|

市場調査レポート

商品コード

1911781

日本の乳製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Japan Dairy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の乳製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 241 Pages

納期: 2~3営業日

|

概要

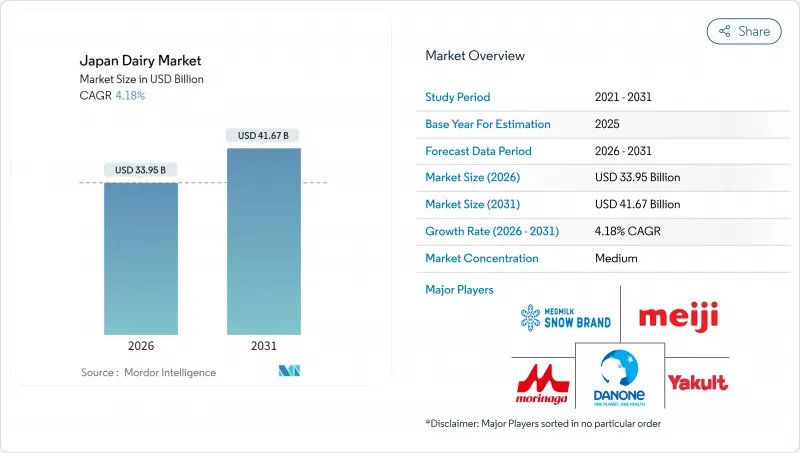

日本の乳製品市場は、2025年に325億9,000万米ドルと評価され、2026年の339億5,000万米ドルから2031年までに416億7,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは4.18%と見込まれています。

構造的な労働力不足、飼料コストの上昇、プレミアム製品のポジショニング、機能性食品の進歩が需要動向を形成しています。健康意識の高まりと予防栄養への注目が、低脂肪、プロバイオティクス、強化、乳糖不使用の乳製品の消費を促進しており、ヨーグルトと機能性飲料がこの成長を牽引しています。ヨーグルトのプロバイオティクス効果と牛乳の常温保存可能フォーマットが、家庭での採用拡大を推進しています。一方、チーズや乳製品デザートは、贅沢な味わいが魅力として人気を集めています。小売業者は都市部の通勤客向けに冷蔵の便利な形態に注力する一方、地方の消費者は常温保存可能なUHT牛乳を選ぶ傾向が強まっています。北海道では、農場の自動化により生産性が向上し、労働力不足が部分的に解消されています。同時に、精密発酵技術やビフィズス菌株への投資が進み、特に機能性表示食品制度のもとで、日本が機能性乳製品イノベーションのリーダーとしての地位を確立しつつあります。

日本の乳製品市場の動向と洞察

プレミアムチーズとヨーグルトの需要拡大

日本ではチーズ消費が着実に増加しており、特にナチュラルチーズはプロセスチーズを上回る成長率を示しています。都市化の進展と西洋料理の日本食への融合により、チーズはニッチな輸入品から広く受け入れられる調理素材・スナックへと変貌を遂げました。一方、ヨーグルトはさらに顕著な成長軌道をたどっています。免疫機能や消化器の健康促進に焦点を当てたプロバイオティクス配合製品は、朝食の習慣や食後の摂取習慣に欠かせない存在となりました。プレミアム化の動向も勢いを増しており、消費者は牧草飼育で生産履歴が追跡可能な乳製品に対して、より高い価格を支払う意思を示しています。多国籍企業はこの機会を捉え、原産地ストーリーの強調や持続可能性認証の取得を通じて、こうした高まる嗜好に応えています。この変化は小売品揃えを大きく変容させています。コンビニエンスストアでは、冷蔵ケースのスペースを職人の手作りチーズや輸入チーズに割り当てる傾向が強まっており、ヨーグルト製品ラインも、飲むヨーグルト、スプーンで食べるタイプ、冷凍デザートとのハイブリッド商品など、多様な選択肢へと拡大しています。

