|

市場調査レポート

商品コード

1911436

決済市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 決済市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

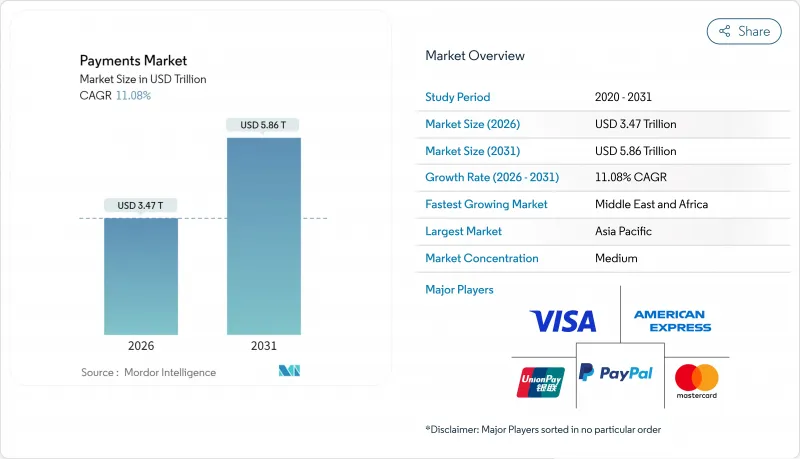

決済市場は、2025年の3兆1,200億米ドルから2026年には3兆4,700億米ドルへ成長し、2026年から2031年にかけてCAGR11.08%で推移し、2031年までに5兆8,600億米ドルに達すると予測されています。

成長の基盤は、消費者のモバイルファースト取引への移行拡大、金融機関の即時決済システムへの迅速な参入、そして取引量と単価の両方を押し上げる越境電子商取引の加速にあります。迅速な決済と統一データ規格に対する継続的な規制支援が口座間決済の普及を促進する一方、非接触型交通プログラムが大都市圏システムにおけるタップ決済カードの利用を刺激しています。カードネットワークが取引量を保護するため人工知能やトークン化に投資する一方で、デジタルウォレットエコシステム、政府運営のリアルタイム決済基盤、新興フィンテック仲介業者が従来のインターチェンジ経済への依存度を低下させていることから、競争の激しさは依然として高い水準にあります。小売分野が全体の取引量を牽引していますが、医療分野と国境を越えた送金分野が最も急速な成長機会を提供しており、専門のプロセッサーやオーケストレーションプラットフォームが参入しています。

世界の決済市場の動向と洞察

モバイルファーストの新興アジアが牽引するEコマース拡大

中国では既にデジタルウォレットがオンライン購入の82%、店舗決済の66%を支えており、インドでは2024年に全取引形態で50%の普及率を達成しました。この普及曲線は欧米の10年分の成長を3年未満に圧縮し、QRコードやウォレット決済がインターチェンジ手数料や旧式カードインフラを迂回することで、加盟店は決済コストを15~20%削減可能となります。スマートフォン普及率とスーパーアプリエコシステムによりウォレットの利用が一般化するにつれて、アジアにおける現金取引の割合は2027年までに14%に低下すると予測されています。アジアのフィンテック企業がQR規格やスーパーアプリのプレイブックを複製することで、湾岸協力会議(GCC)やアフリカの回廊地域にも波及効果が生じ、世界の決済市場の成長軌道を強化しています。ウォレット環境内で収集される詳細な行動データは、従来のカードネットワークでは利用できない融資やロイヤルティにおける収益化の道筋を生み出し、ウォレットの競争をさらに加速させています。

政府による即時決済システムの導入により、北米およびラテンアメリカにおけるA2Aの採用が加速

FedNowは2024年初めまでに米国の400の金融機関が参加し、リアルタイム決済オプションが国内送金の主流となることで構造的な変化をもたらしています。連邦準備制度が目標とする8,000機関の参加により、低額国内取引がカードスキームから分散されます。ブラジルのPIXとインドのUPIはネットワーク効果を実証しており、UPIは年間1,000億件以上の取引を処理し市場浸透率50%を達成。これにより、国が支援する決済基盤が消費者と加盟店の期待値を再定義する能力が確認されました。これらの決済基盤におけるISO 20022規格の互換性により、豊富なデータペイロードが可能となり、企業財務担当者の照合時間を最大40%短縮します。カードネットワークは防衛策を高額取引や越境取引へシフトさせると同時に、紛争管理や分割払いオプションなどの付加価値サービスを拡充しています。

