欧州および中東・アフリカの段ボール包装:市場シェア分析、産業動向、成長予測(2025~2030年)

EMEA Corrugated Board Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1631578

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

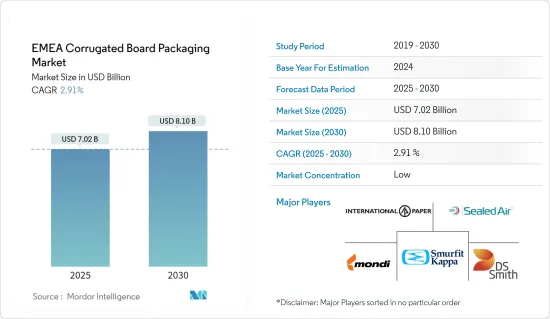

欧州および中東・アフリカの段ボール包装の市場規模は2025年に70億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.91%で、2030年には81億米ドルに達すると予測されます。

段ボール包装は、さまざまな製品を保護、保存、輸送するための多用途でコスト効率の高い方法です。軽量、生分解性、リサイクル性などの特性により、包装業界では不可欠な要素となっています。

主なハイライト

- 生鮮食品・飲食品、家庭・個人向け製品、物流用途、電子製品、持続可能な包装に対する消費者の意識の高まり、eコマース産業の成長といった要因によって、欧州および中東・アフリカの段ボール箱需要は予測期間中に増加すると予想されます。

- eコマース業界は近年、重要なプレーヤーとして台頭してきました。アマゾンのような著名なeコマース企業は、個々の商品をプラスチック包装に頼る一方で、主要な包装として段ボール箱を使用しています。段ボールは汎用性が高いです。そのため、箱以外にもさまざまな形をとることができ、持続可能性の問題から、徐々にフレキシブルなプラスチック袋に取って代わりつつあります。さらに、段ボールはいくつかの印刷技術にとって完璧なベースです。

- 段ボールの使用量では、加工食品分野が最大のシェアを占めています。このセグメントは、欧州および中東・アフリカ内外で消費される食品を包装し、保管し、様々な場所に輸送するという大規模な前提条件により、市場全体をリードしています。また、使い捨てプラスチックの禁止に関する厳しい法律が施行されたことにより、環境に優しい包装材料、特に紙製包装ソリューションの必要性が高まっています。

- ドイツは、段ボール箱の著名な欧州市場のひとつです。製薬、自動車、食品、電子機器などの主要産業が、段ボール箱の高い需要を生み出しています。例えば、ドイツ連邦統計局によると、ドイツにおける段ボール紙・板紙および紙・段ボール製容器の製造による収益は、2023年までに約240億3,000万米ドルに達しました。

- 原材料価格の変動は段ボール製品の製造コストに影響し、段ボール箱の硬度や強度を低下させる。また、段ボール梱包は耐火性も低いです。そのため、段ボール素材の強度が低く、バリア性が低いことが市場の成長を妨げています。

欧州および中東・アフリカの段ボール包装市場の動向

加工食品セグメントが大きな市場シェアを占める見込み

- 欧州および中東・アフリカでは多忙なライフスタイルのため、簡便食品のニーズが高まると予想されます。加工食品は短時間で調理できるため、消費者を惹きつけています。人口の増加により、便利で健康的な加工食品へのニーズが高まると予想されます。加えて、環境に優しい製品の実践に関するユーザーの認識の高まりが、同地域における段ボール包装の需要を促進すると予想されます。

- 環境に優しい包装材料を刺激する政府の動きは、段ボール包装を強化する段ボール業界のイニシアチブである段ボール包装同盟の努力と相まって、この市場の成長にさらなる刺激を与えています。

- Statistisches Bundesamtによると、ドイツのコンビニエンス食品製造事業は2022年に63億5,000万米ドルの収益を上げ、2023年には63億5,000万米ドルに増加しました。コンビニエンス・フード業界は、製品の保護と安全な輸送を保証する包装オプションに大きく依存しています。ドイツのコンビニエンス食品製造業界が開発されるにつれて、こうしたニーズを満たす段ボール包装の需要が高まると思われます。

