米国のゲーム機と付属品:市場シェア分析、産業動向、成長予測(2025~2030年)

United States Gaming Console & Accessories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643023

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

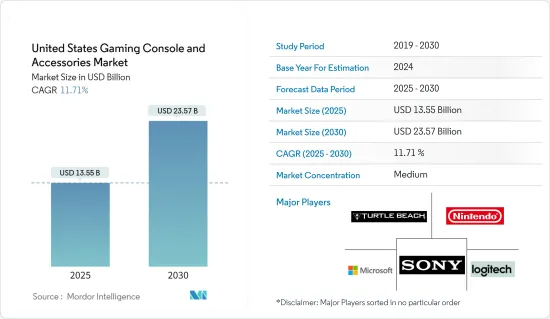

米国のゲーム機と付属品市場規模は2025年に135億5,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは11.71%で、2030年には235億7,000万米ドルに達すると予測されます。

ゲーム産業における継続的な技術進歩が、ゲーム機と付属品市場の拡大を後押ししています。米国のゲーム開発者は、ゲーマーの体験を向上させようと絶えず努力しており、その結果、PlayStation、Xbox、Windows PCなど、さまざまなコンソール/プラットフォーム向けのコードを発表したり書き換えたりして、1つの製品に組み込み、クラウドプラットフォームを通じてゲーマーに提供しています。

主要ハイライト

- eスポーツの急成長により、先進的なゲーミングキーボードやゲームパッドの需要が高まっています。ゲーミング付属品市場は、ゲームコンテンツの継続的な強化により、予測期間中に成長すると予想されます。

- 3DやAR/VRゲームのような新しい技術の統合が市場を牽引しています。ゲーム機はもはや、キャラクターが2次元空間で戦い、ミッションをこなし、敵を征服することに限定されるものではないです。バーチャルリアリティは、ビデオゲームを現実の3D世界と融合させる技術です。ファンタジーと現実の境界線をなくすVRは、技術に貪欲な今日のゲーマーのために、より現実的で没入感のあるゲーム世界の創造に役立っています。

- クラウドゲーミングは、ゲーム産業全体の新たな技術であり、ユーザーは、高速ネットワーク接続により、ノートパソコン、タブレット、携帯電話などの携帯端末でハイエンド・ゲームをストリーミングできるため、定期的なハードウェアのアップグレードやゲーム機/PCの購入が不要になります。こうした要因は、長期的には市場の成長に悪影響を及ぼすと予想されます。

- COVID-19の封鎖により、人々は家に閉じこもり、一部の人々は時間を過ごすためにゲームプラットフォームに目を向けた。これらのプラットフォームは、オンライントラフィックでより多くの新規訪問者を集め、様々なゲーム付属品の需要を創出しました。さらに、COVID-19の封鎖期間中にゲームが増えたことで、新しいゲームのリリースが急増しました。パンデミック後は、国内で新しいゲームコンテンツが発売され、市場が急成長しています。

米国ゲーム機・付属品市場動向

高グラフィックを要求する新しいゲームコンテンツの発売が市場成長を牽引

- ビジュアルニーズの高い新しいゲームコンテンツの発売が市場を牽引。コンソールゲームからオンデマンド映像エンターテインメントへの移行はすでに始まっています。

- さらに、ゲーミングキーボードは、進化と複数の製品発売によって際立ち、メーカーの競合を高め、ゲーマーにさまざまな選択肢を提供しています。各社は、ゲーマーのゲーム体験を向上させるため、RGBライト付きゲーミングキーボードの開発に注力しています。

- さらに、ゲーム機は他のプラットフォームとは比較にならないほど洗練されたグラフィック出力を提供しています。エンターテインメントソフトウェア協会によると、米国のゲーマーの63%は、購入の決め手の大半をグラフィック品質に置いています。4K映像をサポートする機能は、ゲーム機に恩恵をもたらしました。

