|

市場調査レポート

商品コード

1911331

共有オフィススペース:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Shared Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 共有オフィススペース:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

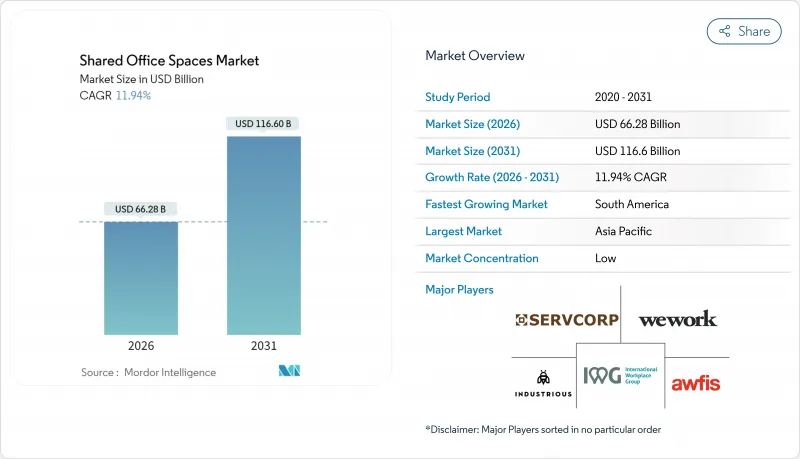

共有オフィススペース市場は、2025年の592億米ドルから2026年には662億8,000万米ドルへ成長し、2026~2031年にかけてCAGR11.94%で推移し、2031年には1,166億米ドルに達すると予測されています。

ハイブリッドワークの企業導入加速、資産軽量モデルへの投資家の関心、地方都市への着実な拡大がこの成長を後押ししています。事業者側は、リース債務を抑制しつつネットワーク範囲を拡大する収益分配型パートナーシップへ軸足を移しつつあります。ウェルネス認証取得やデータ駆動型スペースへの技術投資は顧客の定着率を高めていますが、既存都心部の供給過剰が利益率を圧迫する状況も続いています。アジア太平洋が成長を牽引する一方、南米では新規参入者が初めてのフレキシブルワークスペース利用者を取り込むための急成長の余地が最も大きい状況です。

世界の共有オフィススペース市場の動向と洞察

大企業から中小企業まで、ハイブリッドフレキシブル勤務形態の急速な普及

ハイブリッドとフレキシブルな勤務形態が、大企業から中小企業に至るまで急速に普及しています。CBREの調査によれば、回答企業の92%以上がハイブリッド勤務を導入しており、そのうち3分の2は従業員が週に最低3日は出社すると予測しています。この変化により、長期リース契約は潜在的な負債となり、柔軟な契約条件が戦略的要件となっています。企業は共有オフィススペースに注力しており、変動する出勤状況に応じて座席数を調整できるほか、未使用スペースに関連するコストを削減できます。この仕組みはコスト削減につながるだけでなく、従業員が勤務地の柔軟性をますます重視する中、人材の獲得にも寄与しています。複数の都市で最高水準のセキュリティと一貫した品質を保証できる運営会社は、需要の急増を目の当たりにしています。

新興都市・地方都市への世界のコワーキング事業者の進出

世界のコワーキング事業者は、高まる需要に対応するため新興都市や地方都市への進出を加速しています。2024年にはIWGが867拠点を主に提携により開設し、収益を33億ポンド(41億米ドル)に拡大しました。資産軽量型取引に注力することで、同社は賃貸契約よりも内装工事により多くの資本を配分しています。このアプローチにより、投資資本利益率(ROIC)が向上し、これまでプレミアムコワーキングスペースが不足していた郊外や地方都市への成長を支えています。分散型ロケーションにより、IWGはリモートファーストチームの通勤時間を短縮し、従来型都心集中型モデルからハブアンドスポーク型ネットワークへと移行しています。この戦略は、事業者が都心部の潜在的な空室リスクから保護されるだけでなく、地元中小企業の未充足ニーズにも対応しています。

高い運営費と内装費が事業者の収益性を低下

フレキシブルワークスペース市場において、高い運営コストと内装コストが事業者の収益性に深刻な影響を及ぼしています。2024年第2四半期にはWeWorkの稼働率が67%に低下し、固定費が売上高を上回ったことで、同社の支払能力に対する懸念が高まりました。同社の高級内装、企業向けITインフラ、最高水準のサービスは多額の設備投資を必要とします。これらのコストは、特に空席が発生した場合に重くのしかかります。運営会社はこうした資本負担を軽減するため、地主に協力を求めるケースが増加していますが、小規模プロバイダは近代的な改装資金の調達に苦戦しています。この課題は市場からの撤退を加速させ、さらなる産業再編を促進する可能性があります。