- 使い捨てプラスチックを禁止する厳しい法律により、環境に優しい包装材料、特に紙ベースのソリューションへの需要が高まっています。この地域ではeコマース・プラットフォームの人気が高まっており、市場の需要をさらに押し上げています。eコマースは小売の風景を大きく変えました。中東、特に湾岸地域におけるeコマースの拡大に拍車をかけている主な要因には、旺盛な一人当たり所得、高度な輸送・物流ネットワーク、インターネット普及率の上昇、技術の進歩などがあります。

- 包装食品に対する食欲の高まりは、段ボール包装の需要を増大させています。Interpack(包装見本市)によると、中東は世界の包装商品の5%を消費しており、そのビジネスは急速に成長しています。予測によると、需要は21%急増し、2026年には4,400万トンに達します。30%弱のシェアを持つサウジアラビアは、包装食品消費量で中東のトップです。さらに、持ち帰りや宅配サービスに傾倒する単身世帯が増えるにつれて、フードサービス業界の再編成が市場の成長をさらに促進すると予想されます。

飲料セグメントが大きなシェアを占める見込み

- 欧州および中東・アフリカでは飲料産業が重要な役割を果たしています。飲料セグメントの成長を牽引する主な決定要因には、人口の着実な増加、1人当たり収入、ライフスタイルの向上などがあります。経済的な制約から、一部のブランドオーナーは高価なパッケージを簡素化しなければならないです。二次包装は良い代用品であり、段ボール箱は手頃な包装オプションの一つです。

- ベンダーが持続可能性を優先するにつれ、従来の硬質パッケージング・ソリューションは、より環境に優しい段ボールパッケージングへと移行しています。顧客中心の製品と優れた製品保護に対する需要が高まる中、液体包装は実行可能で経済的な選択肢として浮上しています。このカテゴリーには、要求される保護レベルに合わせた様々なサイズと厚さの段ボールが含まれます。

- 政府の活動は、アルコール飲料市場に対する消費者の関心を高めると予想されます。ドイツの包装・ボトリング機械メーカーであるKrones AGによると、中東・アフリカにおける包装飲料の消費量は、2021年の約1,180億リットルから2024年には1,271億リットルに増加すると予想されています。

- ブランドは差別化を図るため、戦略的に段ボールパッケージング・ソリューションを採用し、ニーズに合わせた様々なフルーティング・オプション、厚さ、デザインを活用しています。カスタマイズ可能な印刷オプションの数々により、エンドユーザーはパッケージが棚で人目を引くことを保証し、売上成長を促進することができます。

- 液体飲料用段ボール箱で包装されるため、牛乳ベースの製品に対する需要の高まりが市場の成長を後押ししています。英国ソフトドリンク協会によると、2023年の英国におけるノンアルコール飲料は、炭酸飲料が38.6%でトップ、次いで希釈飲料、ボトル入り飲料水、その他の飲料となっています。

欧州および中東・アフリカの段ボール包装業界の概要

欧州および中東・アフリカの段ボール包装市場は断片化されており、多くの企業が段ボール包装ソリューションを提供しています。段ボール包装は、多様な製品を保護、保存、輸送するための費用対効果の高いソリューションです。軽量、生分解性、リサイクル性といった特性により、段ボールは包装業界の要としての役割を確固たるものにしています。段ボールは様々な印刷技術にとって理想的なキャンバスとなります。

市場は、インターナショナル・ペーパー、DSスミス、スマーフィット・カッパ、モンディ、ウェストロック、サイカ、モデル、ダナパック・パッケージングなどの企業が独占しています。大手企業が欧州および中東・アフリカ域内外で存在感と収益を拡大するために中小企業を買収するため、市場は統合されようとしています。M&Aは最も採用されている戦略のひとつであり、この傾向は今後も続くと予想されます。開発企業は持続可能な包装を開発し、環境に優しい包装商品を提供するために絶えず技術革新を行っています。各企業は、市場の成長機会を活用するため、様々なエンドユーザー産業向けに段ボール箱のデザインを発表しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 高いリサイクル価値と印刷技術革新への対応力による段ボール箱需要の促進

- 生鮮食品と青果物セグメントからの高い需要

- 市場の課題

- 段ボール製品の材料入手性と耐久性に対する懸念

第6章 市場セグメンテーション

- エンドユーザー産業別

- 加工食品

- 生鮮食品と青果物

- 飲料

- 紙製品

- その他エンドユーザー産業(電気製品、その他)

