|

市場調査レポート

商品コード

1910471

中東・アフリカの乳製品:市場シェア分析、業界動向、統計、成長予測(2026年~2031年)Middle East And Africa Dairy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの乳製品:市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 276 Pages

納期: 2~3営業日

|

概要

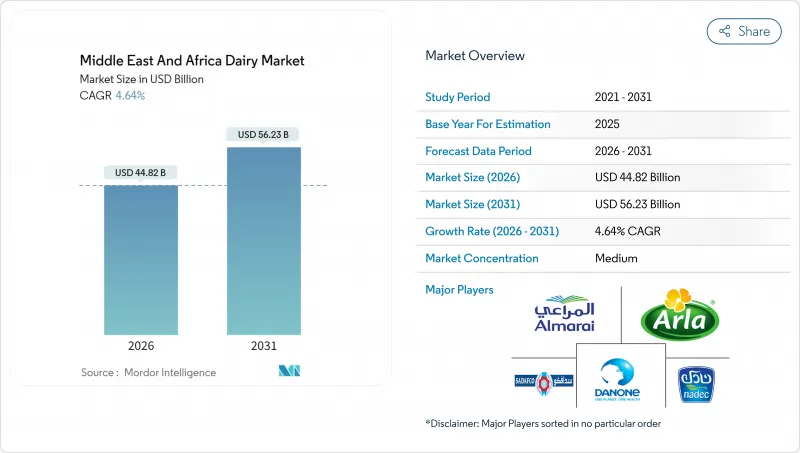

中東・アフリカの乳製品の市場規模は、2026年に448億2,000万米ドルに達すると予測されております。

これは2025年の428億3,000万米ドルから成長した数値であり、2031年には562億3,000万米ドルに達すると見込まれております。2026年から2031年にかけてはCAGR4.64%で拡大する見通しです。

この成長は、政府資金による学校給食向け牛乳プログラム、外出先での消費に対応した製品革新、機能性メリットを備えたプレミアム製品への需要増加によって支えられています。しかしながら、コールドチェーンインフラの不足や植物由来代替品との競合といった課題が、さらなる拡大を制限しています。サウジアラビアは、アルマライ社による農場から物流までの事業への48億米ドル投資を背景に、2024年の生産量の31.31%を占めると予測されています。アラブ首長国連邦は、有機牛乳およびラクダ乳ブランドの成長に支えられ、5.89%のCAGRで最も高い成長率を達成すると見込まれています。ヨーグルトはプロバイオティクス含有のスプーンで食べられるタイプや飲料タイプの人気により、CAGR5.93%で最も急速に成長するカテゴリーです。一方、冷蔵保管の課題を解決する常温保存可能な超高温殺菌(UHT)製品により、牛乳は主要カテゴリーとしての地位を維持しています。2024年の小売流通では、現代的な小売チャネルが65.43%を占めると予測されています。一方、ホテル、レストラン、カフェなどの飲食店チャネルは、湾岸地域のホスピタリティ産業の回復に伴い、回復傾向にあります。競争の激しさは依然として中程度であり、主要な国内企業は強固な国内市場での地位を活かして利益を得ています。一方、多国籍企業は合弁事業やプレミアム製品セグメントを通じて、ますます市場に参入しています。

