|

市場調査レポート

商品コード

1627138

北米のガラス瓶/容器:市場シェア分析、産業動向、成長予測(2025~2030年)North America Glass Bottles/Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のガラス瓶/容器:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

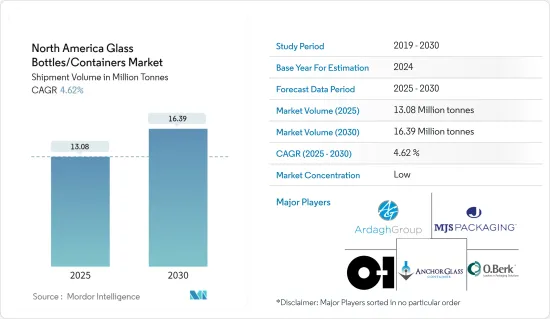

北米のガラス瓶/容器市場規模(出荷量ベース)は、2025年の1,308万トンから2030年には1,639万トンに拡大し、予測期間(2025~2030年)のCAGRは4.62%と予測されます。

主要ハイライト

- 北米のガラス瓶/容器市場は、飲食品、化粧品、医薬品などのセグメントでの消費拡大に牽引され、拡大基調にあります。消費者が安全で健康的な包装をますます優先するようになるにつれ、ガラスは多様なカテゴリーに進出しています。特に飲料セグメントではその傾向が顕著で、高級品や工芸飲料はガラス瓶入りであることが多いです。

- さらに、エンボス加工、成形、芸術的仕上げの最先端技術がガラス包装の魅力を高めています。このような技術革新は、カスタマイズやブランディングを強化するだけでなく、目立つ包装を目指す企業にとってガラス容器を有力な選択肢にしています。産業の軽量ガラス技術への取り組みは、輸送コストの懸念や環境への影響に対処するものであり、市場の拡大にさらに拍車をかけています。

- 米国では、アルコール飲料の消費量が急増し、包装、特にガラス瓶への需要が高まっています。この需要は、アルコール飲料タイプの拡大と、消費者の高級包装志向を反映しています。ガラス瓶が好まれるのは、リサイクル性や高級感のためだけでなく、飲料の品質や味を保持する能力が高いためでもあります。クラフトビールの動向と職人技を駆使したスピリッツの出現は、最高級のガラス製包装に対する欲求を増幅させています。

- 2023年全米薬剤乱用・健康調査(NSDUH)のデータによると、米国の成人2億1,870万人(18歳以上の84.9%)がアルコールを摂取した経験があることが明らかになっています。このような大きな消費者基盤は、飲料セグメントにおける多様な包装ソリューションに対する安定した需要を保証しています。汎用性と訴求力のあるガラス瓶は依然として主流であり、メーカーは生産者と消費者双方の嗜好の変化に対応するために技術革新を行っています。

- Glass Globalの報告によると、北米のガラス瓶/容器の生産量はセクターを問わず838万9,233トンで、年間生産能力は932万1,370トンでした。これは、この地域がガラス包装セグメントで確固たる存在感を示していることを強調しています。堅調な生産能力と生産量は、強力なインフラだけでなく、飲食品、医薬品、化粧品などの産業にまたがる旺盛な需要をも示しています。

- さらに、国際貿易センターのデータによると、米国は約14万1,143トンのガラス包装を輸出しています。これはガラス包装のセグメントで急成長している機会を示しているだけでなく、北米のガラス製品に対する国際的な需要を強調しています。大幅な国内生産と大幅な輸出の組み合わせは、北米のガラス包装産業の強さと成長軌道を際立たせています。

- この地域では、ガラス瓶/容器が様々なセグメントで採用されるようになり、リサイクルが重要な焦点となっています。飲食品、医薬品、化粧品などの産業では、ガラス瓶/容器の使用量が増加しているため、ガラス廃棄物が大量に発生しています。効率的なリサイクルは、廃棄物管理、環境への影響の最小化、持続可能性の推進に不可欠です。政府の規制がサステイナブル包装に傾いているため、メーカーはますますガラス製ソリューションに目を向けるようになっています。これらの力学が北米のガラス包装市場の成長を後押ししています。

北米のガラス瓶/容器市場の動向

アルコール飲料セグメントが大きな成長を遂げる見込み

- アルコール飲料メーカーはガラス瓶入りの新製品を発売しており、この動きは市場にプラスの影響を与えると予想されます。ガラス包装を採用することで、これらのメーカーは製品の魅力を高め、消費者の認識を再構築し、ガラスに関連する高級イメージを活用することを目指しています。ガラス瓶は、製品の味や品質をより効果的に保つだけでなく、リサイクル性の向上や高級感も記載しています。多くの消費者は、ガラス製包装を優れた飲料品質と同一視しており、しばしばプレミアム価格を正当化しています。