国境を越えた資金移動において、サイバー詐欺の手口がAI/機械学習による防御を凌駕

2023年の世界の不正損失額は4,420億米ドルに達し、攻撃者が遅延や管轄区域の分断を悪用するため、国境を越えたチャネルで最も急激な増加が見られました。Visaは500以上のAIモデルを導入し、データ中心の防御に30億米ドル以上を投資していますが、誤検知が成長著しいアパレルや旅行業者の承認率を損ない続けています。リアルタイム決済は、バッチ決済が従来提供していた調査の機会を排除し、合成身元情報がオンボーディングフィルターを突破した場合の損失を増幅させます。業界が行動ベースの分析へ転換するには、より広範なデータ共有が必要ですが、競合の機密性やプライバシー規制が統一コンソーシアムモデルの構築を妨げています。その結果生じる摩擦は、加盟店による新たな決済基盤の導入を遅らせ、消費者の信頼を損ない、世界の決済市場拡大の一部にブレーキをかけています。

セグメント分析

2025年時点で、POSカード取引は世界決済市場の41.43%を占めております。これは数十年にわたるEMVインフラと世界のブランドの信頼に支えられた結果です。この基盤があるにもかかわらず、QRコードや口座直接決済による受入コスト削減により、電子財布と口座間送金の流れは年率17.31%で増加しております。アジアの加盟店は、消費者をウォレットへ誘導することで手数料を最大2%削減可能であり、この構造的変化を後押ししています。これに対しカードネットワークは、ウォレットエコシステム内に自社決済基盤を組み込むため、ネットワークトークンや分割払いAPIを推進。決済形態が変化しても取引件数を維持しようとしています。

世界の決済市場では、消費総額の増加に伴いカード取引量は絶対値で増加し続ける一方、相対的なウォレットシェアの伸びがより速くなります。ISO 20022の豊富なデータメッセージは法人カードの照合を強化しますが、同時に同じメタデータを持つ競争力のあるA2A(口座間決済)代替手段も可能にします。顧客データ獲得を目指すEC大手企業にとって、共同ブランドカードの発行は戦略的なヘッジ手段であり、即時的なカニバリゼーション(相互食い)ではなく共存を示唆しています。

2025年時点で物理POS端末の取扱高シェアは72.20%を占めましたが、EC・モバイルコマースはCAGR(年率)16.11%で成長を続け、その差は年々縮まっています。このため加盟店は、オンラインと店頭決済を単一APIで統合する決済オーケストレーションへの投資を加速し、ベンダー側の複雑性を低減しています。デジタルウォレットは「ワンクリック決済」とスマートフォンNFCの普及により、2025年のオンライン支出の53%を占めました。店頭での現金利用率は10年間で44%から15%に低下し、実店舗小売業者は現金管理業務の人員を再配置できるようになりました。

世界の決済市場では、飲食店やファストフードチェーンがQRコード注文を導入し、顧客が店内にいる間も決済をEC基盤経由で処理しています。ウェアラブル端末はカード提示の概念を腕時計や指輪に拡張し、エッジでのトークン化の必要性を高めています。決済サービスプロバイダーは、承認・再試行・コストデータを詳細に可視化するオーケストレーションダッシュボードで差別化を図り、CFOが決済を単なる合否判定のユーティリティではなく、管理可能な損益計算書の項目として扱えるようにしています。

本決済業界市場レポートは、決済手段(POS、オンライン販売)、エンドユーザー業界(小売、医療など)、インタラクションチャネル(POS、Eコマース/Mコマース)、取引タイプ(個人間(P2P)、消費者から企業(C2B)など)、地域別に分類されています。市場予測は金額(米ドル)ベースで提供されます。

地域別分析

アジア太平洋地域は、中国の電子ウォレット二強体制とインドのUPIが年間取引量1,000億件を突破したことに牽引され、2025年に37.62%の収益で世界決済市場をリードしました。東南アジア全域では、加盟店がスキーム間で相互運用可能な動的QR規格を採用したことで、電子ウォレットの普及が加速しています。地域各国政府は小売用途向け中央銀行デジタル通貨(CBDC)の試験運用を継続しており、これによりカード決済を上回る口座ベースの資金流動がさらに促進される可能性があります。

