|

市場調査レポート

商品コード

1693912

英国のガラス瓶・容器:市場シェア分析、産業動向、成長予測(2025~2030年)United Kingdom (UK) Glass Bottles and Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のガラス瓶・容器:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 133 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

英国のガラス瓶・容器市場規模は2025年に235万トンと推定され、2030年には271万トンに達すると予測され、予測期間(2025~2030年)のCAGRは2.94%です。

プラスチック包装技術は近年大きく進歩しました。それでもなお、高級アルコール飲料と非アルコール飲料の包装では、ガラスが支配的であり続けています。ガラスは蒸留酒などのアルコール飲料に最も好まれる包装材料のひとつです。製品の香りと風味を保つガラス瓶の能力が需要を牽引しています。

主要ハイライト

- 安全で健康的な包装に対する顧客ニーズの高まりが、様々なカテゴリーにおけるガラス製包装の成長を支えています。また、ガラスにエンボス加工を施し、形を整え、芸術的な仕上げを加える革新的な技術が、ガラス包装をエンドユーザーの間でより望ましいものにしています。さらに、エコフレンドリー製品に対する需要や飲食品市場からのニーズの高まりといった要因も、市場の成長を後押ししています。

- その上、消費者はビールやワインを好むようになっており、ガラス包装メーカーは生産量を調整しています。プレミアム飲食品ブランドは、ガラスが化学的に不活性で無孔性、不浸透性であることから、プラスチックなどの他の包装オプションよりもガラス(容器用ガラス)を好みます。

- プラスチックや金属などの代替包装形態の採用が増加していることは、予測期間における市場の成長に影響を与える顕著な要因の一つです。加えて、政府によって奨励されている再生プラスチック(rPET)ボトルの増加も、ガラス包装の採用にとって厳しい条件につながっています。

- Argus Mediaによると、2022年5月、英国の動きの速い消費財(FMCG)セクタの多くの企業やブランドは、プラスチック包装のリサイクル含有量を増やすことを目指しています。英国プラスチック連盟(BPF)は、英国のPETボトル市場における現在のリサイクル率の平均水準を15%~20%と見積もっています。

- Glass Alliance Europeによると、2年前の生産量は3,950万トンでした。これは、ガラスメーカーが、第三国との高い競合に加えて、エネルギー問題にも悩まされていることを示しています。2021年と比較すると、2022年のEU-27の輸出量は430万トンで4.6%減少したが、14.9%増加しました。EU-27の4大輸出先は、数量ベースでは英国(20%)を含むその他の欧州(59.5%)であり、それ以上の国々です。

- 国内各地で紙、プラスチック、金属などの代替包装形態の採用が拡大していることは、予測期間中の市場成長に影響を与える顕著な要因のひとつです。プラスチック製造技術の先進化と、バイオプラスチックのようなリサイクル性の高いプラスチックの出現は、さらにプラスチック包装の成長を促進すると予想されます。

英国のガラス瓶・容器市場の動向

最大のエンドユーザー産業は飲料

- ガラスは蒸留酒などのアルコール飲料に最も好まれる包装材料のひとつです。製品の香りと風味を保つガラス瓶の能力が需要を牽引しています。安全で健康的な包装に対する消費者の需要の高まりが、様々なカテゴリーにおけるガラス製包装の成長を後押ししています。また、ガラスにエンボス加工を施し、形を整え、芸術的な仕上げを加える革新的な技術が、エンドユーザーの間でガラス包装をより望ましいものにしています。

- ガラス瓶やガラス容器は、その化学的無菌性と非透過性から、主にアルコール飲料やノンアルコール飲料に使用されています。また、ガラスは重要なバリア材料であり、包装における透明性でも高いランクにあります。CO2の損失や酸素の侵入に耐えるため、長期保存可能な包装を作ることができます。ガラス瓶のフランジ性は、新しい加工やコーティングによって改善されてきました。最新の軽量化と強化技術により、ガラスの強度と消費者の利便性が向上しました。