- さらに、ガラスはユニークで独創的なボトルデザインを可能にするため、ブランドは店頭で差別化を図ることができます。

- ガラス包装への移行は、持続可能で環境に優しい選択肢を求める消費者ニーズの高まりと共鳴するものです。

- 例えば、2024年9月、Diageo傘下のJohnnie Walkerは、スコッチウイスキー用に調整された世界最軽量の700mlガラス瓶を披露する限定版「Blue Label Ultra」を発表しました。この先駆的な包装は、サステイナブルウイスキー瓶詰めの顕著な飛躍を示すものです。

- 北米のビール包装セグメントは、進化する文化動向、人口増加、都市化、若年層におけるビール人気の急上昇の影響を大きく受けています。継続的な投資と地域間のビール流通網の拡大は、こうした動向を維持し、ガラス瓶/容器市場を活性化させる可能性があります。

- 2024年3月から5月にかけて、米国の瓶ビールと缶ビールの生産量は1,041万バレルから1,247万バレルの間で変動しており、包装ビールに対する米国の需要を裏付けています。2023年に米国のビール生産量と輸入量が5%減少し、クラフトビールメーカーの数量が1%減少した市場はビール消費量の増加傾向に支えられています。

- 生産量と輸入量の落ち込みは、消費者の嗜好の変化、経済的要因、または規制の変更に起因する可能性があります。しかし、ビール消費量の増加は、産業の未開拓の成長とイノベーションの可能性を示唆しており、おそらく新しいビール品種、マーケティングの強化、消費者行動の進化によって拍車がかかると考えられます。

- 北米では、サステイナブルライフスタイルを取り入れる消費者の層が拡大しており、特にプラスチック廃棄物を抑制する取り組みが盛んです。この動きは、ワイン・スピリッツ市場のガラス瓶へのシフトを後押ししています。多くの消費者は、ガラス瓶をプラスチック製よりも環境に優しく、高級な製品であると認識しています。こうした認識は環境意識の高い消費者の共感を呼び、サステイナブル包装に割高な対価を支払うことを厭わないケースも多いです。さらに、プラスチック使用量の抑制を目的とした政府規制が間近に迫っており、アルコール飲料セグメントでのガラス瓶の需要がさらに高まる可能性があります。

米国が主要市場シェアを占める見込み

- 米国は世界最大の包装市場の一つであり、飲食品、パーソナルケア、医薬品など様々な産業向けにガラス瓶や容器を製造する主要企業が数多く存在します。同国の経済成長と食品、飲料、医薬品、パーソナルケア製品に対する消費支出の増加が、ガラス瓶・容器包装ソリューションの需要を牽引しています。

- この動向は、持続可能でリサイクル可能な包装オプションへの嗜好の高まりによってさらに後押しされており、ガラスはその環境に優しい特性から好まれています。ビールや蒸留酒を中心とするクラフト飲料産業の成長も、特殊なガラス製包装の需要拡大に寄与しています。高齢化社会の進展と医療の進歩による医薬品セグメントの拡大も、厳しい安全・保存基準を満たす高品質のガラス容器へのニーズを高めています。

- 米国は、好調な経済、包括的なビジネス移民制度、多様な消費者層、イノベーション主導の文化、ビジネスフレンドリーな施策により、ベンチャー企業にとって有利な環境を提供しています。これらの要因により、米国は事業の拡大や新設を目指す起業家や企業にとって魅力的な進出先となっています。強固なインフラ、先進的技術セグメント、資本へのアクセスは、さまざまな業種の企業にとってさらに魅力を高めています。

- eコマースプラットフォームの成長と消費者行動の進化は、オンライン小売業者にとって大きなビジネス機会となっています。デジタル市場は、インターネットの普及率、モバイル機器の利用率、ショッピング習慣の変化などを背景に、急速に拡大しています。こうした動向は、ガラス包装を含む様々な産業に潜在的なビジネス機会をもたらしています。

- 消費者の環境意識が高まり、サステイナブル解決策を求めるようになるにつれ、ガラス包装メーカーはリサイクル可能で再利用可能な容器の需要を生かすことができます。さらに、ニッチ市場における高級品や職人技を駆使した製品への嗜好の高まりは、ガラス包装の品質や美的魅力に合致することが多く、ガラス包装産業にさらなる成長の可能性をもたらしています。

