|

市場調査レポート

商品コード

1635452

スペインの容器用ガラス:市場シェア分析、産業動向、成長予測(2025~2030年)Spain Container Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインの容器用ガラス:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

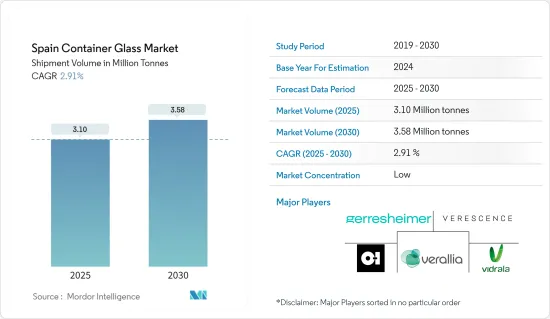

スペインの容器用ガラス市場規模(出荷量ベース)は、予測期間(2025-2030年)のCAGR 2.91%で、2025年の310万トンから2030年には358万トンに成長すると予測されます。

主なハイライト

- 包装食品や飲食品の需要増に牽引され、ソーダ石灰シリカ系ガラスのニーズが、特に多様な食品原料の保存用として急増しています。この動向は、ジャム、ソース、ピクルス、調理済み食品などに顕著に見られ、ガラス容器は保存性だけでなく視覚的な魅力も高めています。

- 同市場は、食品加工分野における高級包装への憧れの高まりに後押しされ、急速に拡大しています。ガラス容器は、製品の品質を際立たせ、棚の存在感を高めることができるため、ますます好まれるようになっています。

- プラスチック汚染に対する意識の高まりと持続可能な代替品を求める声が、ガラス包装へのシフトに拍車をかけています。このシフトは、環境に優しく、安全で、より健康的なパッケージングを求める消費者の要望によってさらに後押しされています。ガラス成形、エンボス加工、装飾仕上げの技術革新は、ガラス包装の魅力をさらに高めています。このような進歩は、ユニークなデザインを容易にするだけでなく、ブランディングの機会を提供し、製品が店頭で注目を集めることを確実にします。

- さらに、環境に優しい製品に対する飲食品セクターの需要の高まりは、特にガラスが100%リサイクル可能で、品質を損なうことなく無限に再利用できることから、市場の成長を後押ししています。

- 国際貿易センターによると、スペインの容器ガラス輸入(HSコード-701090)は、2022年の8億886万1,000米ドルから2023年には10億7,089万米ドルに急増しました。この顕著な輸入の増加は、飲食品、医薬品、化粧品などの分野によって容器ガラスの需要が急増していることを裏付けています。このような消費の高まりは潜在的な市場成長のシグナルであり、メーカーやサプライヤーはそれに応じて事業規模を拡大する必要があります。

- 高級食品ブランドやアルコール飲料・非アルコール飲料の製造業者は、プラスチックのような代替品よりもガラス容器を選ぶ傾向が強まっています。この嗜好は、ガラスの化学的不活性、無孔性、不浸透性に起因しています。このような特性は、製品の味、香り、品質が長期にわたって損なわれないことを保証し、高級品や賞味期限が長いものにとって極めて重要な要素です。

- 容器用ガラスはアルコール飲料に好まれ、その香りと味を保つのに適しています。例えば、ワイン・メーカーはしばしば着色された容器ガラスを選び、品質を損なう可能性のある光線からワインを保護しています。

- スペインの容器用ガラス市場は、ワイン消費量の増加、クラフトビールや高級蒸留酒への評価の高まりによって活況を呈しています。カクテル文化の台頭や、職人技を駆使した高級飲料への動向は、アルコール業界における最高級のガラス製容器包装への需要をさらに高めています。

- しかし、スペインの容器用ガラス市場は、代替製品の台頭という課題に直面しています。パッケージング技術の先進化により、プラスチック、金属、カートンなどの代替品が人気を集めています。その軽量性、コスト効率、デザインの柔軟性が魅力となっています。この傾向は、利便性と持続可能性が最重要視される飲食品業界で特に顕著です。

スペイン容器用ガラス市場の動向

飲料産業が最も高い市場シェアを占める

- ガラス製容器包装市場は、金属製容器包装分野、特にアルコール飲料用の缶と激しく競合しています。しかし、高級品との関連から、容器用ガラス包装は予測期間を通じて市場シェアを維持するものと思われます。コーヒー、ジュース、紅茶、乳飲料、非乳飲料を含む非アルコール飲料分野の成長が見込まれます。