- さらに、ワインの販売と消費はパンデミックの間に何倍にも増加し、販売されるワインのほとんどは標準的な750ミリリットル入りだが、小型ボトルなどの代替品も増えています。パンデミック(世界的大流行)の間にこの地域で酒類の消費量が増加したことは、ガラス瓶の需要に好影響を与えました。

- OEC(Observatory of Economic Complexity)によると、2023年4月の英国のガラス瓶の輸出は1,580万GBP(1,948万米ドル)、輸入は4,070万GBP(5,018万米ドル)で、全体では2,490万GBP(3,070万米ドル)の貿易赤字となりました。2022年4月から2023年4月にかけて、英国のガラス瓶の輸出は1,670万GBP(2,059万米ドル)から1,580万GBP(1,948万米ドル)に93万1,000GBP(114万7,965米ドル)、5.57%減少し、輸入は3,040万GBP(3,748万米ドル)から4,007万GBP(4,940万米ドル)に1,000万GBP(123万3,456.2米ドル)、33.9%増加しました。

- 主にアルコール・非アルコール飲料産業からの需要が、同国におけるガラス瓶輸入の増加を牽引しています。この増加は予測期間中も続くと予想されます。

フリントは色で主要市場シェアを占める

- ワイン、牛乳、ビール、ジュースなどの食品では、透明包装の利用が増加しています。この決定は、顧客が購入前に製品を検査することを好むというマーケティング上の提案によって推進されています。

- 英国では、再生ガラス製造の課題は、その難しさにあるのではなく、むしろリサイクル率の高い透明ガラス瓶を製造するのに必要な高品質の再生透明ガラス(カレット)の供給が不十分であることにあります。リサイクル率の高いガラス瓶を必要とする製品では、グリーンガラスが唯一の選択肢となります。濃色ガラスも有効な選択肢ではあるが、製品やブランドによっては適さない場合もあります。特に飲食品産業では、フリントまたはエクストラフリントと呼ばれる最高品質の透明ガラスが好まれます。

- リサイクル工場で混合色ガラスを分別する作業は、非常に時間とコストがかかります。その結果、粉々になった混合ガラスの破片は、新しいボトルに生まれ変わるのではなく、断熱材として役立つガラス繊維製品の製造に再利用されます。マルチストリームリサイクルは、他のリサイクル原料から分離された高品質のガラスカレットを製造する最も効果的な方法です。

- 流れの純度は、特に処理されるガラスの色に関して決定的に重要です。グリーンガラスは95%まで再生ガラスを使用することができるが、ホワイトガラスやフリントガラスにはより厳しい品質要求があります。この場合、混入のリスクと最終製品の品質への悪影響から、再生ガラスの使用は最大でも60%までしか認められていないです。

- ワイン産業では、ボトルの色はグリーンかアンバーが一般的です。しかし最近では、環境問題や商業的な要求から、より軽量で薄いガラス瓶が求められています。軽いボトルへのシフトは、エネルギー消費、輸送コスト、リサイクル費用の削減を目的としています。さらに、フリントガラスボトルの使用は、ロゼワインや白ワインの色を際立たせ、包装全体の美観を向上させるというニーズに応えるものです。さらに、英国におけるビールの消費量の増加も市場の成長を後押しすると予想されています。

英国のガラス瓶・容器市場概要

英国のガラス瓶・容器市場は、Verallia UK Limited(Verallia Packaging SAS)、Ciner Glass Ltd.、O-I Glass, Inc.、Ardagh Groupなど、様々な大手企業によって細分化されています。この産業で事業を展開する企業は、提携、投資、製品イノベーションなどを通じて事業の拡大に注力しています。