健康志向の高まりによる機能性乳製品への移行

プロバイオティクス、ビタミン、または生物活性ペプチドを強化した機能性乳製品は、予防的な健康ソリューションを求める消費者の関心を集めています。キリンの乳酸菌株「LC-Plasma」は形質細胞様樹状細胞の活性化を促進します。日本の規制枠組みはこうした進展を支援しています。特定保健用食品制度に比べ、科学的根拠に基づく健康効果の自己認証を可能とする「機能性表示食品」制度により、承認プロセスが迅速化されています。この好環境により、製薬会社や栄養補助食品企業が乳製品開発に参画し、業界の境界が曖昧になる中、研究開発が促進されています。高齢化が進む日本では、骨の健康、免疫力、腸内環境の重要性が高まっており、プロバイオティクスヨーグルトや強化乳製品が日常的な健康食品として需要を拡大しています。消費者庁の調査によると、2024年3月時点で、日本の消費者の15.5%が「特定保健用食品(FOSHU)」として認定された健康食品を試したことがあるとのことです。都市部のプロフェッショナルや若い消費者は、忙しいライフスタイルに合致し、代謝改善や消化器健康といった科学的に証明された効果を提供する、単回用飲用ヨーグルトなどの便利な選択肢を好んでいます。

酪農家の高齢化

日本の酪農従事者は急速に高齢化が進み、現在70%以上が65歳以上となっております。この人口動態の動向は生産能力の低下と経営リスクの増大を招いております。多くの生産者は、特に配合飼料の価格上昇や農産物乳価の低迷に直面し、赤字経営を余儀なくされ、市場からの撤退を検討しております。日本酪農協会のデータによりますと、国内の生乳生産量は2022年の753万トンから2023年には732万トンへと減少しました。2024年6月には政府が外国人労働政策を改定し、技能実習生から特定技能労働者への移行を目的とした3年間の育成プログラムを導入しました。本プログラムは畜産分野を明示的に対象としておりますが、実施は2027年まで延期され、年間受け入れ数は限定的と見込まれております。北海道農業公社の5年リース購入制度や全楽アカデミーの3年研修プログラムといった後継者育成制度により、1982年以降約400の新規酪農経営が支援されてまいりました。しかしながら、これらの取り組みは年間引退農家のごく一部に対応するに過ぎません。人口動態上の課題により経営統合が進み、畜群規模は徐々に拡大し、法人による引退農場の買収も増加しています。こうした努力にもかかわらず、統合のペースは引退のペースに追いついておらず、輸入や生産性向上では部分的にしか緩和できない構造的な供給不足が生じています。

セグメント分析

2025年、ヨーグルトは日本の乳製品市場の36.08%を占め、朝食の定番、人気のスナック、健康志向製品としての地位を強化しました。一方、牛乳は乳製品の中で最も高い成長率が見込まれており、2031年までの予測CAGRは4.72%です。プロバイオティクスの進歩がヨーグルトの主導的地位を推進しています:キリンのLC-Plasma菌株、明治のR-1シリーズ、森永のビフィズス菌配合製品は、ヨーグルトを基本的な商品から予防医療製品へと高めました。メーカー各社は「特定保健用食品」の認定も取得しており、パッケージ上で免疫サポート効果を謳うことが可能となりました。飲用タイプのヨーグルトは外出先での消費者に支持され、一方、スプーンで食べるタイプは朝食や食後の摂取に好まれています。牛乳の成長を支えているのは、超高温殺菌処理(UHT)技術です。これにより保存期間が150日に延長され、常温流通が可能となりました。この技術革新は、特に地方や単身世帯において、コールドチェーンコストの削減と入手容易性の向上を実現しています。コーヒー、抹茶、ストロベリーなどのフレーバーミルクは若年層に人気を集めており、UHT牛乳も成長を続けています。