- スペインの活気あるナイトライフは観光客を惹きつけるだけでなく、高級品を好む高級志向の顧客をも惹きつけています。優れた保存性と美的魅力で知られるガラスは、高級飲料のパッケージとして好まれています。ナイトクラブの隆盛に伴い、こうした高級品に特化した高級ガラス容器の需要が高まると思われます。

- 国際ナイトライフ協会の報告によると、2023年にはスペインが世界をリードし、27の一流ナイトクラブを誇っています。米国は、世界のエリート・クラブの5分の1をホストしており、その後塵を拝しています。

- ワイン、ビール、スピリッツなどのボトル入り飲料の主要消費者であるナイトクラブは、需要の急増を目の当たりにしています。接客業の盛況を示すこの増加は、容器ガラス市場における高級ガラス包装のニーズの高まりを裏付けています。

- ガラス容器は、ヨーグルトやクリームからフレーバーミルクやデザートに至るまで、その鮮度保持の特質から高級乳製品の包装に最適な選択肢となっています。乳製品部門が拡大するにつれて、特に高級品や職人気質の生産者のガラス製パッケージに対する需要も拡大すると思われます。

- スペイン飲食品産業連盟(FIAB)のデータは、乳製品セクターの成長を強調している:スペインの乳製品額は2018年の95億6,300万米ドルから2023年には注目すべき168億6,200万米ドルに急増します。

化粧品産業が成長を促進する見込み

- 企業はますます、国連の17の持続可能な開発目標(SDGs)に自社の事業を合わせるようになっています。この取り組みはスペインの化粧品容器用ガラス市場に利益をもたらし、成長を促進する可能性があります。SDGsに取り組むことで、企業は持続可能性と社会的責任への献身を強調することができます。その結果、これらの目標を掲げるスペインの化粧品会社は、消費者の信頼と忠誠心を高め、市場シェア拡大への道を開く可能性があります。

- 環境・社会・ガバナンス(ESG)要素は、投資家やビジネスパートナーが企業を評価する際に注目されています。スペインの化粧品企業は、SDGsと連携することで、持続可能な事業を求める投資家へのアピールを強化することができます。さらに、このような連携は、持続可能性を重視する他の企業とのパートナーシップに道を開き、化粧品容器ガラス市場の革新と成長に拍車をかけるコラボレーションを促進することができます。

- 化粧品の消費量が増加するにつれ、包装材料、特にガラス容器の需要も増加しています。特に香水、スキンケアアイテム、高級化粧品などのプレミアム化粧品は、その美的魅力と保護効果を重視し、ガラス製パッケージを選ぶことが多いです。ガラス容器は、香りの完全性を保ち、汚染を防ぐだけでなく、製品の賞味期限を延ばすことができます。

- Cosmetic Europeによると、スペインの化粧品市場は2018年の75億8,000万米ドルから2023年には112億6,000万米ドルに達すると予測されています。

- 市場の拡大に伴い、特に高級品とハイエンドのセグメントでは、高級パッケージング・ソリューションの需要が高まっています。高級感のある外観、透明性、環境に優しい特性で支持されているガラスは、高品質の化粧品に最適な選択肢です。そのリサイクル性の高さは、持続可能な包装に対する消費者の嗜好の高まりと共鳴しています。さらに、ガラスはデザインに多様性があるため、ブランドはユニークな形状を作ることができ、混雑したマーケットプレースで差別化を図ることができます。

スペインの容器用ガラス産業の概要

スペインの容器用ガラス市場は細分化されており、地域的なプレーヤーと世界のプレーヤーが混在して市場シェアを争っています。この多様な競合情勢には、既存メーカーと新規参入メーカーの両方が含まれ、それぞれが市場での重要なポジションを争っています。

この市場で事業を展開する企業は、製品ラインナップの拡大、市場でのプレゼンス向上、市場内での収益性向上を目指し、戦略的買収を積極的に進めています。さらに、この競合環境で差別化を図るため、技術革新や持続可能な取り組みに注力する企業もあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 容器用ガラスの輸出入データ

- PESTEL分析- スペインの容器用ガラス産業

- 包装用容器ガラスの業界標準と規制

- 包装用ガラスの原材料分析と材料検討

- 容器包装用ガラスの持続可能性動向

- スペインの容器用ガラス炉容量と立地

第5章 市場力学

- 市場促進要因

- 環境に優しい製品に対する需要の高まり

- 飲食品市場の需要急増

- 市場の課題

- 代替製品の利用拡大

- 欧州の容器用ガラス市場におけるスペインの市況分析

- 貿易概況-スペインの容器用ガラス産業における輸出入パラダイムの歴史と現状分析

第6章 市場セグメンテーション

- エンドユーザー業界別

- アルコール(セグメント分析のための定性分析)

