|

市場調査レポート

商品コード

1644463

アジア太平洋地域のガラス瓶および容器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のガラス瓶および容器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

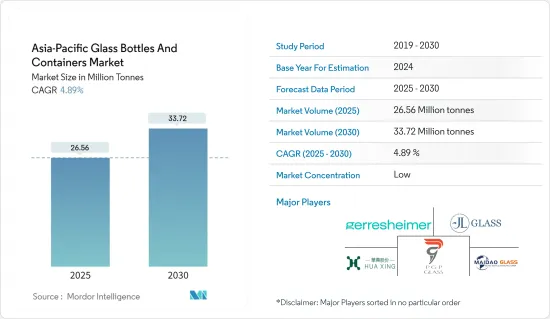

アジア太平洋地域のガラス瓶および容器の市場規模は2025年に2,656万トンと推定・予測され、予測期間(2025-2030年)のCAGRは4.89%で、2030年には3,372万トンに達すると予測されます。

主なハイライト

- アジア太平洋地域では、飲食品、医薬品セクターがガラス容器の需要急増を牽引しています。このような需要の増加は、プラスチック包装の禁止、持続可能性の推進、地域全体で確立されたリサイクルインフラによるところが大きいです。

- 国際貿易センターのデータでは、アジアのガラス容器輸出における中国の優位性が強調されており、2023年には189万8,260トンとなり、インドは35万7,747トンでこれに続く。両国が輸出を拡大するにつれて、最先端の生産技術への投資も活発化しています。このような先進パッケージングは、優れた製品品質だけでなく、工程を合理化し、コストを削減し、他の代替パッケージングに対するガラス容器の競合力を強化する可能性があります。

- インドでは、アルコール飲料への嗜好が高まっており、ガラス容器産業の拡大が見込まれています。特にワイン用のガラス瓶は、日光による腐敗を防ぐという点で好まれています。カナダ農業食糧省は、インドのワイン消費量が2025年までに5,220万リットルに達すると予測しており、ガラス製容器包装の需要がさらに高まるとしています。

- 使い捨てプラスチックの取り締まりにより、ガラスのような代替品への注目が集まっています。日本では、ガラス瓶のリサイクルにかかる財政支出は、他の包装材料に比べて経済的であることが際立っています。日本容器包装リサイクル協会のデータによると、2023年におけるガラス瓶のリサイクルコストは、琥珀色が1kgあたり約8.2円(0.058米ドル)、無色透明が1kgあたり約6円(0.042米ドル)です。このようなコストメリットは、メーカーをガラス包装に向かわせています。

- ガラスの製造はエネルギー集約的な努力であり、原料を溶かすために高温を必要とします。このエネルギー需要は、特にエネルギー価格の高騰や厳しい環境規制に直面している地域では、操業コストを押し上げる可能性があります。さらに、シリカ、ソーダ灰、石灰石のような主要原材料価格の変動は、生産コストをさらに上昇させる可能性があります。

アジア太平洋地域の容器用ガラス市場の動向

飲料が最大の市場シェアを占める

- アジア太平洋地域の容器用ガラス市場では、飲料産業が市場シェアの約60%を占めており、市場の成長を牽引する極めて重要な役割を担っています。

- 消費者は、特に飲料用として、プラスチックよりもガラスを使用することの健康上の利点をますます認識するようになっています。ガラスは毒性がなく、化学物質を製品に溶出させることもなく、特にアルコール飲料では長期間の使用に安全であると考えられています。このような消費者の嗜好の変化は、容器用ガラス市場の成長を促進すると予想されます。

- 中国の包装産業は、経済の拡大と購買力を増した中間層の増加により、急速かつ着実な成長を遂げています。飲料市場の拡大により、特にガラス容器分野での包装需要が高まっています。各飲料カテゴリーにはそれぞれ独自の課題と機会が存在しますが、中国の消費者のライフスタイルに新たな動向が生まれ、ガラス製容器包装の需要が形成されつつあります。

- 中国の主要都市部では、アルコール飲料とノンアルコール飲料の消費量が増加しています。古代にルーツを持つアルコール飲料には、米酒、ブドウ酒、ビール、ウイスキー、各種蒸留酒などがあります。白酒は依然として中国で最も消費されている蒸留酒です。