- 2023年5月-アーダグ・ガラス包装(AGP)-英国は、ガラス生産プロセスからの温室効果ガス排出を最小限に抑える、持続可能性の高い効率的な炉の建設を発表。

- 2023年2月-シナー・ガラスがクリスタルパークIIIの240,000m2の土地譲渡契約に調印。この契約により、シナー・ガラスは2021年に開始した購入手続きを完了し、LRMが以前所有していた土地の完全な使用権を取得しました。これにより、ガラスびんメーカーはロンメルに最新鋭の施設を建設するという、さらなる開発における次のステップを構成することができるようになります。ロンメルは、ガラス産業との歴史的なつながりと伝統に加え、戦略的な立地条件からも選ばれました。このような戦略的イニシアチブは、シナーの今後数年間の収益拡大に貢献することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 循環型経済を重視した産業エコシステム分析

- 容器用ガラス-産業情勢

- ロシア・ウクライナ紛争-市場エコシステムへの影響

- 輸出入分析

- 主要促進要因によるコスト分析(部品とエネルギー消費量)

第5章 市場力学

- 市場の促進要因

- 飲料産業におけるガラス包装の需要増加

- ガラス包装が提供するリサイクル性の利点が持続可能性を促進

- 市場課題

- 代替包装オプションが市場成長の課題

- 英国におけるガラスリサイクル重視の高まりとリサイクル率の現状分析

- 英国における容器ガラスの回収とリサイクルの欧州市場との比較分析

- 英国のガラス製造業全体の分析

- 規制の枠組み

- ガラス容器・ボトルの需要-小売業とフードサービス産業

- ガラス製容器包装に対する消費者の動向と嗜好性

- 産業標準-ボトルのサイズと形態

- 英国のガラス生産分析

第6章 市場セグメンテーション

- エンドユーザー産業別

- 飲料

- アルコール飲料

- ビール・サイダー

- ワインスピリッツ

- その他のアルコール飲料

- ノンアルコール

- 炭酸飲料

- 牛乳

- 水、その他ノンアルコール飲料

- 食品

- 化粧品

- その他

- 飲料

- 色別

- 琥珀色

- フリント

- グリーン

第7章 競合情勢

- 企業プロファイル

- Verallia Packaging(Verallia SA)

- Ciner Glass Ltd

- O-I Glass Inc.

- Ardagh Group SA

- Glassworks International

- Gaasch Packaging

- Berlin Packaging

- Vidrala SA

- Beatson Clark

- Stoelzle Flaconnage

第8章 投資分析

第9章 市場の将来

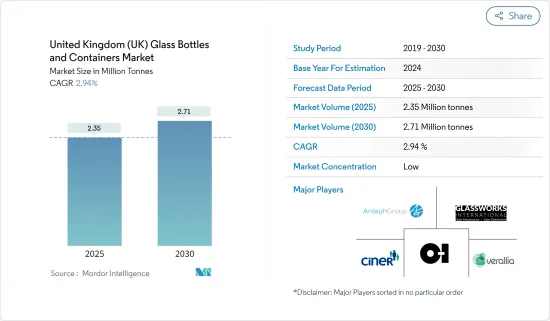

The United Kingdom Glass Bottles and Containers Market size is estimated at 2.35 million tonnes in 2025, and is expected to reach 2.71 million tonnes by 2030, at a CAGR of 2.94% during the forecast period (2025-2030).

Plastic packaging technologies have come a long way in recent years. Still, glass continues to dominate upscale alcoholic and non-alcoholic beverage packaging. Glass is among the most preferred packaging materials for alcoholic beverages, such as spirits. The ability of glass bottles to preserve the aroma and flavor of the product is driving the demand.

Key Highlights

- Increasing customer needs for safe and healthier packaging supports glass packaging growth in different categories. Also, innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end users. Furthermore, factors such as the demand for eco-friendly products and the rising need from the food and beverage market are boosting the market's growth.

- Besides, consumers increasingly prefer beer and wine, and glass packaging manufacturers have adjusted their production. Premium food and beverage brands prefer glass (container glass) over other packaging options, such as plastic, as glass is chemically inert, non-porous, and impermeable.