セグメント分析

2025年時点で、コワーキングスペースは共有オフィス市場全体の59.12%を占めました。その成功要因は、即利用可能な環境、コミュニティプログラム、パイロットチームや新規市場参入時のコスト効率性にあります。企業は、プライバシーと協働機会のバランスを取るため、コワーキングハブ内の専用スイートを好みます。サービスオフィスやエグゼクティブスイートは、完全装備のプライベートスペースを固定条件で必要とする企業の間で、依然として需要があります。

ハイブリッド型とバーチャル型ソリューションは、2026~2031年にかけてCAGR12.75%で最も急速に成長するセグメントを形成します。これらはクラウドベースデスク予約、分散型メンバーシップ、オンデマンド会議クレジットを融合し、広範なハイブリッドワークプロトコルを反映しています。WeWorkがVast Coworking Groupと提携し、賃貸契約を結ばずに75の郊外拠点を導入した事例は、運営事業者がネットワーク化されたサービス提供へ移行していることを示しています。これらのモデルにより、企業はプロジェクトの進捗に応じて物理的な存在感を柔軟に調整でき、共有オフィススペース市場の価値提案を強化しています。

地域別分析

2025年、アジア太平洋は急速な都市化と政府支援のイノベーションハブを背景に、世界収益の37.10%を占めました。インドのコワーキングスペース(SmartworksやIndiQubeなどが主導)は、特に第2級都市への拡大に伴い、ほぼ満室状態の稼働率を記録しました。中国では、共有オフィスはスマートシティ計画の一環として位置付けられています。東南アジアでは観光客やデジタルノマドの増加が追い風となり、地域の運営会社はネットワーク拡大戦略の一環として、文化に即したコミュニティイベントを企画しています。

北米は規模では第2位ながら、状況は複雑です。都心部では空室率上昇により賃料が低下しており、運営会社は賃料維持のため設備の充実を図っています。一方、郊外は好調で、米国のフレキシブルワークスペースの45%が現在、中心業務地区(CBD)外に位置し、通勤時間の短縮ニーズに応えています。企業顧客が郊外スペースをサテライトオフィスとして活用する傾向が強まり、従来は住宅地だった地域でのネットワーク拡大が進んでいます。

南米は最も急速に成長しており、2031年までにCAGR13.28%が見込まれています。ブラジルがこの成長を牽引していますが、コロンビアやチリの二次市場でも、ラテンアメリカに初めて進出する多国籍企業からの関心が高まっています。通貨変動リスクは存在しますが、オーナー側は管理契約を通じて運営会社と提携し、参入リスクを軽減しています。欧州では、成長は着実ながら緩やかなペースです。モビリティの枠組みや越境GDPRへの準拠が成長を支えており、特にリモートワークビザに関する施策が安定した首都圏で顕著です。

その他の特典

- エクセル形態の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 大企業から中小企業に至るまで、ハイブリッド型と柔軟な勤務形態の急速な普及

- 世界のコワーキング事業者の新興都市・地方都市への進出

- スタートアップ企業、フリーランス、デジタルノマドからの需要増加

- 回復力のある資産クラスとしての共有オフィスポートフォリオに対する投資家の関心

- テナントのウェルネス認証取得済み、技術導入済み、コミュニティ主導型スペースへの選好の高まり

- 市場抑制要因

- 高い運営コストと内装費用が事業者の収益性を低下させています

- 成熟市場における供給過剰リスクとそれに伴う価格圧力

- 中小・スタートアップ企業における稼働率安定性に影響を与える経済変動性

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者と資産所有者-主要な定量・定性的洞察

- ワークスペース設計技術コンサルタント-主要な定量・定性的洞察

- モジュール型家具とスマートオフィスソリューション提供企業-主要な定量・定性的洞察

- 産業における政府規制と施策

- シェアオフィス不動産市場における技術革新

- 主要オフィス不動産業指標に関する洞察(供給量、賃料、価格、稼働率/空室率(%))

- リモートワークがスペース需要に与える影響

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額:米ドル)

- タイプ別

- コワーキングスペース

- サービスオフィス/エグゼクティブスイート

- その他(ハイブリッド、バーチャルオフィス)

- セクタ別

- 情報技術(ITとITES)

- BFSI(銀行、金融サービス、保険)

- ビジネスコンサルティングと専門サービス

- その他のサービス(小売、ライフサイエンス、エネルギー、法務サービス)

- 最終用途別

- フリーランス

- 企業

- スタートアップとその他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- その他の南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- インドネシア

- その他のアジア太平洋

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 企業プロファイル

- IWG plc(Regus, Spaces)

- WeWork Inc.

- Industrious

- Servcorp Ltd.

- Awfis Space Solutions

- Smartworks

- Ucommune International

- JustCo

- Convene

- Knotel

- Impact Hub

- Office Evolution

- Serendipity Labs

- Expansive(前Novel Coworking)

- CommonGrounds Workplace

- The Executive Centre

- Bizspace

- Workbar

- WorkSuites

- Office Partners 360