- 地域別

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- 欧州

第7章 競合情勢

- 企業プロファイル

- International Paper Company

- Mondi Group

- Smurfit Kappa Group

- DS Smith PLC

- Sealed Air Corporation

- WestRock

- Saica Group

- SCA Group

- Neopack

- Dunapack Packaging

- Arabian Packaging LLC

- VPK Packaging Group

- National Packaging Industries

- Corruseal Group

第8章 投資分析

第9章 市場の将来

目次

The EMEA Corrugated Board Packaging Market size is estimated at USD 7.02 billion in 2025, and is expected to reach USD 8.10 billion by 2030, at a CAGR of 2.91% during the forecast period (2025-2030).

Corrugated board packaging is a versatile and cost-efficient method of protecting, preserving, and transporting a wide range of products. Its attributes, such as light weight, biodegradability, and recyclability, have made it an integral component in the packaging industry.

Key Highlights

- Factors such as increasing demand for fresh food and beverages, home and personal products, logistics applications, electronic goods, building consumer awareness toward sustainable packaging, and the growth of the e-commerce industry are expected to increase corrugated box demand in EMEA during the forecast period.

- The e-commerce industry has emerged as a significant player in recent years. Prominent e-commerce companies, such as Amazon, have been using corrugated board boxes as their principal packaging while relying on plastic packaging for individual items. The corrugated board is highly versatile. Thus, it can take various forms other than the box, and due to sustainability issues, it is slowly replacing flexible plastic bags. Moreover, corrugated boxes are a perfect base for several printing techniques.

- The processed food segment accounts for the largest share in terms of the use of corrugated boards. The segment leads the overall market due to the massive prerequisite of foodstuffs being packed, stored, and transported to various places for consumption within and outside EMEA. Also, the need for green packaging materials, particularly paper packaging solutions, is fueled by the enforcement of strict legislation regarding the ban on single-use plastic.

- Germany is one of the prominent European markets for corrugated boxes. The country's principal industries, including pharmaceutical, automotive, food, and electronics, generate a high demand for corrugated boxes. For instance, according to the Federal Statistical Office of Germany, revenue from manufacturing corrugated paper and paperboard and containers of paper and cardboard in Germany amounted to approximately USD 24.03 billion by 2023.

- Fluctuations in raw material prices affect the production costs of corrugated products, which decreases the firmness and strength of corrugated boxes. Corrugated packing also has poor fire resistance. Hence, the low strength of corrugated materials and poor barrier properties hinder the growth of the market.

EMEA Corrugated Board Packaging Market Trends

The Processed Foods Segment is Expected to Occupy a Significant Market Share

- The need for convenience foods is anticipated to grow owing to the busy lifestyles in EMEA. Processed food can be cooked in less time, which attracts consumers. The growing population is anticipated to drive the need for processed food, which is convenient and healthy. Additionally, the increasing realization among users regarding the practice of environment-friendly products is expected to drive the demand for corrugated board packaging in the region.

- Government drives to stimulate eco-friendly packaging materials, coupled with the efforts of the Corrugated Packaging Alliance, a corrugated industry initiative to strengthen corrugated packaging, provide an added stimulus to this market's growth.

- According to Statistisches Bundesamt, the German convenience food production business earned USD 6.35 billion in revenue in 2022, which increased to USD 6.35 billion in 2023. The convenience food industry significantly relies on packaging options to guarantee its products' protection and safe transit. As the convenience food production industry in Germany develops, the demand for corrugated board packaging to satisfy these needs will rise.

- Strict legislation banning single-use plastics has intensified the demand for green packaging materials, especially paper-based solutions. The rising popularity of e-commerce platforms in the region further drives market demand. E-commerce has significantly transformed the retail landscape. Key drivers fueling e-commerce's expansion in the Middle East, particularly in the Gulf region, include robust per capita income, advanced transportation and logistics networks, rising internet penetration, and technological advancements.

