|

市場調査レポート

商品コード

1644817

日本のモバイル決済:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Japan Mobile Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のモバイル決済:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

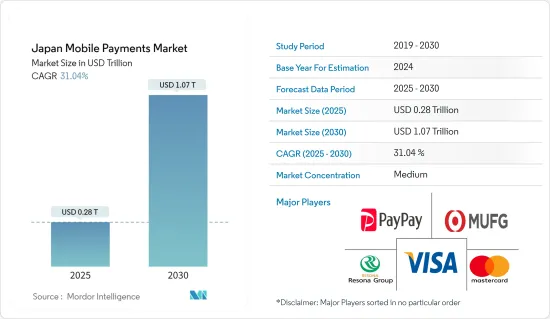

日本のモバイル決済市場規模は2025年に2,800億米ドルと推定され、予測期間(2025-2030年)のCAGRは31.04%で、2030年には1兆700億米ドルに達すると予測されます。

日本の国民はテクノロジーをいち早く採用することで知られています。現代の電子商取引に熱心に参加し、キャッシュレス決済の2つの主要技術である近距離無線通信(NFC)とQRコードの発明者でもあります。史上初のモバイルウォレットも20年前に日本で発売されました。

主なハイライト

- さらに、非接触型カードでの決済が容易になったことで、非接触型カードと比較して、利用者の総支出行動が増加し、カードの利用が増加しました。しかし、モバイルウォレットの活性化は、支出全体にはるかに深い影響を与えました。パンデミックは、モバイル決済の急速な普及により、非接触型決済への移行を加速させました。さらに、レストランやクイックサービスレストランでは、非接触型決済の利用率が驚くほど高かったです。

- 決済ビジネスはかつてない変化を目の当たりにしています。新たな決済ソリューション企業は既存企業と市場シェアを競い合い、テクノロジーを駆使して小売・卸売決済全体の伝統的なネットワークやビジネスモデルを破壊しています。その一方で、規制は強化され、決済プラットフォームや市場インフラは統合、刷新、再設計されています。

- 確かに、決済サービスを提供する携帯電話アプリケーションは、データ・プライバシーの危険に直面し続けています。セキュリティと信頼性を高めるため、企業は顧客の身元を確認するための、より迅速で安全なソリューションを常に模索しています。一部の企業は、運転免許証などの公的書類を統合してユーザーを認証し、架空または不正なアカウントを防止しようと躍起になっています。こうした動きがモバイル決済を強化しています。

- COVID-19以降、デジタル決済手段の受け入れが増加し、時間の経過とともに重要性を増すことが予想されました。政府や規制機関は、通貨がウイルスを媒介する可能性があると考え、通貨の使用を禁じています。例えば、政府が封鎖措置を取って以来、日本では現金の使用が半減し、生活必需品を扱う店舗では現金取引が避けられるようになった。

日本のモバイル決済市場動向

Mコマースプラットフォームの開発とインターネット普及率の上昇が市場を牽引

- 日本のモバイル決済環境を牽引しているのは、日本のネットワークとインターネットインフラの拡大です。携帯電話やインターネットへのアクセスが向上した結果、国内の小規模店舗や日常的なサービスではモバイル決済が標準となりつつあります。

- インターネットの急速な普及により、調査対象市場の繁栄が予想されます。インターネット・サービス・プロバイダーによる投資の増加により、インターネット普及率はここ数年好調に推移しており、今後も同じ軌道をたどると予想されます。

- 日本は、5Gインターネット・インフラをいち早く導入した国のひとつです。ネットワーク・インフラの拡大を促すため、政府は帯域を積極的に割り当て、必要な行政・財政支援を要請しました。

- インターネット利用の増加により、オンライン小売とeコマースの分野が最も著しい成長を遂げると予想されます。日本のeコマース市場は、2022年には6.9%増の1,943億米ドルになると予測されました。スマートフォンの利用率が上昇し、より包括的なオンライン・プレゼンスが確立されたことで、eコマースは成長し、調査対象のセクターに利益をもたらすと予想されます。

