アルコール飲料包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Alcoholic Beverage Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1629780

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

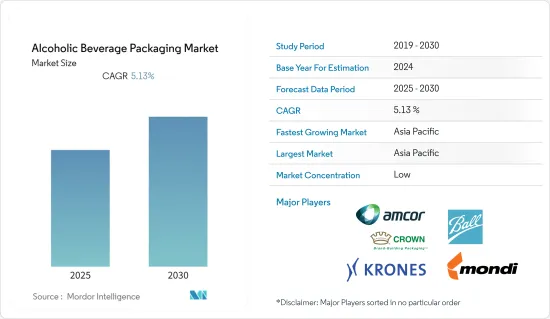

アルコール飲料包装市場は予測期間中にCAGR 5.13%を記録する見込み

主要ハイライト

- アルコール飲料の世界の消費量は、ここ数十年で大幅に増加していることが確認されています。Lancetが実施した調査によると、国民1人当たりのアルコール消費量は1990年の59リットルから2017年には世界全体で65リットルに増加しました。さらに、その後の13年間で、一人当たりのアルコール消費量は17%増加し、2030年には76リットルに達すると予想されています。アルコール飲料消費の増加は、市場成長を促進する主要な要因の1つです。

- さらに、包装廃棄物を最小限に抑えるため、100%リサイクル可能な製品の使用に関する意識のおかげで、包装のリサイクルへの注目が高まっています。このため、サステイナブル包装製品に対する需要が高まり、アルコール飲料包装市場の成長を支えています。

- しかし、危険物や非生分解性製品の使用に関する政府の厳しい規制により、製造業者は一部の包装材料に限定されています。さらに、生産コストの増加も調査対象市場の成長を制限しています。

アルコール飲料包装市場の動向

ガラス包装が大きなシェアを占める

- ガラスは品質と頑丈さを損なうことなく100%リサイクル可能です。利用されたガラス瓶の大半は、新しいガラス瓶の生産に使用されます。ワイン包装における重要性の高まりと市場の堅調な需要により、ガラス容器の需要は拡大する可能性があります。

- 世界的に消費されるアルコールの50%以上はワインの形で消費されており、OIVは世界的にワインの生産量が17%増加すると予測しています。顧客はバッグ・イン・ア・ボックス(BiB)のような代替包装のワインを受け入れ始めているが、大量購入に限られています。

- 2019年4月に発表されたWine Institute of Americaの報告書によると、米国では2017年に約10億ガロンのワインが生産されました。米国はワインの消費量が最も多く、世界シェアは15%です。したがって、ガラス包装セグメントは、ワイン包装用途を支配しています。

- さらに、ビール産業は、過去数年間で着実な成長を示しています。成長するビール産業は、おそらくガラス包装セグメントに大きな発展を示すかもしれません。例えば、欧州では、全体のリサイクル材料のうち、ガラスは紙に次いで、2017年に22%のシェアを獲得しました。

アジア太平洋が市場を独占する見込み

- 同地域ではビールやスピリッツ飲料の消費が増加しており、これが市場成長の大きな要因となっています。WHOは、インドのアルコール消費者の92%がビールやワインよりも蒸留酒を好むと発表しています。各社がサステイナブル包装製品を志向する中、この地域ではアルコール飲料用のガラス製包装の採用が拡大しています。

- 中国やインドのような人口の多い国の存在、可処分所得の増加、新興国でのアルコール消費の受け入れ拡大によって強化されたこの地域の巨大な消費者基盤は、調査した市場の成長を促進する主要要因です。

- Lancetの調査によると、東南アジアと西太平洋における一人当たりのアルコール消費量は、1990~2017年にかけてそれぞれ104%と54%増加しました。アジアの人口中央値は30.7歳で、アルコール飲料市場に巨大な潜在機会をもたらし、アルコール飲料包装の需要を増大させています。

アルコール飲料包装産業概要

アルコール飲料の包装ソリューションを提供する企業が複数存在することで、市場の競争は激化しています。そのため、市場は適度に細分化されており、多くの企業が拡大戦略を展開しています。

- 2019年4月-Diageo PLCは、プラスチック廃棄物の最小化に焦点を当て、同社のビールブランドであるGuinnessについて、全世界でプラスチック包装を使用しないと発表しました。同社はこの動きと、プラスチックに代わる100%リサイクル可能で生分解性の段ボールの採用のために1,600万ユーロを投資する予定。

- 2019年3月-Amcor LimitedはライバルのBemis CompanyInc.を買収しました。この2つのマーケットリーダーを組み合わせることで、Amcorは株主、顧客、従業員、環境に対してより強力な価値提案を行うことを目指しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- アルコール飲料消費の増加

- リサイクルへの注目の高まり

- 製品の長期保存に対する需要の高まり

- 市場抑制要因

- 包装材料に関する厳しい規制の実施

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 材料別

- ガラス

- 金属

- プラスチック

- その他

- 製品別

- 缶

- ボトル

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- その他

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Amcor PLC

- Ball Corporation

- Krones AG

- Mondi PLC

- Crown Holdings Inc.