- The rising appetite for packaged food is increasing the demand for corrugated board packaging. According to Interpack (a packaging trade fair), the Middle East consumes 5% of the world's packaged goods, and its business is rapidly growing. Projections indicate a 21% surge in demand, reaching 44 million tons by 2026. Saudi Arabia, holding just under a 30% share, tops the Middle East in packaged food consumption. Additionally, as more single households lean toward takeaway and delivery services, the reshaped foodservice industry is expected to further propel the growth of the market.

The Beverage Segment is Expected to Hold a Significant Share

- The beverage industry plays an essential role in EMEA. The principal determinants driving the growth of the beverage segment include a steadily growing population, per capita revenue, and improving lifestyles. Due to economic constraints, some brand owners must simplify their pricey packaging. Secondary packaging is a good substitute, and corrugated boxes are among the affordable packaging options.

- As vendors prioritize sustainability, traditional rigid packaging solutions give way to more eco-friendly corrugated board packaging. With the rising demand for customer-centric products and superior product protection, liquid packaging is emerging as a viable and economical choice. This category includes corrugated boards in various sizes and thicknesses tailored to the required protection level.

- The government's activities are anticipated to increase consumer interest in the alcoholic beverage market. According to Krones AG, a German packaging and bottling machine manufacturer, consumption of packaged beverages in Middle East and Africa is expected to increase to 127.1 billion liters by 2024 from nearly 118 billion liters in 2021.

- Brands strategically employ corrugated packaging solutions to differentiate themselves, utilizing various fluting options, thicknesses, and designs tailored to their needs. With a range of customizable printing options, end users can ensure their packages are eye-catching on shelves, driving sales growth.

- The growing demand for milk-based products is boosting market growth as they are packaged in liquid beverage corrugated milk carton boxes. According to the British Soft Drinks Association, in terms of non-alcoholic beverages in the United Kingdom in 2023, carbonated soft drinks took the top position with 38.6%, followed by dilutables, bottled water, and other drinks.

EMEA Corrugated Board Packaging Industry Overview

The corrugated board packaging market in EMEA is fragmented, with many companies offering corrugated board packaging solutions. Corrugated board packaging is a cost-effective solution for safeguarding, preserving, and transporting diverse products. Attributes like lightweight, biodegradability, and recyclability have cemented the corrugated board's role as a cornerstone of the packaging industry. Corrugated boxes provide an ideal canvas for various printing techniques.

The market is dominated by players, including International Paper, DS Smith, Smurfit Kappa, Mondi, WestRock, Saica, Model, and Dunapack packaging. The market is set for consolidation as the big players acquire smaller players to expand their presence and revenue throughout and outside EMEA. Mergers and acquisitions have been among the most adopted strategies; this trend is expected to continue in the coming years. Businesses continually innovate to develop sustainable packaging and render environment-friendly packaging goods. The players are launching corrugated box designs for various end-user industries to leverage market growth opportunities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclable Value and Ability to Support Innovations in Printing to aid Demand for Corrugated Boxes

- 5.1.2 High Demand from the Fresh Food & Produce Segment

- 5.2 Market Challenges

- 5.2.1 Concerns over Material Availability and Durability of Corrugated Board-based Products

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Processed Foods

- 6.1.2 Fresh Food and Produce

- 6.1.3 Beverages

- 6.1.4 Paper Products

- 6.1.5 Other End-user Industries (Electrical Products and Others)

- 6.2 By Geography

- 6.2.1 Europe

- 6.2.1.1 United Kingdom

- 6.2.1.2 Germany

- 6.2.1.3 France

- 6.2.1.4 Spain

- 6.2.1.5 Italy

- 6.2.2 Middle East and Africa

- 6.2.2.1 South Africa

- 6.2.2.2 Saudi Arabia

- 6.2.2.3 United Arab Emirates

- 6.2.1 Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Mondi Group

- 7.1.3 Smurfit Kappa Group

- 7.1.4 DS Smith PLC

- 7.1.5 Sealed Air Corporation

- 7.1.6 WestRock

- 7.1.7 Saica Group

- 7.1.8 SCA Group

- 7.1.9 Neopack

- 7.1.10 Dunapack Packaging

- 7.1.11 Arabian Packaging LLC

- 7.1.12 VPK Packaging Group

- 7.1.13 National Packaging Industries

- 7.1.14 Corruseal Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日