Checkout experience. This feature is now available to all PayU merchants with WhatsApp integration without charging additional setup or maintenance costs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Sizing and Estimates of India Mobile Payments Market

- 4.3 Industry Attractiveness-Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of COVID-19 Impact on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Booming E-Commerce Sector Propelling the India Mobile Wallet Market Growth

- 5.1.2 An Increase in Smartphone Owners and Internet Users Will Drive Market Growth.

- 5.1.3 Favorable Government Initiatives

- 5.2 Market Challenges

- 5.2.1 Poor Internet Connectivity and Security Issues

- 5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.4 Key Regulations and Standards in the Mobile Payments Industry

- 5.5 Analysis of Business Models in the Industry

- 5.6 Analysis of the Increasing Market Penetration of Mobile Wallets

- 5.7 Analysis on Enabling Technologies (Coverage to include NFC, QR, etc.)

- 5.8 Commentary on the growth of Mobile Commerce and its influence on the Market

6 MARKET SEGMENTATION

- 6.1 BY TYPE (Market share in percentage based on relative adoption)

- 6.1.1 Proximity

- 6.1.2 Remote

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PAYTM PAYMENTS BANK LIMITED (Paytm)

- 7.1.2 PhonePe

- 7.1.3 Alphabet Inc. (Google Pay)

- 7.1.4 Amazon Payments, Inc. (Amazon Pay)

- 7.1.5 ICICI Bank Limited (ICICI Pockets)

- 7.1.6 Freecharge Payment Technologies Pvt. Ltd.

- 7.1.7 State Bank of India (Yono SBI)

- 7.1.8 Bharti Airtel (Airtel Money)

- 7.1.9 HDFC Bank Limited (HDFC PayZapp)

- 7.1.10 Meta Platforms, Inc. (WhatsApp pay)