- 米国では、ミレニアル世代とX世代がワイン消費の伸びを牽引しています。これらの消費者層はワインに対する嗜好を高めており、市場動向や商品提供に影響を与えています。彼らの嗜好や購買習慣の進化は、ワイン産業の方向性に大きな影響を与えています。米国におけるワインの小売総額は、2023年に約1,063億米ドルに達します。この大幅な数字は、アメリカのワイン市場の堅調な性質と継続的な拡大を反映しています。販売額の伸びは、消費の増加と、プレミアムまたは高価格のワイン製品へのシフトの可能性を示しています。

- この動向は、ワイン包装における高品質ガラス瓶への需要の増加を示しています。消費者の目が肥えるにつれ、ワイン製品の全体的なプレゼンテーションと品質が重視されるようになっています。ガラス瓶、特に優れた品質のものは、ワインの完全性を保ち、その価値を高める上で重要な役割を果たします。ワイナリーが高級包装ソリューションに対する消費者の期待に応えようとしているため、包装産業、特にガラスメーカーはこの動向から恩恵を受けると考えられます。

北米のガラス瓶/容器産業概要

北米のガラス瓶/容器市場はセグメント化されており、多数の世界的・地域的企業が市場シェアを争っています。このセグメントの主要企業には、O-I Glass, Inc.、Ardagh Group S.A.、MJS Packaging、Anchor Glass Container Corporationなどがあります。これらの企業や他の市場参入企業は、多様で競争的な状況に貢献しています。

市場の進化に伴い、サステイナブル競争優位性を維持・拡大するためには技術革新が不可欠となっています。企業は研究開発に投資し、製品の改良、製造プロセスの強化、消費者の需要の変化に対応しています。このような技術革新への注力は、軽量ガラス製造の進歩、リサイクル技術の向上、製品保護強化のための特殊コーティングの開発を促進しています。

持続可能性と環境への関心の高まりも、ガラス瓶/容器市場の重要な促進要因となっています。多くの企業が環境に優しい方法を採用し、ガラスのリサイクル可能性を重要なセールスポイントとして宣伝しています。この傾向は今後も競合情勢を形成し、市場力学に影響を与え続けると考えられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 容器用ガラスの輸出入データ

- 容器用ガラス市場のPESTEL分析

- 容器包装用ガラスの産業標準と規制

- 容器包装用ガラスの原料分析と材料考察

- 容器包装用ガラスの持続可能性動向

- 北米地域の容器用ガラス炉と立地

第5章 市場力学

- 市場促進要因

- 飲食品産業からの需要拡大

- 持続可能性とリサイクル性への取り組みがエンドユーザーのガラス包装需要を拡大

- 市場抑制要因

- ガラス製造による高いカーボンフットプリント

- 操業と物流に関する懸念

- 貿易シナリオ-ガラス瓶/容器産業の輸出入パラダイムの歴史と現状分析

第6章 市場セグメンテーション

- エンドユーザー産業別

- 飲料

- アルコール飲料(セグメント別定性分析)

- ビール・サイダー

- ワイン・スピリッツ

- その他のアルコール飲料

- ノンアルコール(セグメント別定性分析)

- 炭酸飲料

- 牛乳

- 水・その他ノンアルコール飲料

- 食品

- 化粧品

- 医薬品

- その他産業別

- 飲料

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- O-I Glass, Inc

- Ardagh Group S.A.

- Gerresheimer AG

- Arksansas Glass Container Corporation

- MJS Packaging

- O.Berk Company, L.L.C.

- Kaufman Container Company

- Burch Bottle & Packaging, Inc.

- Anchor Glass Container Corporation

- West Coast Container Inc.

- PGP Glass Private Limited

第8章 北米のガラス瓶/容器工場に供給する主要炉メーカーの分析

第9章 市場の将来展望

The North America Glass Bottles/Containers Market size in terms of shipment volume is expected to grow from 13.08 million tonnes in 2025 to 16.39 million tonnes by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

Key Highlights

- Driven by rising consumption in sectors like food and beverage, cosmetics, and pharmaceuticals, the North American container glass market is on an upward trajectory. As consumers increasingly prioritize safe and healthy packaging, glass has found its way into diverse categories. This is especially pronounced in the beverage sector, where premium products and craft beverages often come in glass bottles.

- Moreover, cutting-edge technologies in embossing, shaping, and artistic finishes are elevating the allure of glass packaging. Such innovations not only offer enhanced customization and branding but also make glass containers a go-to choice for companies aiming for standout packaging. The industry's push towards lightweight glass technologies addresses transportation cost concerns and environmental implications, further fueling market expansion.