- The growing adoption of alternative forms of packaging, such as plastic and metal, is among the prominent factors affecting the market's growth over the forecast period. In addition, the increase in recycled plastic (rPET) bottles encouraged by the government also leads to challenging conditions for the adoption of glass packaging.

- According to Argus Media, in May 2022, many companies and brands in the UK's fast-moving consumer goods (FMCG) sector aim to increase recycled content in plastic packaging. The British Plastics Federation (BPF) estimates the current average level of recycled content in the United Kingdom PET bottle market is 15%-20%.

- According to Glass Alliance Europe, production with 39.5 million tonnes were produced two years back. This indicates that the glass manufacturers suffered from energy concerns on top of high competition from third countries. Compared with 2021, 2022 extra EU-27 exports decreased by 4.6% in volume at 4.3 million tonnes but increased by 14.9%. The EU-27's four significant clients in volume are the rest of Europe (59.5%), including the UK (20%), and more countries.

- The growing adoption of alternative forms of packaging, such as paper, plastic, and metal, in different parts of the country is among the prominent factors affecting the market's growth over the forecast period. The advancement in plastic manufacturing technologies and the emergence of highly recyclable plastics, such as bio-plastics, are further expected to drive the growth of plastic packaging, as plastic packaging offers a significant cost advantage compared to glass packaging.

United Kingdom (UK) Glass Bottles and Containers Market Trends

Beverages to be the Largest End-user Industry

- Glass is among the most preferred packaging materials for alcoholic beverages, such as spirits. The ability of glass bottles to preserve the aroma and flavor of the product is driving the demand. Rising consumer demand for safe and healthier packaging helps glass packaging grow in different categories. Also, innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end-users.

- Glass bottles and containers are mainly used in alcohol and nonalcoholic beverages because of their chemical sterility and non-permeability. Also, glass is a significant barrier material and ranks highly for transparency in packaging. It creates an extended shelf-life package because it resists CO2 loss and O2 invasion. The glass bottle frangibility has been improved by new processing and coatings. Modern lightweight and strengthening techniques have improved the strength and consumer-friendliness of glass.

- Furthermore, wine sales and consumption have grown manifolds during the pandemic, and while most of the wines sold are packaged in the standard 750-milliliter format, alternatives such as small format bottles are on the rise. The increase in the consumption of liquor in the region during the pandemic has positively impacted the demand for glass bottles.

- According to the Observatory of Economic Complexity (OEC), in April 2023, United Kingdom exports of Glass Bottles totaled GBP 15.8 million (USD 19.48 million), while imports totaled GBP 40.7 million (USD 50.18 million), resulting in an overall trade deficit of GBP 24.9 million (USD 30.70 million). From April 2022 to April 2023, the United Kingdom's export of Glass Bottles decreased by GBP 931,000 (USD 1,147,965), or 5.57%, from GBP 16.7 million (USD 20.59 million) to GBP 15.8 million (USD 19.48 million), while its imports rose by GBP 10,000,000 (USD 12,330,456.2), or 33.9%, from GBP 30.4 million (USD 37.48 million) to GBP 40.07 million (USD 49.40 million).

- The demand from the alcoholic and nonalcoholic beverage industry primarily drives the increase in the import of glass bottles in the country. This upswing is expected to be witnessed in the forecast period also.

Flint to Hold Major Market Share in Colors

- The utilization of transparent packaging is on the rise for food items such as wine, milk, beer, and juice. This decision is driven by the marketing suggestion that customers prefer to inspect the product before purchase.

- In the United Kingdom, the challenge in producing recycled glass is not in its difficulty but rather the insufficient supply of high-quality recycled clear glass (cullet) necessary for making clear glass bottles with high recycled content. Green glass is the only option if a product requires a glass bottle with a high recycled content. While dark glass is a viable alternative, it may not be suitable for certain products and brands, particularly in the food and beverages industry, where a crystal-clear glass of the highest quality, known as flint or extra-flint, is preferred.