- HKEXnewsによると、2021年、Nongxiangフレーバー白酒の売上高は約2,860億人民元(404億2,000万米ドル)で、中国の白酒売上高の半分以上を占めています。Nongxiangフレーバー白酒の売上は、2026年までに3,129億人民元(442億2,000万米ドル)に達すると予測されています。

- 韓国の飲酒文化はアルコール消費にとどまらず、伝統的な付随食品にまで広がっています。強烈でスパイシーな風味で知られる韓国料理は、しばしば飲酒を補完します。伝統的な米酒から、ますます人気が高まっている焼酎に至るまで、アルコールは韓国の社会と文化で中心的な役割を果たしています。市場は主に、大量消費向けの焼酎を製造する低価格ブランドによって特徴付けられています。

- ガラス包装は、飲料の保存にいくつかの利点を提供します。持続可能で、無限にリサイクルでき、再利用可能で、詰め替え可能で、合成化学物質を含まず不活性です。これらの特性により、ガラスは飲料を安全に包装するための実行可能な選択肢となっています。

- 日本コカ・コーラは、飲料からプラスチックラベルを取り除き、自動販売機の消費電力を削減するなど、様々な持続可能性への取り組みを実施しています。これは、2030年までに全世界のパッケージの25%をリサイクルし、ガラス瓶を含む再利用可能なパッケージを導入するという同社の世界のコミットメントと一致しています。こうした取り組みが、同地域におけるガラス容器市場の成長に寄与しています。

- 消費者の間で健康とウェルネスに対する意識が高まり、様々な健康効果があるとされる機能性飲料への需要が高まっています。ガラス製容器包装は飲料の栄養状態を保持するための安全で衛生的な選択肢と考えられているため、この動向に合致しており、ガラス製容器市場の成長を支えています。

- Hong Kong Exchanges and Clearing Limitedによると、中国における機能性飲料の小売売上高は2019年に約158億2,000万米ドルに達し、2024年には248億2,000万米ドルに達すると予測されています。

著しい市場成長を占めるインド

- 乳製品の需要増がガラス包装設計の革新を促しています。メーカーは、利便性、耐久性、審美性を向上させたガラス瓶や容器を開発するために研究開発に投資すると思われます。このような技術革新はアジア太平洋地域のガラス包装市場の成長に貢献すると期待されています。

- 持続可能性と環境に優しいパッケージング・ソリューションに重点を置く乳製品業界は、リサイクル可能で何度も再利用できるガラス容器の採用をさらに後押ししています。

- 世界の生乳生産量におけるインドの圧倒的な地位は、この動向をさらに後押ししています。Invest Indiaによると、インドは世界の生乳生産量の25%を占め、世界の生乳生産量をリードしています。インドの生乳生産量は2014-15年から2022-23年の間に58%増加し、2022-23年には2億3,058万トンに達します。この生乳生産の大幅な伸びにより、高品質のパッケージング・ソリューションに対する需要が高まり、高級乳製品にはガラス瓶が好んで選ばれています。

- 清涼飲料メーカーはガラス瓶の使用を積極的に推進しています。2023年3月、コカ・コーラ・インディアのサムズアップは「Toofan Glass Mein Nahin, Glass Se Peete Hain」というテレビキャンペーンを開始し、消費者にリターナブルのガラス瓶から飲料を体験するよう促しました。同社は、ソーダファウンテンやガラス瓶で販売される飲料を含め、2030年までに全世界で飲料の少なくとも25%を再利用可能またはリターナブル容器で販売することを目指しています。

- このイニシアチブは持続可能性を促進するだけでなく、ガラス瓶は他の包装材料よりも飲料の炭酸と風味を維持しやすいことが知られているため、消費者の体験を向上させる。

- ノンアルコール飲料、特にソフトドリンクの成長もガラス包装の市場需要に影響を与えると予想されます。消費者の健康志向の高まりにより、天然飲料やオーガニック飲料の消費が増加しており、これらの飲料は純度と鮮度を保つためにガラス瓶で包装されることが多いです。さらに、クラフトソーダや職人技を駆使した飲料など、ノンアルコール飲料のプレミアム・セグメントでは、品質と高級感を伝えるためにガラス製パッケージを選ぶことが多いです。