- In the U.S., a surge in alcoholic beverage consumption is driving a robust demand for packaging, especially glass bottles. This demand mirrors the expanding range of alcoholic offerings and a consumer tilt towards premium packaging. Glass bottles are preferred not just for their recyclability and premium look, but also for their prowess in preserving beverage quality and taste. The craft beer trend and the emergence of artisanal spirits have amplified the appetite for top-tier glass packaging.

- Data from the 2023 National Survey on Drug Use and Health (NSDUH) reveals that 218.7 million U.S. adults (84.9% of those 18 and older) have consumed alcohol at some point. Such a significant consumer base ensures a steady demand for varied packaging solutions in the beverage sector. Glass bottles, with their versatility and appeal, remain dominant, and manufacturers are innovating to cater to the changing preferences of both producers and consumers.

- Glass Global reports that North America produced 8,389,233 tonnes of glass bottles and containers across sectors, with an annual capacity of 9,321,370 tonnes. This underscores the region's formidable presence in the glass packaging arena. The robust production capacity and volume signal not just a strong infrastructure but also a thriving demand, spanning industries like food and beverage, pharmaceuticals, and cosmetics.

- Additionally, data from the International Trade Centre highlights the U.S. exported around 141,143 tonnes of glass packaging. This not only points to a burgeoning opportunity in the glass packaging realm but also underscores the international demand for North American glass products, likely attributed to their quality and the region's manufacturing prowess. The blend of substantial domestic production and significant export figures accentuates the North American glass packaging industry's strength and growth trajectory.

- As container glass finds increasing adoption across sectors in the region, recycling has emerged as a critical focus. Industries like food and beverage, pharmaceuticals, and cosmetics are generating substantial glass waste due to their heightened use of container glass. Efficient recycling is vital for waste management, minimizing environmental impact, and championing sustainability. With government regulations leaning towards sustainable packaging, manufacturers are increasingly turning to glass solutions. Collectively, these dynamics are propelling the growth of North America's glass packaging market.

North America Glass Bottles/Containers Market Trends

Alcoholic Beverage Segment is Expected to Witness Significant Growth

- Alcohol manufacturers are rolling out new versions of their products in glass bottles, a move anticipated to positively influence the market. By adopting glass packaging, these manufacturers aim to boost product appeal and reshape consumer perceptions, capitalizing on the premium image associated with glass. Glass bottles not only preserve the product's taste and quality more effectively but also offer heightened recyclability and an upscale feel. Many consumers equate glass packaging with superior beverage quality, often justifying a premium price tag.

- Moreover, glass facilitates unique and creative bottle designs, allowing brands to differentiate themselves on store shelves.

- This pivot to glass packaging resonates with the rising consumer demand for sustainable and eco-friendly options, given that glass is entirely recyclable and boasts multiple reuse capabilities.

- For example, in September 2024, Diageo-owned Johnnie Walker unveiled a limited edition Blue Label Ultra, showcasing the world's lightest 700ml glass bottle tailored for Scotch whisky. This pioneering packaging marks a notable leap in sustainable whisky bottling.

- The North American beer packaging sector is largely influenced by evolving cultural trends, a growing population, urbanization, and a surge in beer's popularity among younger demographics. Continued investments and a broadening beer distribution network across regions are likely to uphold these trends, potentially invigorating the market for glass bottles and containers.

- From March to May 2024, U.S. beer production in bottles and cans fluctuated between 10.41 million and 12.47 million barrels, underscoring the nation's demand for packaged beer. Even though the U.S. witnessed a 5% dip in beer production and imports in 2023, and craft brewer volume sales fell by 1%, the market remains buoyed by a rising beer consumption trend.

- The dip in production and imports could stem from shifts in consumer preferences, economic factors, or regulatory changes. Yet, the uptick in beer consumption hints at untapped growth and innovation avenues in the industry, possibly spurred by new beer varieties, intensified marketing, or evolving consumer behaviors.

- In North America, a growing segment of consumers is embracing sustainable lifestyles, notably in their efforts to curb plastic waste. This movement is propelling the wine and spirits market's shift towards glass bottles. Many consumers view glass bottles as more eco-friendly than their plastic counterparts and associate them with premium product quality. This perception resonates with environmentally-conscious consumers, often willing to pay a premium for sustainable packaging. Furthermore, looming government regulations aimed at curbing plastic usage could further amplify the demand for glass bottles in the alcoholic beverage sector.

United States is Expected to Account for Major Market Share

- The United States represents one of the world's largest packaging markets, featuring numerous key players producing glass bottles and containers for various industries, including food and beverage, personal care, and pharmaceuticals. The country's economic growth and rising consumer expenditure on food, drinks, pharmaceuticals, and personal care products drive the demand for glass bottle and container packaging solutions.