- Frequently, the process of segregating mixed-colored glass at a recycling plant is excessively time-consuming and costly. Consequently, the shattered fragments of mixed glass are repurposed to manufacture glass fiber products, which can serve as an insulation material rather than being transformed into fresh bottles. Multi-stream recycling is the most effective method for producing high-quality glass cullet, which is free from other recyclables.

- The purity of the stream is crucially important, particularly with regard to the color of the glass being processed. Green glass can use up to 95% recycled glass, but there are much stricter quality requirements for white or flint glass. In this case, the maximum level of recycled glass permitted is only 60% due to the risk of contamination and its detrimental effect on the final product's quality.

- In the wine industry, the usual bottle colors are green or amber. However, there has been a recent push for lighter and thinner glass bottles due to environmental concerns and commercial demands. This shift towards lighter bottles aims to reduce energy consumption, transportation costs, and recycling expenses. Furthermore, the use of flint glass bottles responds to the need to highlight the color of rose or white wines and improve the overall aesthetics of the packaging. Furthermore, the increasing consumption of beer in the United Kingdom is also expected to boost the growth of the market.

United Kingdom (UK) Glass Bottles and Containers Market Overview

The United Kingdom Glass Bottles and Containers Market is fragmented with various significant players such as Verallia UK Limited (Verallia Packaging SAS), Ciner Glass Ltd., O-I Glass, Inc., Ardagh Group, and more. Companies operating in the industry are focused on expanding their business through collaborations, investments, product innovations, and more.

- May 2023 - Ardagh Glass Packaging (AGP) - United Kingdom announced the building of a highly sustainable, efficient furnace that is set to minimize greenhouse gas emissions from the glass production process.

- February 2023 - Ciner Glass signed a land transfer agreement for 240,000 m2 at Kristalpark III. With this agreement, Ciner Glass finalized the purchase process that started in 2021 and acquired the full right to use the land previously owned by LRM. This will enable the glass bottle manufacturer to constitute the next step in the further development of building a state-of-the-art facility in Lommel. In addition to its historical connection and heritage with the glass industry, Lommel was chosen for its strategic location. Such strategic initiatives are set to help Ciner in revenue growth in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Eco-system Analysis With an Emphasis on Circular Economy

- 4.4 Container Glass - Industry Landscape

- 4.5 Russia-Ukraine Conflict - Impact on the Market Eco-System

- 4.6 Import and Export Analysis

- 4.7 Cost Analysis With Key Drivers (Components and Energy Consumption)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Glass Packaging in Beverage Industry

- 5.1.2 Recyclability Benefits Offered by Glass Packaging Drive Sustainability

- 5.2 Market Challenges

- 5.2.1 Alternative Packaging Options Challenging the Market Growth

- 5.3 Analysis of the Increasing Emphasis on Glass Recycling and the Current Recyclability Rate in the United Kingdom

- 5.4 Comparative Analysis of Collection and Recycling of Container Glass in the United Kingdom as Opposed to the European Market

- 5.5 Analysis of the Overall Glass Manufacturing Industry in the United Kingdom

- 5.6 Regulatory Framework

- 5.7 Demand for Glass Containers and Bottles - Retail and Foodservice Industries

- 5.8 Consumer Trends and Preference for Glass Packaging

- 5.9 Industry Standards - Bottle Sizes and Shapes

- 5.10 United Kingdom Glass Production Analysis

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Beverages

- 6.1.1.1 Alcoholic

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Other End-user Industries

- 6.1.1 Beverages

- 6.2 By Color

- 6.2.1 Amber

- 6.2.2 Flint

- 6.2.3 Green

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Verallia Packaging (Verallia SA)

- 7.1.2 Ciner Glass Ltd

- 7.1.3 O-I Glass Inc.

- 7.1.4 Ardagh Group SA

- 7.1.5 Glassworks International

- 7.1.6 Gaasch Packaging

- 7.1.7 Berlin Packaging

- 7.1.8 Vidrala SA

- 7.1.9 Beatson Clark

- 7.1.10 Stoelzle Flaconnage