- ビデオゲームはもはや若者だけの趣味ではないです。ビデオゲームが生活の一部として当たり前のものとして育った世代が増えたことで、典型的なゲーマーの年齢も上がっています。エンターテインメントソフトウェア協会の世論調査によると、ビデオゲーム・参入企業の36%が18歳から34歳で、65歳以上が6%を占めています。昨年、15歳から19歳のアメリカ人は、1日平均1.44時間をゲームや余暇のパソコン利用に費やしました。45歳から54歳の年齢層は、ビデオゲームのプレイ時間が最も短いです。この年齢層は、毎日0.28時間しかコンピューターで遊んでいないです。

- 国内の主要企業は新技術を提供し、戦略的提携を結び、市場拡大を推進しています。例えば、2022年5月、大手ゲーミングオーディオ付属品プロバイダーの1つであるタートルビーチ・コーポレーションは、ベストセラーのタートルビーチ・コンソールゲーミング付属品と受賞歴のあるROCCAT PCゲーミング付属品ブランドが、ニューオーリンズ・セインツの先発セイフティ選手であるチョーンシー・ガードナー・ジョンソンと提携したと発表しました。ガードナー-ジョンソン氏は、NBAのスター選手であるグレイソン-アレン氏、イマニュエル-クイックリー氏、ジョシュ-ハート氏などのプロアスリートゲーマーに加わり、デジタル戦場で優位に立つために必要なすべてのゲーム機器のためにタートルビーチ社とROCCATと提携しました。

ゲーミングコンソールセグメントが大きな市場シェアを占める

- ゲーミングコンソールは、米国における参入企業の増加と技術の向上により、近年継続的に需要を伸ばしています。ゲームの数や多様性が増すにつれ、消費者がゲームに費やす時間も増加しています。また、常に新しいコンテンツが生み出されています。

- 米国はビデオゲームをプレイする人が最も多い国です。2022年、Entertainment Software Associationは、米国人の66%、全年齢のアクティブなビデオゲーム参入企業は2億1,550万人以上と推定しています。ビデオゲームを毎週プレイする個人の平均数に関して。エンタテインメントソフトウェア協会のデータによると、米国のこの数字は週に13時間です。

- さらに、米国では52%の人がゲーム専用機を使ってゲームをプレイしているといいます。ゲーム専用機を使用しているゲーマーの数に関して、ゲーム専用機はそのアカウントで2位にランクされています。

- さらに、ビデオゲームはゲーマーが友人や家族とコミュニケーションをとるための一般的な手段でもあります。2022年の世論調査によると、米国ではゲーマーの83%がオンラインや直接会って他人とプレイしており、2020年の65%から増加しています。米国のゲーマーによると、オンラインで遊ぶ相手は友人が最も多いです。

- 市場は家庭用ゲーム機が独占しており、Sony、Microsoft、Nintendoといった複数の企業が産業を支配しています。ソニーは次世代システムPS5向けに、新しいコントローラ、ヘッドセット、コントローラスタンド、メディアリモコンなど、ゲーム機の人気を高める周辺機器を多数発表しました。

米国ゲーム機と付属品産業概要

米国のゲーム機と付属品市場は細分化されており、Sony Corporation、Microsoft株式会社、Nintendo、Logitech International S.A.、Turtle Beach Corporationなどの大手企業が参入しています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年12月、著名なASTRO A50シリーズのコンソール用ゲーミングヘッドセットの第5弾であるLogitech G ASTRO A50 X LIGHTSPEED Wireless Gaming Headset and Base Stationが、米国を拠点とするLogitechのブランドであり、ゲーミング技術とギアのスペシャリストであるLogitech Gから発売されました。

- 2023年11月、世界有数のゲーミンググループであるFaZe Holdings, Inc.とゲーミング及びesports周辺機器の世界参入企業であるSteelSeriesは、現在Best Buy小売店でのみ販売されているFaZe Clan x SteelSeriesと呼ばれる共同ブランドの新しいゲーミング製品ラインの発売を発表しました。Arctis Nova 7ワイヤレスヘッドセット|FaZeクランエディション、Apex 9ミニキーボード|FaZeクランエディション、Aerox 3ワイヤレスマウス|FaZeクランエディション、QcK Heavy XXL|FaZeクランエディションはこのパートナーシップで提供されるいくつかの製品です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- COVID-19の産業への影響評価