- Paytm、PhonePayなど複数のアプリがモバイル決済を可能にしています。銀行、店舗、小売店、ブランドは、顧客により良い、より効果的な支払いオプションを提供するためにモバイルアプリを立ち上げています。この側面が、調査対象市場をかなり牽引しています。

- 日本では、eコマースとモバイル決済ビジネスがともに急速な勢いで拡大しています。eコマース・プラットフォームやオンライン小売業者の急速な拡大は、消費者にモバイル決済の導入を促し、地域市場に影響を与えてきました。

デジタルウォレット(モバイルウォレットを含む)が成長を牽引

- オンライン請求書支払いやその他の送金サービスを可能にするその簡便性により、モバイルウォレットは日本全国でeコマース事業者に非常に普及しています。さらに、これらの最新機器を使用することで、迅速かつ安全な取引が可能になります。モバイルウォレットを利用するこれらの利点により、これらの製品の利用が増加しています。

- 予測期間中、この要因は調査対象市場に有利な機会を生み出すと予想されます。モバイルウォレットの顧客は、ユーザーフレンドリーなUIにより、簡単に送金や受け取りができます。モバイルウォレットのユーザーは、ユーザーフレンドリーなUIにより、外出先でも取引を完了できます。

- 代替デジタル通貨はすでにこの地域で急速に受け入れられており、中でも暗号通貨は最も需要が高いです。将来のデジタルウォレットは、こうした代替デジタル資産へのオンデマンドかつ摩擦のないアクセスを提供し、決済取引を保存・可能にします。さらに、こうした多くの決済ソースを利用した金融取引や、現金の保管も可能になります。

- ペイメントゲートウェイの統合は、今日、さまざまな業界のあらゆる企業にとって最も不可欠なコンポーネントの1つです。さらに、予測される期間を通じて、市場の拡大はオンライン取引の増加によって促進されると予想されています。膨大な量のデジタル決済を維持するために必要なエコシステムを強化する重要な進歩は、信頼性の高い通信インフラの構築に注力することで支えられてきました。インドのヤフーやアマゾンのように、このような進歩の恩恵を受けている企業は、デジタルウォレットを利用した支払いにリベートを提供し、顧客にこれらのサービスを選択するよう促しています。

日本のモバイル決済業界の概要

日本のモバイル決済市場は半固定的で、サービス・プロバイダー間の熾烈な競争が見られます。複数の通信事業者が、携帯電話経由での支払いを受け入れるために、現在のアプリとの接続を可能にしています。通信事業者は、自社製品を携えて市場に参入しようと躍起になっています。日本を通じて、エコシステムには他のエコシステムからの新たな参加者が増えています。

- 2023年11月-MastercardとNECが店舗でのバイオメトリクス決済を推進するために戦略的パートナーシップを締結。締結された覚書により、このパートナーシップは、NECの顔認証および生体認証技術と、Mastercardの決済の実現および最適化されたユーザーエクスペリエンスを実装し、世界な規模拡大を推進します。

- 2023年10月りそなHDの子会社であるりそなケーサイサービスの株式の一部を取得し、りそなグループとの共同販売体制を強化。りそなグループとの連携により、当社はりそなグループの顧客に対して最新の決済ソリューションを提供し、りそなグループは当社グループの顧客に対して金融ソリューションを提供します。りそなケーサイサービスに対する当社の出資比率は15%から20%となります。株式取得の条件(譲渡株式数、取得価額等)については、りそなHDと当社が別途協議の上、合意します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の利害関係者分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 日本における決済環境の進化

- 日本におけるキャッシュレス決済の拡大に関連する主な市場動向

- COVID-19が日本の決済市場に与える影響

- 主要事例と使用事例の分析

第5章 市場力学

- 市場促進要因

- 購買力の向上と日本におけるインターネット普及率の上昇に支えられたmコマースや越境ECの台頭を含むeコマースの高い普及率が市場を牽引

- 市場抑制要因

- 特に国境を越えた取引の場合、標準的な立法政策が欠如しています。

- 市場機会

- キャッシュレス社会への移行

- 新規参入企業によるイノベーションが普及を促進

- モバイル決済業界における主な規制と基準

- 日本の決済業界に関連する主要な人口動向とパターンの分析(人口、インターネット普及率、銀行普及率/非銀行人口、年齢、所得などを網羅)