- ビールとサイダー

- ワイン・スピリッツ

- その他のアルコール飲料

- ノンアルコール(セグメントのための定性分析)

- 炭酸飲料

- 牛乳

- 水・その他ノンアルコール飲料

- 食品

- 化粧品

- 医薬品(バイアル・アンプルを除く)

- その他エンドユーザー業界別

- アルコール(セグメント分析のための定性分析)

第7章 競合情勢

- 企業プロファイル

- Verallia Group

- BA GLASS GROUP

- O-I Glass, Inc.

- Vidrala, S.A.

- VERESCENCE FRANCE

- Gerresheimer AG

- SAVERGLASS Group

- ALGLASS SA

- Quadpack Industries SA

- Berlin Packaging

第8章 補足取材-スペインの主要容器ガラス工場への主要加熱炉サプライヤーの分析

第9章 市場の将来展望

The Spain Container Glass Market size in terms of shipment volume is expected to grow from 3.10 million tonnes in 2025 to 3.58 million tonnes by 2030, at a CAGR of 2.91% during the forecast period (2025-2030).

Key Highlights

- Driven by the rising demand for packaged food and beverages, the need for soda-lime-silica-based glass has surged, especially for storing diverse food ingredients. This trend is notably seen in items like jams, sauces, pickles, and ready-to-eat meals, where glass containers not only preserve but also enhance visual appeal.

- The market is witnessing rapid expansion, fueled by a growing appetite for premium packaging in the food processing sector. Glass containers are increasingly preferred for their ability to highlight product quality and boost shelf presence.

- Heightened awareness of plastic pollution and a collective push for sustainable alternatives have spurred a shift towards glass packaging. This shift is further bolstered by consumer demand for eco-friendly, safe, and healthier packaging. Innovations in glass shaping, embossing, and decorative finishes have amplified the allure of glass packaging. Such advancements not only facilitate unique designs but also present branding opportunities, ensuring products capture attention on store shelves.

- Furthermore, the food and beverage sector's rising demand for eco-friendly products propels market growth, especially given glass's 100% recyclability and infinite reusability without quality loss.

- According to the International Trade Centre, Spain's container glass imports (HS Code-701090) surged to USD 10,70,890 thousand in 2023, up from USD 8,08,861 thousand in 2022. This notable uptick in imports underscores a burgeoning demand for container glass, likely spurred by sectors like food and beverage, pharmaceuticals, and cosmetics. Such heightened consumption signals potential market growth, prompting manufacturers and suppliers to scale operations accordingly.

- Premium food brands and producers of both alcoholic and non-alcoholic beverages are increasingly gravitating towards glass containers over alternatives like plastic. This preference stems from glass's chemical inertness, non-porosity, and impermeability. Such attributes ensure that a product's taste, aroma, and quality remain intact over time, a crucial factor for high-end items and those with extended shelf lives.

- Container glass is a favored choice for alcoholic beverages, adept at preserving their aroma and taste. For instance, wine manufacturers often opt for tinted container glass, shielding the wine from light exposure that could compromise its quality.

- Spain's container glass market has been buoyed by rising wine consumption and a burgeoning appreciation for craft beers and premium spirits. The cocktail culture's ascent and a trend towards premium, artisanal beverages further amplify the demand for top-tier glass packaging in the alcoholic sector.

- However, the Spain container glass market faces challenges from the rising adoption of substitute products. Thanks to advancements in packaging technology, alternatives such as plastic, metal, and carton materials are gaining traction. Their lighter weight, cost-effectiveness, and design flexibility make them appealing. This trend is especially pronounced in the food and beverage industry, where convenience and sustainability are paramount.

Spain Container Glass Market Trends

Beverage Industry to Hold the Highest Market Share

- The container glass packaging market contends fiercely with the metal packaging segment, particularly in the form of cans used for alcoholic beverages. Yet, due to its association with premium products, container glass packaging is poised to retain its market share throughout the forecast period. Growth is anticipated in the non-alcoholic beverage sector, encompassing coffee, juices, tea, and both dairy and non-dairy drinks.

- Spain's vibrant nightlife not only draws tourists but also an upscale clientele with a penchant for premium products. Glass, celebrated for its superior preservation and aesthetic allure, is the preferred choice for high-end beverage packaging. As the nightclub sector flourishes, the demand for specialized luxury glass containers for these premium offerings is set to rise.