- アルコール飲料の輸出増加は、ガラス瓶および容器の需要を牽引しています。ガラス包装は風味と品質を保つ能力があるため、アルコール飲料に好まれます。APEDAによると、2023年度のインドのアルコール飲料輸出額は3億1,600万米ドルに達し、前年度から3,800万米ドル増加しました。

- 国際市場では輸入アルコール飲料の品質や包装に対する要求が厳しいことが多いため、このような輸出の伸びは高級ガラス包装に対する需要の高まりにつながっています。さらに、この地域におけるクラフトビール醸造所や蒸留所の台頭は、特殊なガラス瓶や容器のニッチ市場を生み出し、ガラス包装業界の成長をさらに促進しています。

アジア太平洋地域の容器用ガラス産業の概要

アジア太平洋地域の容器用ガラス市場は細分化されており、複数の大手企業が市場シェアを争っています。これらの企業は、市場での地位を強化するため、戦略的パートナーシップや製品開拓に継続的に投資しています。

市場の主要企業には、多国籍企業や地域メーカーが含まれます。これらの企業は、生産能力の拡大、流通網の強化、革新的なパッケージング・ソリューションの開発に注力し、多様な顧客ニーズに応えています。また、市場でのプレゼンスを強化し、新しい技術や市場セグメントへのアクセスを得るために、M&Aを行う企業もあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 容器用ガラスの輸出入データ

- 容器用ガラス市場のPESTEL分析

- 容器包装用ガラスの業界標準と規制

- 包装用ガラスの原材料分析と材料検討

- 容器包装用ガラスの持続可能性動向

- アジア太平洋地域の容器用ガラス炉と立地

第5章 市場力学

- 市場促進要因

- 持続可能な包装ソリューションへの需要の高まりによるガラス使用の促進

- 製薬業界におけるガラス製包装への嗜好の高まり

- 市場の課題

- 高い製造コストとエネルギーコストが容器用ガラス市場の成長を制限

- 貿易概況-アジア太平洋地域における容器用ガラス産業の輸出入パラダイムの歴史と現状分析

第6章 市場セグメンテーション

- エンドユーザー業界別

- 飲料

- アルコール

- ビール・サイダー

- ワイン・スピリッツ

- ノンアルコール

- 炭酸飲料

- ジュース

- 水

- 乳飲料

- フレーバー飲料

- 食品

- 化粧品

- 医薬品(バイアル・アンプルを除く)

- その他のエンドユーザー業界別

- 飲料

- 国別

- 中国

- インド

- 日本

- タイ

- オーストラリア・ニュージーランド

- 韓国

- ベトナム

第7章 競合情勢

- 企業プロファイル

- Gerresheimer AG

- Guangdong Huaxing Glass Co., LTD

- Maidao Industry Co. Ltd

- JL Glass Co., Ltd

- PGP Glass Private Limited

- KOA GLASS CO., LTD.

- AGI glaspac

- CANPACK GROUP

- Emerge Glass

- JAPAN SEIKO GLASS CO.,LTD.

第8章 補足資料:地域内の主要コンテナーガラス工場への主要加熱炉サプライヤーの分析

第9章 市場の将来展望

The Asia-Pacific Glass Bottles And Containers Market size is estimated at 26.56 million tonnes in 2025, and is expected to reach 33.72 million tonnes by 2030, at a CAGR of 4.89% during the forecast period (2025-2030).

Key Highlights

- In the Asia-Pacific region, the food, beverage, and pharmaceutical sectors are driving a surge in demand for glass containers. This uptick is largely attributed to bans on plastic packaging, a push for sustainability, and a well-established recycling infrastructure throughout the region.

- Data from the International Trade Centre highlights China's dominance in Asia's glass container exports, tallying 1,898,260 tons in 2023, with India trailing at 357,747 tons. As both nations ramp up their export activities, they're poised to channel investments into cutting-edge production technologies. Such advancements promise not only superior product quality but also streamlined processes, potentially slashing costs and bolstering the competitiveness of glass containers against other packaging alternatives.