チーズは第3の規模を誇るセグメントであり、ナチュラルチーズが著しい成長を見せております。この拡大は、西洋料理への採用とプレミアム製品への志向変化が牽引しております。消費者は料理やシャルキュトリーボード用にチェダー、パルメザン、職人の手による品種をますます選択しております。生クリーム、調理用クリーム、ホイップクリームを含むクリーム類は、外食産業と家庭用ベーキングの両方のニーズに応え、需要は祝祭期にピークを迎えます。アイスクリーム、チーズケーキ、フローズンデザートなどの乳製品デザートは、ご褒美カテゴリーとして成長しています。注目すべきフレーバーの革新としては、森永製菓の「ピノ抹茶」や明治製菓のコラボレーションデザートなどが挙げられます。ニッチカテゴリーである発酵乳飲料は、酸味のある発酵風味とプロバイオティクスの効能を求める消費者層を惹きつけております。このセグメンテーションは二極化した市場構造を浮き彫りにしており、ヨーグルトと牛乳が販売数量を牽引する一方、チーズとデザートが利益率を押し上げております。このため、加工メーカー各社は収益性と採算性の両方を最適化すべく、戦略的に製品ポートフォリオを管理しております。

日本乳製品市場レポートは、製品タイプ別(バター、チーズ、クリーム、乳製デザート、牛乳、ヨーグルト、サワーミルク飲料)および流通チャネル別(外食産業向け、小売向け)に分類されています。市場予測は金額(米ドル)および数量(トン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- プレミアムチーズおよびヨーグルトに対する需要の増加

- 健康志向の高まりによる機能性乳製品への移行

- 高齢化社会における乳製品の栄養的利点への認識の高まり

- 乳製品加工技術の進歩により、保存期間と品揃えが向上

- 強力な国内乳製品ブランドと幅広い製品革新

- 北海道におけるロボット搾乳の導入

- 市場抑制要因

- 酪農家の高齢化

- Z世代の植物性食品への移行

- 日本における放牧地の供給不足

- 乳糖不耐症や乳製品アレルギーに関する消費者の懸念

- 消費者行動分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額と数量)

- 製品タイプ

- バター

- 有塩バター

- 無塩バター

- チーズ

- ナチュラルチーズ

- チェダー

- コテージ

- リコッタ

- パルメザンチーズ

- その他

- プロセスチーズ

- ナチュラルチーズ

- クリーム

- 生クリーム

- クッキングクリーム

- ホイップクリーム

- その他(クロッテッドクリーム、サワークリーム)

- 乳製品デザート

- アイスクリーム

- チーズケーキ

- 冷凍デザート

- その他(プリン・デザート類、トリフル、フール)

- 牛乳

- 加糖練乳

- フレーバーミルク

- 生乳

- UHTミルク(超高温殺菌乳)

- 粉ミルク

- ヨーグルト

- ドリンカブル

- スプーナブル

- サワーミルク飲料

- バター

- 流通チャネル

- オントレード

- オフトレード

- コンビニエンスストア

- 専門店

- スーパーマーケットおよびハイパーマーケット

- オンライン小売

- その他(倉庫型会員制店、ガソリンスタンドなど)

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Bel Japon KK

- Danone SA

- Megmilk Snow Brand Co. Ltd

- Meiji Dairy Corp.

- Morinaga Milk Industry Co. Ltd

- NH Foods Ltd

- Rokko Butter Co. Ltd

- Takanashi Dairy Co. Ltd

- Yakult Honsha Co. Ltd

- Yotsuba Milk Products Co. Ltd

- Koiwai Dairy Products Co. Ltd

- Arla Foods Japan K.K.

- Fonterra Japan Ltd

- Savencia Fromage and Dairy Japan

- Kraft Heinz Japan Co. Ltd

- Asahi Group Foods Ltd

- Ezaki Glico Co. Ltd

- Kyodo Milk Industry Co. Ltd

- Lacto Japan Co. Ltd

- Hokkaido Dairy Co-op