- 日本における顧客満足度重視の高まりと世界の動向の融合に関する分析

- 日本における現金離れと非接触決済の台頭に関する分析

第6章 市場セグメンテーション

- 決済モード別

- POS

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- 現金

- その他の販売店

- オンライン販売

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- その他のオンライン販売(代金引換、銀行振込、Buy Now, Pay Laterを含む)

- POS

- エンドユーザー産業別

- 小売

- エンターテインメント

- ヘルスケア

- ホスピタリティ

- その他のエンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- PayPay

- Visa Inc.

- MasterCard Inc.

- Mitsubishi UFJ Financial Group

- Resona Holdings

- Rakuten Group Inc.

- Credit Saison

- Aeon Credit Service

- JCB

- PayPal

第8章 投資分析

第9章 今後の動向

The Japan Mobile Payments Market size is estimated at USD 0.28 trillion in 2025, and is expected to reach USD 1.07 trillion by 2030, at a CAGR of 31.04% during the forecast period (2025-2030).

The population of Japan is known for being early technology adopters. They are eager participants in modern eCommerce, as well as an inventor of two key cashless payments technologies Near field communication (NFC) and QR Codes. The first-ever mobile wallet was also launched in Japan two decades ago.

Key Highlights

- Moreover, The ease of payment with contactless-enabled cards led to an increase in the total spending behavior of users and increased use of the card compared to the non-contactless-enabled card. However, activating mobile wallets had a far deeper impact on overall spending. The pandemic accelerated the transition toward contactless payment with the rapid adoption of mobile payments. Further, the usage of contactless payments was incredibly high in restaurants and quick-service restaurants.

- The payments business is witnessing unprecedented change. New payment solution companies compete with incumbents for market share and use technology to disrupt traditional networks and business models across retail and wholesale payments. On the other hand, regulations are increasing, and payment platforms and market infrastructures are consolidating, renewing, and re-designing.

- To be sure, the mobile phone applications that offer payment services continue to face danger from data privacy. To increase the security and dependability of their policies, businesses are always looking for quicker and safer solutions to identify the identities of their customers. Some companies are eager to integrate official papers, such as driver's licenses, etc., to authenticate users and prevent fictitious or fraudulent accounts. These actions are enhancing mobile payments.

- After COVID-19, it was anticipated that acceptance of digital payment methods would increase and become more significant over time. Governments and regulatory agencies forbid currency usage because it is thought to be a possible virus carrier. For instance, since the government imposed a lockdown, cash usage in Japan decreased by half, and stores that sold necessities avoided cash transactions.

Japan Mobile Payments Market Trends

Development of M-Commerce Platforms and Increasing Internet Penetration in Japan Driving the Market

- Japan's mobile payment environment is driven by the nation's expanding network and internet infrastructure. As a result of improved cellular and internet access, mobile payments are becoming the standard in the nation's small shops and everyday services.

- Because of the internet's quick spread, the market under investigation is anticipated to prosper. Due to increased investments by internet service providers, the internet penetration rate has been strong over the previous few years and is expected to continue on the same trajectory.

- Japan was one of the first nations to install 5G internet infrastructure in their areas. To encourage the expansion of network infrastructure, the government actively allocated the bands and requested the necessary administrative and financial assistance.

- The online retail and e-commerce sectors are expected to experience the most significant growth due to rising internet usage. Japan's e-commerce market was projected to increase 6.9% to USD 194.3 billion in 2022. With rising smartphone usage and a more comprehensive online presence, e-commerce is expected to grow and benefit the sector under study.