- In India, the rising appetite for alcoholic beverages is set to propel the glass container industry's expansion. Glass bottles, especially for wine, are favored for their protective qualities against sunlight-induced spoilage. Agriculture and Agri-Food Canada forecasts India's wine consumption to hit 52.2 million liters by 2025, further amplifying the demand for glass packaging.

- With the crackdown on single-use plastics, there's been a notable pivot towards alternatives like glass. In Japan, the financial outlay for recycling glass bottles stands out as more economical compared to other packaging materials. Data from the Japan Containers and Packaging Recycling Association reveals that in 2023, recycling costs for amber and colorless glass bottles were about JPY 8.2 (USD 0.058) and JPY 6 (USD 0.042) per kilogram, respectively. Such cost benefits are nudging manufacturers towards glass packaging.

- Producing glass is an energy-intensive endeavor, demanding elevated temperatures to melt raw materials. This energy requirement can inflate operational costs, particularly in areas grappling with surging energy prices or stringent environmental mandates. Moreover, fluctuations in the prices of key raw materials like silica, soda ash, and limestone can further escalate production expenses.

Asia-Pacific Container Glass Market Trends

Beverage Occupies the Largest Market Share

- The beverage industry's dominance, accounting for approximately 60% of the market share in the Asia-Pacific container glass market, plays a pivotal role in driving the market's growth.

- Consumers are increasingly aware of the health benefits of using glass over plastic, particularly for beverages. Glass is non-toxic, does not leach chemicals into the product, and is considered safer for long-term use, especially in alcoholic beverages. This shift in consumer preference is expected to fuel growth in the container glass market.

- China's packaging industry is experiencing rapid and steady growth, fueled by the country's expanding economy and a growing middle class with increased purchasing power. The beverage market's expansion is driving a heightened demand for packaging, particularly in the glass container segment. While each beverage category presents unique challenges and opportunities, emerging trends in Chinese consumer lifestyles are shaping the demand for glass packaging.

- China's major urban areas have witnessed an increase in the consumption of both alcoholic and non-alcoholic beverages. Alcoholic beverages, with roots in ancient times, include rice wine, grape wine, beer, whiskey, and various spirits. Baijiu remains the most consumed distilled spirit in China.

- According to HKEXnews, in 2021, Nongxiang flavor baijiu generated revenue of approximately CNY 286 billion (USD 40.42 billion), accounting for over half of China's baijiu sales revenue. The revenue from Nongxiang flavor baijiu is projected to reach CNY 312.9 billion (USD 44.22 billion) by 2026.

- Korean drinking culture extends beyond alcohol consumption to include traditional accompanying foods. Korean cuisine, known for its intense and spicy flavors, often complements alcohol consumption. From traditional rice wines to the increasingly popular soju, alcohol plays a central role in Korean society and culture. The market is predominantly characterized by low-priced brands producing soju for mass consumption.

- Glass packaging offers several advantages for beverage storage. It is sustainable, infinitely recyclable, reusable, refillable, and inert, containing no synthetic chemicals. These properties make glass a viable option for packaging beverages safely.

- Coca-Cola Japan has implemented various sustainability initiatives, including removing plastic labels from drinks and reducing power consumption in vending machines. This aligns with the company's global commitment to recycle 25% of packaging worldwide by 2030 and implement reusable packaging, including glass bottles. Such initiatives are contributing to the growth of the glass container market in the region.

- Increasing health and wellness awareness among consumers is driving demand for functional beverages, which are perceived to offer various health benefits. Glass packaging aligns with this trend as it is considered a safe and hygienic option for preserving the nutritional integrity of beverages, thus supporting the growth of the glass containers market.

- According to Hong Kong Exchanges and Clearing Limited, the retail sales of functional beverages in China reached nearly USD 15.82 billion in 2019 and are projected to reach USD 24.82 billion by 2024.

India to Account for Significant Market Growth

- The increasing demand for dairy products is driving innovation in glass packaging design. Manufacturers are likely to invest in research and development to create glass bottles and containers that offer improved convenience, durability, and aesthetic appeal. This innovation is expected to contribute to the growth of the Asia-Pacific glass packaging market.

- The dairy industry's focus on sustainability and eco-friendly packaging solutions further propels the adoption of glass containers, as they are recyclable and can be reused multiple times.