第5章 市場力学

- 市場促進要因

- グラフィック要件の高い新しいゲームコンテンツの発売

- 3DやAR/VRゲームのような新技術の統合

- 市場抑制要因

- クラウドゲームサービスからの脅威の増加

- モバイルベースのプラットフォームに対する需要の高まり

第6章 米国におけるゲーム市場全体のシナリオ

第7章 年齢・性別によるゲーム人口の人口統計学的分析

第8章 市場セグメンテーション

- タイプ別

- ゲーム機

- 付属品

第9章 競合情勢

- 企業プロファイル

- Sony Corporation

- Microsoft Corporation

- Nintendo Co., Ltd.

- Logitech International S.A.

- Turtle Beach Corporation

- Razer Inc.

- Corsair Components Inc.

- Mad Catz Global Limited

- Kingston Technology Corporation

- Performance Designed Products LLC

- PowerA

第10章 市場機会と今後の動向

目次

The United States Gaming Console & Accessories Market size is estimated at USD 13.55 billion in 2025, and is expected to reach USD 23.57 billion by 2030, at a CAGR of 11.71% during the forecast period (2025-2030).

Continuous technological advancements in the gaming industry are driving the expansion of the gaming console and accessories market. Game developers in the United States continually strive to enhance gamers' experience, thereby launching and rewriting codes for various consoles/platforms, such as PlayStation, Xbox, and Windows PC, incorporated into one product and provided to the gamers through the cloud platform.

Key Highlights

- The rapid growth of e-sports has increased the demand for advanced gaming keyboards and gamepads. The gaming accessories market is expected to grow over the forecast period with the continuous enhancement of gaming content.

- Integration of newer technologies, Like 3D and AR/VR gaming, is driving the market. The gaming console is no longer limited to characters fighting battles, completing missions, and conquering foes in two-dimensional space. Virtual reality is where technology meshes video games with the real 3D world. Diminishing the lines between fantasy and reality, VR is helping create gaming worlds that are more realistic and immersive for today's technology-obsessed gamers.

- Cloud gaming is an emerging technology across the gaming industry, allowing users to stream high-end games across hand-held devices, such as laptops, tablets, and mobiles, with fast network connectivity, thereby eliminating the requirement for a regular hardware upgrade or a gaming console/PC. Such factors are anticipated to have a negative impact on market growth in the long term.

- Due to the COVID-19 lockdown, people stayed home, and some turned to the gaming platform to spend their time. These platforms attracted more new visitors in online traffic and created a demand for various gaming accessories. Furthermore, the increase in gaming during the COVID-19 lockdown came with a surge in new game releases. Post-pandemic, the market was growing rapidly with the launch of new gaming content in the country.

US Gaming Console & Accessories Market Trends

Launch Of New Gaming Content With High Graphic Requirements Drives the Market Growth

- The release of new game content with high visual needs drives the market. The move from console gaming to on-demand visual entertainment has already begun.

- Furthermore, gaming keyboards are distinguished by advancements and multiple product launches, boosting manufacturer competitiveness and offering gamers various options. Companies are concentrating on creating RGB-lit gaming keyboards to improve gamers' gaming experiences.

- Moreover, gaming consoles offer sophisticated graphics output that is unmatched by other platforms. According to the Entertainment Software Association, 63% of gamers in the United States base their purchasing decisions mostly on graphic quality. The ability to support 4K video benefited gaming consoles.

- Video gaming is no longer a hobby exclusively for the young. The typical gamer's age has increased as generations have grown up with video gaming as a normal part of life. According to an Entertainment Software Association poll, 36% of video game players are between 18 and 34, with 6% being 65 and older. Last year, Americans aged 15 to 19 spent an average of 1.44 hours per day on gaming or leisurely computer use. The 45 to 54-year-old age group played the least quantity of video games. Members in this age range spend only 0.28 hours playing on the computer daily.