- Sidel SA

- Oi SA

- Ardagh Group SA

- Berry Global Inc.

- Nampak Limited

- Stora Enso Oyj

- Gerresheimer AG

第7章 投資分析

第8章 市場機会と今後の動向

目次

Product Code: 56567

The Alcoholic Beverage Packaging Market is expected to register a CAGR of 5.13% during the forecast period.

Key Highlights

- It was observed that the global consumption of alcoholic beverages has been increasing significantly, over the decades. According to the study conducted by Lancet, alcohol per-capita consumption increased from 59 liters in 1990 to 65 liters in 2017, globally. Furthermore, in the following 13 years, alcohol per-capita consumption is expected to grow by 17%, reaching 76 liters in 2030. The rising alcoholic beverage consumption is one of the key factors driving market growth.

- Additionally, owing to the awareness regarding the usage of 100% recyclable products, in order to minimize packaging waste, the focus on recycling packagings is growing. This is, thus, fuelling the demand for sustainable packaging products and supporting the growth of the alcoholic beverage packaging market.

- However, stringent government regulations on the use of hazardous and non-biodegradable products have limited the manufacturers to a few packaging materials. Furthermore, the increasing cost of production is also restricting the growth of the market studied.

Alcoholic Beverage Packaging Market Trends

Glass Packaging Segment to Account for a Crucial Share

- Glass is 100% recyclable without the loss of quality and sturdiness. The majority of utilized glass bottles are used for the production of new glass bottles. The demand for glass containers may likely expand, owing to its increasing importance in wine packaging and robust demand in the market.

- More than 50% of the alcohol consumed globally is in the form of wine, and OIV has projected a 17% growth in the production of wine, globally.Though the customers have started accepting wine in alternative packagings, like Bags in a Box (BiB), it is limited to bulk purchasing.

- According to the report by the Wine Institute of America, released in April 2019, almost 1 billiongallons of wine wereproduced in the United States in 2017. The United States isthe highest consumerof wine,with a 15% global share. Thus, the glass packaging segment dominates the wine packaging application.

- Additionally, the beer industry has shown steady growth over the past years. Thegrowing beer industry may possibly show significant development in the glass packaging segment. For instance,in Europe, out of the overall recycling materials, glass captured 22% share in 2017, after paper.

Asia-Pacific Region is Expected to Dominate the Market

- The increasing consumption of beer and spirit drinks in the region has been a significant factor for the growth of the market. WHO has stated that 92% of the alcohol consumers in India prefer spirits over beer and wine. As the players are moving toward sustainable packaging products, the adoption of glass packaging for alcoholic beverages is growing in the region.

- The huge consumer base in the region, reinforced by the presence of highly populated countries, like China and India, increasing disposable incomes, and the growing acceptance of alcohol consumption in developing nations are the major factors driving the growth of the market studied.

- The study by Lancet has stated that per capita alcohol consumption in Southeast Asia and West Pacific increased by 104% and 54%, respectively, from 1990 to 2017. The Asian population represents the median age of 30.7 years, which presents huge potential opportunities for the alcoholic beverages market, thus augmenting the demand for alcoholic beverage packaging.

Alcoholic Beverage Packaging Industry Overview

The availability of several players providingpackagingsolutions for alcoholic beverages has intensified the competition in the market. Therefore, the market is moderately fragmented, with many companies developing expansion strategies.

- Apr 2019 -Diageo PLCannounced that it will not be using plastic packaging, globally, for its beer brand, Guinness, with a focus on minimizing plastic waste. The company is planning to invest EUR 16 million for this move and for the introduction of 100% recyclable and biodegradable cardboard to replace plastic.

- Mar 2019 - Amcor Limited acquired its rival Bemis CompanyInc. By combining these two market leaders, Amcor aims tocreate a stronger value proposition for shareholders, customers, employees, and the environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Consumption of Alcoholic Beverages

- 4.2.2 Increased Focus on Recycling

- 4.2.3 Rising Demand for Long Shelf Life of the Product

- 4.3 Market Restraints

- 4.3.1 Implementation of Stringent Regulations on Packaging Materials

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Glass

- 5.1.2 Metal

- 5.1.3 Plastic

- 5.1.4 Other Materials

- 5.2 By Product

- 5.2.1 Cans

- 5.2.2 Bottles

- 5.2.3 Other Products

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 Unites States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Latin America

- 5.3.4.2 Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor PLC

- 6.1.2 Ball Corporation

- 6.1.3 Krones AG

- 6.1.4 Mondi PLC

- 6.1.5 Crown Holdings Inc.

- 6.1.6 Sidel SA

- 6.1.7 Oi SA

- 6.1.8 Ardagh Group SA

- 6.1.9 Berry Global Inc.

- 6.1.10 Nampak Limited

- 6.1.11 Stora Enso Oyj

- 6.1.12 Gerresheimer AG

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

アルコール飲料包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日