- India's dominant position in global milk production further supports this trend. According to Invest India, the country leads worldwide milk production, contributing 25% of the global output. India's milk production increased by 58% between 2014-15 and 2022-23, reaching 230.58 million tonnes in 2022-23. This significant growth in milk production has led to an increased demand for high-quality packaging solutions, with glass bottles being a preferred choice for premium dairy products.

- Soft drink manufacturers are actively promoting the use of glass bottles. In March 2023, Coca-Cola India's Thumbs Up launched a television campaign, 'Toofan Glass Mein Nahin, Glass Se Peete Hain,' encouraging consumers to experience the beverage from returnable glass bottles. The company aims to sell at least 25% of its beverages globally in reusable or returnable containers by 2030, including drinks sold at soda fountains and in glass bottles.

- This initiative not only promotes sustainability but also enhances the consumer experience, as glass bottles are known to maintain the beverage's carbonation and flavor better than other packaging materials.

- The growth in non-alcoholic beverages, particularly soft drinks, is also expected to impact the market demand for glass packaging. The rising health consciousness among consumers has led to an increase in the consumption of natural and organic beverages, which are often packaged in glass bottles to maintain their purity and freshness. Additionally, the premium segment of non-alcoholic beverages, including craft sodas and artisanal drinks, often opts for glass packaging to convey a sense of quality and luxury.

- Increased exports of alcoholic beverages are driving demand for glass bottles and containers. Glass packaging is preferred for alcoholic beverages due to its ability to preserve flavor and quality. According to APEDA, in the financial year 2023, India's export value of alcoholic beverages reached USD 316 million, an increase of USD 38 million from the previous year.

- This growth in exports has led to a higher demand for premium glass packaging, as international markets often have stringent quality and packaging requirements for imported alcoholic beverages. Furthermore, the rise of craft breweries and distilleries in the region has created a niche market for specialized glass bottles and containers, further driving the growth of the glass packaging industry.

Asia-Pacific Container Glass Industry Overview

The Asia-Pacific container glass market is characterized by fragmented, with several major companies competing for market share. These companies consistently invest in strategic partnerships and product development initiatives to strengthen their positions in the market.

Key players in the market include multinational corporations and regional manufacturers. These companies often focus on expanding their production capacities, enhancing their distribution networks, and developing innovative packaging solutions to meet diverse customer needs. Some firms also engage in mergers and acquisitions to consolidate their market presence and gain access to new technologies or market segments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL Analysis of Container Glass Market

- 4.4 Industry Standard and Regulation for Container Glass Use for Packaging

- 4.5 Raw Material Analysis and Material Consideration for Packaging

- 4.6 Sustainability Trends for Glass Packaging

- 4.7 Container Glass Furnace and Location in Asia- Pacific Region

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Sustainable Packaging Solutions Boosting Glass Use

- 5.1.2 Growing Pharmaceutical Industry Preference for Glass Packaging

- 5.2 Market Challenge

- 5.2.1 High Manufacturing and Energy Costs Limiting Growth in the Container Glass Market

- 5.3 Trade Scenerio - Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in Asia-Pacific

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.2 Non-Alcoholic

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Juices

- 6.1.1.2.3 Water

- 6.1.1.2.4 Dairy Based Drinks

- 6.1.1.2.5 Flavored Drinks

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical (Excluding Vials and Ampoules)

- 6.1.5 Other End-User Vertical

- 6.1.1 Bevarages

- 6.2 By Country

- 6.2.1 China

- 6.2.2 India

- 6.2.3 Japan

- 6.2.4 Thailand

- 6.2.5 Australia and New Zealand

- 6.2.6 South Korea

- 6.2.7 Vietnam

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Gerresheimer AG

- 7.1.2 Guangdong Huaxing Glass Co., LTD

- 7.1.3 Maidao Industry Co. Ltd

- 7.1.4 JL Glass Co., Ltd

- 7.1.5 PGP Glass Private Limited

- 7.1.6 KOA GLASS CO., LTD.

- 7.1.7 AGI glaspac

- 7.1.8 CANPACK GROUP

- 7.1.9 Emerge Glass

- 7.1.10 JAPAN SEIKO GLASS CO.,LTD.