- Several apps, including Paytm, PhonePay, etc., enable mobile payments. Banks, shops, retail outlets, and brands have launched mobile apps to provide customers with better and more effective payment options. This aspect has considerably driven the market under study.

- In Japan, e-commerce and the mobile payments business are both expanding at a rapid rate. The rapid expansion of e-commerce platforms and online retailers has had and will likely continue to impact local markets, pushing consumers to embrace mobile payments.

Digital Wallet (includes Mobile Wallets) to Witness the Growth

- Due to their simplicity in enabling online bill payments and other money transfer services, mobile wallets are becoming extremely popular all over Japan for e-commerce businesses. Additionally, the usage of these modern instruments enables quick and secure transactions. These advantages of utilizing a mobile wallet have led to increased use of these products.

- During the forecast period, this factor is anticipated to create lucrative opportunities in the studied market. Customers of mobile wallets can transfer and receive money with ease due to the user-friendly UI. Users of mobile wallets can finish their transactions even while on the go due to the user-friendly UI.

- Alternative digital currencies are already quickly embraced in the region, with cryptocurrencies being the most in demand. Future digital wallets will offer on-demand and frictionless access to these alternative digital assets and store and enable payment transactions. Furthermore, they will make it possible to carry out financial transactions using these many payment sources and keep this cash.

- Integrating a payment gateway is one of the most essential components of every firm in various industries today. Furthermore, throughout the projected period, market expansion has been anticipated to be fueled by increased online transactions. The crucial advancement in fortifying the ecosystem required to sustain enormous volumes of digital payments has been supported by the focus on building a reliable communication infrastructure. Companies that have benefited from such advances, like Yahoo and Amazon in India, are providing rebates on payments made using digital wallets, encouraging customers to choose these services.

Japan Mobile Payments Industry Overview

The Japanese mobile payments market is semi-consolidated, demonstrating fierce competition between the service providers. Several communication firms are enabling connection with their current apps to accept payments via cell phones. Telecom companies are eager to enter the market with their products. Through Japan, the ecosystem is seeing new participants from other ecologies grow.

- November 2023 - Mastercard and NEC collaborated to advance in-store biometric payments strategic partnership between Mastercard and NEC Corporation. Through a signed Memorandum of understanding, the partnership will implement NEC's face recognition and liveness verification technology and Mastercard's payment enablement and optimized user experience to drive global scale.

- October 2023 - Resona HD to acquire a partial share of Resona Kessai Service, a subsidiary of Resona HD, strengthening the joint sales structure with Resona Group. In collaboration with Resona Group, the Company will provide its latest payment solutions to Resona Group's clients, and Resona Group will provide its financial solutions to the company group's clients. The Company's shares in Resona Kessai Service will range from 15% to 20%. The terms and conditions of the share acquisition, including the number of shares to be transferred and the acquisition price, will be agreed upon through separate discussions between Resona HD and the Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in the country

- 4.5 Key market trends pertaining to the growth of cashless transaction in Japan

- 4.6 Impact of COVID-19 on the payments market in the country

- 4.7 Analysis of major case studies and use-cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Proliferation of E-commerce, including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power andand Increasing Internet Penetration in Japan Driving the Market

- 5.2 Market Restraints

- 5.2.1 Lack of a standard legislative policy remains especially in the case of cross-border transactions

- 5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Mobile Payments Industry

- 5.5 Analysis of key demographic trends and patterns related to the payments industry in Japan (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age and Income, etc.)

- 5.6 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in Japan

- 5.7 Analysis of cash displacement and rise of contactless payment modes in Japan

6 MARKET SEGMENTATION

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, and Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Other Points of Sale

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PayPay

- 7.1.2 Visa Inc.

- 7.1.3 MasterCard Inc.

- 7.1.4 Mitsubishi UFJ Financial Group

- 7.1.5 Resona Holdings

- 7.1.6 Rakuten Group Inc.

- 7.1.7 Credit Saison

- 7.1.8 Aeon Credit Service

- 7.1.9 JCB

- 7.1.10 PayPal