中東・アフリカの乳製品市場の動向と洞察

健康意識の高まりにより、プロバイオティクス、強化、乳糖フリーの乳製品への関心が高まっています。

機能性乳製品は、ニッチなカテゴリーから、湾岸協力会議(GCC)地域における標準的な期待へと変化しています。これは、生きた培養菌、添加ビタミン、乳糖フリーの表示など、消費者が成分表示にますます注目していることから推進されています。アブダビでは、2024年の学校栄養ガイドラインにより、公立学校で提供されるすべての乳製品は、カルシウムとビタミンDの特定の最低基準値を満たすことが義務付けられており、これにより、商品サプライヤーは事実上排除され、強化に投資するブランドが優先されています。例えば、アラブ首長国連邦のMleiha Dairy社は、2025年初めに乳糖を含まないラバン製品ラインを発売し、乳糖不耐症の中東の成人の大きな割合のニーズに対応することで、首長国のラバン市場で瞬く間に大きなシェアを獲得しました。サウジアラビアでは、腸内細菌叢の健康と免疫力の関連性を強調したソーシャルメディアキャンペーンが後押しとなり、プロバイオティクスヨーグルトの需要が急増しました。パンデミック後の健康意識の高まりの中で、このメッセージは消費者に強く共鳴したのです。同様に、ダノンのアクティビアブランドはビフィドバクテリウム・ラクティス菌株を配合した新処方により、2024年にエジプトで顕著な販売量増加を記録しました。これは科学的に裏付けられた菌株の特異性が、価格に敏感な市場においてもプレミアム価格設定を正当化できることを示しています。さらに2024年には、米国・アラブ首長国連邦ビジネス協議会が報告した通り、連邦政府が医療分野に50億ディルハムを配分しました。

政府支援の学校給食・栄養プログラムが安定した機関需要を創出

学校給食向け牛乳事業は生産者にとって安定した需要基盤を提供し、小売市場の変動から保護すると同時に、厳格な品質基準とトレーサビリティ要件を課します。これは垂直統合型乳業メーカーにとって有利に働くことが多くあります。2024年、サウジアラビア教育省は5年間の学校給食向け牛乳契約を更新し、年間数億個に及ぶ200ミリリットルパックを数百万人の生徒に供給することを約束しました。これは同国の液体乳総消費量において重要な割合を占めています。アルマライ社とサダフコ社が共同でこの契約を請け負い、超高温殺菌処理(UHT)技術を活用することで冷蔵不要の保存期間を数ヶ月延長。信頼性の高い冷蔵設備が限られる遠隔地の学校にとって極めて重要な特長です。エジプトでは、数百万世帯を支援するタカフル・カラマ社会保護プログラムにおいて、政府指定小売店で利用可能な乳製品引換券が毎月支給されています。これにより年間で相当量の資金が正規乳業部門に流入し、非正規の無名牛乳源への依存度が低下しています。一方カタールでは、保健最高評議会が全学校食堂に対し、1食あたり少なくとも1種類の強化乳製品を提供することを義務付けています。これを受けバラドナ社はビタミンD強化フレーバーミルクを開発し、現在では同社の国内収益に大きく貢献しています。さらにサウジアラビアでは、教育省が全国的な学校栄養プログラムの影響力を強調しています。このプログラムは35,000校の学校で520万人の生徒に提供され、2024年には約4億米ドルに相当する安定した機関需要を生み出しています。

都市部を中心に高まる植物性代替品への消費者関心

植物性ミルク代替品は、ニッチな健康食品店からドバイ、リヤド、カイロの主要スーパーマーケットの目立つ棚へと移行し、都市部のミレニアル世代およびZ世代消費者における乳製品の販売数量シェアを減少させています。アラブ首長国連邦発のオートミルクブランド「ニュートリー」は2024年に立ち上げられ、6ヶ月以内にカルフールとスピニーズへの商品掲載を達成、初年度売上高は320万米ドルを記録しました。この数字は控えめに見えますが、数年前までこうした製品がほとんど存在しなかった市場における植物性乳製品の急速な普及を反映しています。2024年、アラブ首長国連邦ではアーモンド飲料とオートミルクの消費量が大幅に増加した一方、従来の牛乳の成長はごくわずかでした。この格差を受け、アルマライ社は2025年9月、2026年に植物性製品ラインの立ち上げを検討する計画を発表しました。さらに、ファームランドグラブ社の調査によれば、2024年時点でサウジアラビアの人口の10%がベジタリアンまたはヴィーガンと自認しています。

セグメント分析

2025年の製品タイプ別シェアでは、牛乳が33.12%を占めました。これは主に、湾岸協力会議(GCC)地域で大きな地位を占める超高温殺菌(UHT)牛乳のバリエーションが牽引したものです。この地域では、夏の間は通常35℃から45℃という高温が持続するため、特に主要都市部以外の地域では、冷蔵生乳の流通に物流上の問題が生じます。そのため、冷蔵を必要とせず、この地域の気候や物流状況に適したUHTミルクが好まれるようになっています。