- Spain led the world in 2023, boasting 27 top-rated nightclubs, as reported by the International Nightlife Association. The U.S. trailed, hosting one-fifth of the globe's elite clubs.

- Nightclubs, major consumers of bottled beverages like wine, beer, and spirits, are witnessing a surge in demand. This uptick, indicative of a thriving hospitality sector, underscores the rising need for premium glass packaging in the container glass market.

- Glass containers are the go-to choice for packaging premium dairy items, from yogurt and cream to flavored milk and desserts, thanks to their freshness-preserving qualities. As the dairy sector expands, so too will the demand for glass packaging, especially from high-end and artisanal producers.

- Data from the Spanish Federation of Food and Beverage Industries (FIAB) highlights the dairy sector's growth: Spain's dairy product value surged from USD 9,563 million in 2018 to a notable USD 16,862 million in 2023.

Cosmetic Industry is Expected to Bolster Growth

- Companies are increasingly aligning their operations with the United Nations' 17 Sustainable Development Goals (SDGs). This alignment stands to benefit Spain's cosmetic container glass market, potentially fueling its growth. By committing to the SDGs, companies underscore their dedication to sustainability and social responsibility. As a result, Spanish cosmetic firms that embrace these goals could see a boost in consumer trust and loyalty, paving the way for an expanded market share.

- Environmental, social, and governance (ESG) factors are gaining prominence among investors and business partners when assessing companies. By aligning with the SDGs, Spanish cosmetic firms can enhance their appeal to investors on the lookout for sustainable ventures. Furthermore, this alignment can pave the way for partnerships with other sustainability-driven businesses, fostering collaborations that spur innovation and growth in the cosmetic container glass market.

- As cosmetic consumption rises, so does the demand for packaging materials, notably glass containers. Premium cosmetics, especially perfumes, skincare items, and luxury makeup, often opt for glass packaging, valuing its aesthetic charm and protective benefits. Glass containers not only preserve fragrance integrity and prevent contamination but also extend the product's shelf life.

- According to Cosmetic Europe, the Spanish cosmetic market is projected to reach a value of USD 11.26 billion in 2023, up from USD 7.58 billion in 2018.

- With the market's expansion, particularly in the luxury and high-end segments, the demand for premium packaging solutions is on the rise. Glass, favored for its premium look, transparency, and eco-friendly attributes, is the go-to choice for high-quality cosmetics. Its recyclability resonates with the growing consumer preference for sustainable packaging. Moreover, glass's versatility in design allows brands to craft unique shapes, setting them apart in a crowded marketplace.

Spain Container Glass Industry Overview

The container glass market in Spain is characterized as fragmented, with a mix of regional and global players competing for market share. This diverse competitive landscape includes both established manufacturers and newer entrants, each vying for a significant position in the market.

Companies operating in this market are actively pursuing strategic acquisitions to expand their product offerings, increase their market presence, and improve profitability within the market. Additionally, some firms focus on technological innovations and sustainable practices to differentiate themselves in this competitive environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL ANALYSIS - Container Glass Industry in Spain

- 4.4 Industry Standard and Regulation for Container Glass Use for Packaging

- 4.5 Raw Material Analysis and Material Consideration for Packaging

- 4.6 Sustainability Trends for Glass Packaging

- 4.7 Container Glass Furnace Capacity and Location in Spain

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Eco-friendly Products

- 5.1.2 Surging Demand from the Food and Beverage Market

- 5.2 Market Challenges

- 5.2.1 Growing Usage of Substitute Products

- 5.3 Analysis of the Current Positioning of Spain in the European Container Glass Market

- 5.4 Trade Scenerio - Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in Spain

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.1 Beer and Cider

- 6.1.1.2 Wine and Spirits

- 6.1.1.3 Other Alcoholic Beverages

- 6.1.2 Non-Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.2.1 Carbonated Soft Drinks

- 6.1.2.2 Milk

- 6.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.3 Food

- 6.1.4 Cosmetics

- 6.1.5 Pharmaceutical (Excluding Vials and Ampoules)

- 6.1.6 Other End-user Verticals

- 6.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Verallia Group

- 7.1.2 BA GLASS GROUP

- 7.1.3 O-I Glass, Inc.

- 7.1.4 Vidrala, S.A.

- 7.1.5 VERESCENCE FRANCE

- 7.1.6 Gerresheimer AG

- 7.1.7 SAVERGLASS Group

- 7.1.8 ALGLASS SA

- 7.1.9 Quadpack Industries SA

- 7.1.10 Berlin Packaging