- This trend is further supported by the increasing preference for sustainable and recyclable packaging options, with glass being favored due to its eco-friendly properties. The growing craft beverage industry, particularly in beer and spirits, has also contributed to the increased demand for specialized glass packaging. The pharmaceutical sector's expansion, driven by an aging population and advancements in healthcare, has also bolstered the need for high-quality glass containers that meet stringent safety and preservation standards.

- The United States offers a favorable environment for business ventures due to its strong economy, comprehensive business immigration system, diverse consumer base, innovation-driven culture, and business-friendly policies. These factors make the USA an attractive destination for entrepreneurs and companies looking to expand or establish new operations. The country's robust infrastructure, advanced technology sector, and access to capital further enhance its appeal for businesses across various industries.

- The growth of e-commerce platforms and evolving consumer behaviors present significant opportunities for online retailers. The digital marketplace has experienced rapid expansion, driven by increased internet penetration, mobile device usage, and changing shopping habits. This shift has created a fertile ground for businesses to reach a wider audience and implement innovative sales strategies.These trends create potential opportunities for various industries, including glass packaging.

- As consumers become more environmentally conscious and seek sustainable solutions, glass packaging manufacturers can capitalize on the demand for recyclable and reusable containers. Additionally, the growing preference for premium and artisanal products in niche markets often aligns well with the perceived quality and aesthetic appeal of glass packaging, presenting further growth prospects for the industry.

- In the United States, Millennial and Gen X consumers have been driving the growth in wine consumption. These demographic groups have shown an increasing preference for wine, influencing market trends and product offerings. Their evolving tastes and purchasing habits have significantly impacted the wine industry's direction. The total retail value of wine sales in the US reached approximately USD 106.3 billion in 2023. This substantial figure reflects the robust nature of the American wine market and its continued expansion. The sales value growth indicates increased consumption and a potential shift towards premium or higher-priced wine products.

- This trend indicates an increasing demand for high-quality glass bottles in wine packaging. As consumers become more discerning, there is a growing emphasis on the overall presentation and quality of wine products. Glass bottles, particularly those of superior quality, play a crucial role in preserving the wine's integrity and enhancing its perceived value. The packaging industry, especially glass manufacturers, will likely benefit from this trend as wineries seek to meet consumer expectations for premium packaging solutions.

North America Glass Bottles/Containers Industry Overview

The North America container glass market is fragmented, with numerous global and regional players competing for market share. Key companies in this space include O-I Glass, Inc., Ardagh Group S.A., MJS Packaging, and Anchor Glass Container Corporation. These firms and other market participants contribute to a diverse and competitive landscape.

As the market evolves, innovation has become crucial in maintaining and growing sustainable competitive advantage. Companies invest in research and development to improve product offerings, enhance manufacturing processes, and meet changing consumer demands. This focus on innovation drives advancements in lightweight glass production, improved recycling techniques, and the development of specialized coatings for enhanced product protection.

The increasing emphasis on sustainability and environmental concerns has also become a significant driver in the glass bottles and containers market. Many companies are adopting eco-friendly practices and promoting the recyclability of glass as a key selling point. This trend will likely continue shaping the competitive landscape and influencing market dynamics in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL Analysis of Container Glass Market

- 4.4 Industry Standard and Regulation For Container Glass Use For Packaging

- 4.5 Raw Material Analysis and Material Consideration For Packaging

- 4.6 Sustainability Trends For Glass Packaging

- 4.7 Container Glass Furnace and Location in North American Region

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from Food and Beverage Industry

- 5.1.2 Sustainability and Recyclability Initiatives Are Expanding End-Users Demand For Glass Packaging

- 5.2 Market Restraints

- 5.2.1 High Carbon Footprint due to Glass Manufacturing

- 5.2.2 Operation and Logistical Concerns

- 5.3 Trade Scenario - Analysis of the Historical and Current Export-Import Paradigm For Container Glass Industry

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical

- 6.1.5 Other End-user Verticals

- 6.1.1 Bevarages

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 O-I Glass, Inc

- 7.1.2 Ardagh Group S.A.

- 7.1.3 Gerresheimer AG

- 7.1.4 Arksansas Glass Container Corporation

- 7.1.5 MJS Packaging

- 7.1.6 O.Berk Company, L.L.C.

- 7.1.7 Kaufman Container Company

- 7.1.8 Burch Bottle & Packaging, Inc.

- 7.1.9 Anchor Glass Container Corporation

- 7.1.10 West Coast Container Inc.

- 7.1.11 PGP Glass Private Limited