中東・アフリカ地域は2031年までに15.12%という最速のCAGRを達成する見込みです。モバイルマネー事業者が代理店ネットワークと簡素化された本人確認(KYC)を通じて現金依存度の高い人口層を転換しているためです。汎アフリカ決済システム(PAPS)は現地通貨によるアフリカ域内即時決済を実現し、中小企業貿易の構造的後押しとなります。湾岸諸国の規制当局はオープンバンキング義務化を推進し、デジタルディルハムの導入を検討しており、これにより世界の決済事業者が地域拠点の設立を進めています。

北米ではクレジットカードの平均利用額が高い水準を維持していますが、FedNowのリアルタイム決済基盤が、公共料金の支払いやギグエコノミーの報酬支払いに新たな国内経路を提供しています。欧州では欧州決済イニシアチブ(EPI)のWeroウォレットを通じたコスト削減と主権確保が優先され、交通ネットワークでは非接触型チケットがカード利用量増加に貢献しています。ラテンアメリカではブラジルのPIXがベンチマークとなり、コロンビアやペルーなどの近隣国が即時決済プログラムを加速。CBDCパイロットでは金融包摂目標に向けオフラインウォレットが模索されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- モバイルファーストの新興アジア市場が牽引する電子商取引の拡大

- 政府による即時決済インフラ(例:FedNow、UPI、PIX)が北米・ラテンアメリカにおけるA2A決済の普及を加速

- 急増する越境B2C送金が中東・北アフリカ(MENA)地域及びアジア太平洋(APAC)回廊におけるデジタルウォレット普及を促進

- 非接触型交通・料金システムが欧州及び北欧におけるタップ決済カード利用を促進

- オセアニア地域における主要小売業者によるBNPL(後払い決済)導入が購入単価と購入頻度を向上

- 先進市場におけるリッチデータ法人決済を実現するISO 20022移行

- 市場抑制要因

- 国境を越えた資金移動において、サイバー詐欺の手口がAI/機械学習による防御策を上回る高度化を遂げております

- EUおよびインドにおけるインターチェンジ手数料とMDR上限が発行体マージンを圧迫

- レガシーコアバンキングシステムの柔軟性の欠如がアフリカにおけるリアルタイム決済を遅延させている

- カリブ海地域の農村経済における現金依存度の高い状況

- バリューチェーン分析

- 規制の見通し

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 持続可能性とグリーン決済イニシアチブ

- 世界決済業界に関連する主要な人口動向とパターンの分析(対象範囲:人口、インターネット普及率、銀行利用率/非銀行利用人口、年齢層・所得など)

- 主要な事例研究と使用事例の分析

- 市場に対するマクロ経済動向の評価

第5章 市場規模と成長予測

- お支払い方法別

- 販売時点情報管理(POS)

- カード(デビットカード、クレジットカード、プリペイドカード)

- デジタルウォレット(Apple Pay、Google Pay、Interac Flash)

- 現金

- その他のPOS(ギフトカード、QRコード、ウェアラブル端末)

- オンライン

- カード(非対面取引)

- デジタルウォレットおよび口座間送金(Interac e-Transfer、PayPal)

- その他のオンライン決済(代金引換、後払い、銀行振込)

- 販売時点情報管理(POS)

- インタラクションチャネル別

- 販売時点情報管理(POS)

- 電子商取引/モバイルコマース

- 取引タイプ別

- 個人間取引(P2P)

- 消費者から企業へ(C2B)

- 企業間取引(B2B)

- 送金・クロスボーダー

- エンドユーザー業界別

- 小売り

- エンターテインメント・デジタルコンテンツ

- ヘルスケア

- ホスピタリティ&トラベル

- 政府・公益事業

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- 北欧諸国

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Visa Inc.

- Mastercard Incorporated

- China UnionPay Co., Ltd.

- Ant Group Co., Ltd.(Alipay)

- PayPal Holdings, Inc.

- Apple Inc.(Apple Pay)

- Google LLC(Google Pay)

- Amazon.com, Inc.(Amazon Pay)

- American Express Company

- Adyen N.V.

- Stripe, Inc.

- Block, Inc.(Square & Afterpay)

- Worldline SA

- Fidelity National Information Services, Inc.(FIS)

- Fiserv, Inc.

- Global Payments Inc.

- Klarna Bank AB

- Razorpay Software Pvt. Ltd.

- PayU Payments Pvt. Ltd.

- Revolut Ltd.