- The key players in the country are offering new technologies, making strategic partnerships, and propelling market expansion. For example, in May 2022, one of the leading gaming audio and accessory provider Turtle Beach Corporation announced its best-selling Turtle Beach console gaming accessories and award-winning ROCCAT PC gaming accessories brands have partnered with New Orleans Saints' starting Safety, Chauncey Gardner-Johnson. Gardner-Johnson joins other pro-athlete gamers, including NBA stars Grayson Allen, Immanuel Quickley, and Josh Hart, who have teamed up with Turtle Beach and ROCCAT for all their gaming equipment needs can dominate on the digital battlefield.

Gaming Console Type Segment Holds Significant Market Share

- Gaming consoles have continuously increased demand in recent years, owing to increased players and technical improvements in the United States. The amount of time consumers spend gaming has increased as the number of games and their diversity has grown. In addition, new content is constantly being generated.

- The United States had the most people who played video games. In 2022, the Entertainment Software Association estimated that 66% of Americans and over 215.5 million active video game players of all ages are in the United States. In terms of the average number of individuals that play video games weekly. According to data from the Entertainment Software Association, this number in the United States is 13 hours per week.

- The report further mentioned that 52 % of the people in the US use dedicated gaming consoles to play games. The gaming consoles ranked second in their account regarding the number of gamers using dedicated consoles.

- Moreover, Video games are a common way for gamers to communicate with friends and family. According to a 2022 poll, 83 percent of gamers in the United States played with others online or in person, up from 65 percent in 2020. According to US gamers, friends are the most common people to play online with.

- The market is dominated by home consoles, with several firms like Sony, Microsoft, and Nintendo dominating the industry. Sony announced a host of new peripherals for its next-generation system, the PS5, including a new controller, headset, controller stand, and media remote-the growing popularity of gaming consoles.

US Gaming Console & Accessories Industry Overview

The United States Gaming Console & Accessories Market is fragmented, with major players like Sony Corporation, Microsoft Corporation, Nintendo Co., Ltd., Logitech International S.A., and Turtle Beach Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In December 2023, the fifth iteration of the prominent ASTRO A50 Series console gaming headset, the Logitech G ASTRO A50 X LIGHTSPEED Wireless Gaming Headset and Base Station, was released by Logitech G, a United States-based brand of Logitech and a specialist in gaming technologies and gear.

- In November 2023, FaZe Holdings, Inc., a prominent gaming group in the world, and SteelSeries, a global player in gaming and esports peripherals, announced the launching of a new line of co-branded gaming products called FaZe Clan x SteelSeries, which are currently only available at Best Buy retail locations. Arctis Nova 7 Wireless Headset | FaZe Clan Edition, Apex 9 Mini Keyboard | FaZe Clan Edition, Aerox 3 Wireless Mouse | FaZe Clan Edition, QcK Heavy XXL | FaZe Clan Edition are a few offerings provided in the partnership.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Launch Of New Gaming Content With High Graphic Requirements

- 5.1.2 Integration Of Newer Technologies Like 3D and AR/VR Gaming

- 5.2 Market Restraints

- 5.2.1 Increasing Threat From Cloud Gaming Services

- 5.2.2 Rising Demand For Mobile-based Platform

6 OVERALL GAMING MARKET SCENARIO IN UNITED STATES

7 DEMOGRAPHIC ANALYSIS OF GAMING POPULATION BY AGE AND GENDER

8 MARKET SEGMENTATION

- 8.1 By Type

- 8.1.1 Gaming Console

- 8.1.2 Accessories

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Sony Corporation

- 9.1.2 Microsoft Corporation

- 9.1.3 Nintendo Co., Ltd.

- 9.1.4 Logitech International S.A.

- 9.1.5 Turtle Beach Corporation

- 9.1.6 Razer Inc.

- 9.1.7 Corsair Components Inc.

- 9.1.8 Mad Catz Global Limited

- 9.1.9 Kingston Technology Corporation

- 9.1.10 Performance Designed Products LLC

- 9.1.11 PowerA

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日