ヨーグルトは、2026年から2031年にかけて、CAGR 5.70%の成長が見込まれています。これは、忙しいライフスタイルに合わせた、プロバイオティクスを豊富に含む飲用タイプのヨーグルトの人気が高まっていることが背景にあります。特に、ダノンのアクティビアと、SADAFCOのサウディアヨーグルトなどの現地ブランドは、2024年にサウジアラビアで合計21%の販売数量増加を記録しました。チーズの輸入は、欧州風ナチュラルチーズを求める駐在員の需要と、メニュー標準化のために加工チーズに依存するファストフードチェーンの影響により、2030年までに金額ベースで26%増加すると予想されています。南アフリカでは、ピザやハンバーガーチェーンの店舗網拡大に伴い、クローバー・インダストリーズ社のチェダー製品ラインが2024年に14%の成長を記録し、乳製品市場全体の成長率を上回りました。

中東・アフリカの乳製品市場レポートは、製品タイプ(バター、チーズ、クリーム、乳製品デザート、牛乳、ヨーグルト、サワーミルク飲料)、流通チャネル(オントレード、オフトレード)、地域(アラブ首長国連邦、カタール、サウジアラビア、エジプト、バーレーン、オマーン、その他)別に分類されています。市場予測は金額(米ドル)および数量(リットル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 健康意識の高まりにより、プロバイオティクス、栄養強化、乳糖不使用の乳製品への関心が増加

- 政府支援の学校給食・栄養プログラムによる安定した機関需要の創出

- バランスの取れた食事と十分なカルシウム、ビタミンD、タンパク質の摂取を促進する公衆衛生キャンペーン

- 消費者の利便性を重視した、すぐに飲める形態や単品包装の乳製品への嗜好の高まり

- 有機および「クリーンラベル」乳製品への関心の高まり

- ラバン、ラブネ、酸乳飲料などの伝統的製品に対する文化的愛着

- 市場抑制要因

- 特に都市部における、植物由来代替品への消費者関心の高まり

- 環境および動物福祉に対する要求の高まりによるコンプライアンスコストの増加

- 輸入原材料のハラール認証遅延とコストが、イノベーションの速度と新製品発売を制限

- 不十分なコールドチェーン網と電力供給の信頼性

- 消費者行動分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額ベースおよび数量ベース)

- 製品タイプ別

- バター

- チーズ

- ナチュラルチーズ

- チェダー

- カッテージ

- リコッタ

- パルメザン

- その他

- プロセスチーズ

- ナチュラルチーズ

- クリーム

- 生クリーム

- クッキングクリーム

- ホイップクリーム

- その他

- 乳製品デザート

- アイスクリーム

- チーズケーキ

- 冷凍デザート

- その他

- 牛乳

- 練乳

- フレーバーミルク

- 生乳

- UHT牛乳(超高温殺菌牛乳)

- 粉ミルク

- ヨーグルト

- 飲用

- スプーナブル

- サワーミルク飲料

- 流通チャネル別

- オントレード

- オフトレード

- コンビニエンスストア

- 専門店

- スーパーマーケットおよびハイパーマーケット

- オンライン小売

- その他

- 国別

- アラブ首長国連邦

- カタール

- サウジアラビア

- バーレーン

- オマーン

- クウェート

- ナイジェリア

- エジプト

- 南アフリカ

- イラン

- その他中東諸国

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Almarai Company

- Saudia Dairy and Foodstuff Company(SADAFCO)

- National Agricultural Development Company(NADEC)

- Arla Foods AmbA

- Groupe Lactalis

- Nestle S.A.

- Al Rashed Food Company

- AlRawabi Dairy Company

- Danone SA

- Bel SA

- Fonterra Co-operative Group

- National Food Products Company(NFC)

- Almunajem Foods

- Saad Group

- Al-Jouf Agriculture Development Company

- Al Marai Home

- Saudi Modern Factory for Food Industries

- Tamimi Markets

- Nesma Holding

- Gulf Dairy Products Company

- Bateel Dairy