南米の乳製品:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Dairy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 259 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693889

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

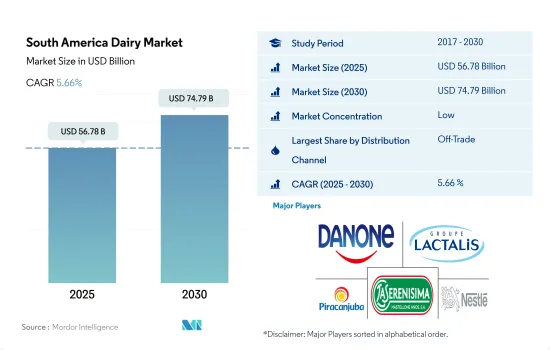

南米の乳製品市場規模は2025年に567億8,000万米ドルと推定・予測され、2030年にはCAGR 5.66%で成長し747億9,000万米ドルに達すると予測されます。

スーパーマーケットやハイパーマーケットを通じた顕著な販売に牽引される流通チャネルの広範な採用が成長を後押ししています。

- 南米の乳製品市場の流通チャネルを支配しているのは非売品セグメントです。オフトレードセグメントでは、消費者は主にコンビニエンスストアで乳製品を購入することを好みます。その結果、コンビニエンスストアは乳製品販売の主要な流通チャネルと見なされ、国全体の売上の48.5%以上を占めています。

- スーパーマーケットとハイパーマーケットは、南米で乳製品を購入する際にコンビニエンスストアに次いで広く好まれている商外流通チャネルです。2022年には、スーパーマーケットとハイパーマーケットが金額シェアの43.9%を占めました。

- Grupo Exito、Carrefour、Walmart、Jumboのような様々なスーパーマーケットやハイパーマーケットチェーンは、消費者を囲い込むために様々なロイヤルティ特典を提供しています。事業の拡大やスーパーマーケットやハイパーマーケットの増加といった要因とともに、こうした小売業態の成長は、南米における乳製品の購入にプラスの影響を与えています。2021年には、Grupo Exitoが南米全土に2,600以上の店舗を展開し、首位に立りました。2位はCarrefourで、同地域で1,200以上の店舗を展開しています。

- 乳製品は南米のレストランや外食チャネルで一般的に使用されており、これが市場の成長をさらに後押ししています。南米の大手レストランチェーンは、牛乳、ヨーグルト、チーズをメニューに加えています。オンチャネルにおける乳製品の売上は、2022年と比較して2025年には9%成長すると予測されます。この成長は、消費者が外食やテイクアウトを好むことによって助長されると予想されます。

ブラジルとアルゼンチンは南米の主要な乳製品生産国であり、地域全体の数量を押し上げています。

- 南米の乳製品産業は2022年に3.24%の成長を遂げました。この成長は、乳製品がかなりの量の必須栄養素を提供するため、健康に対する意識が高まっているためです。コップ1杯の牛乳には3.4グラムのタンパク質、5グラムの炭水化物、0.6グラムの飽和脂肪酸、その他の栄養素が含まれています。このため、健康的な食生活を維持しようとする人々の間で、乳製品への関心が高まっています。このため、乳製品産業は予測期間中に3.51%の成長が見込まれています。

- 南米の乳製品産業ではブラジルが大きなシェアを占めています。ロングライフ牛乳の台頭は、ブラジルの生乳産業を一変させました。現在、消費者は毎日新鮮牛乳を買うのではなく、12リットル入りのパックを購入して保存しています。ブラジルの多くの場所で冷蔵設備が整っていないことも、ロングライフ牛乳の全国的な普及を後押ししています。2021年、ブラジルは1億4,900万米ドル相当のホエイ、ミルクアルブミン、カゼイン製品を輸入しました。しかし、高い生産コストや予測不可能な天候や経済状況などの課題により、乳業は予測期間中にいくつかの障害に直面する可能性があります。

- 無糖または減糖、低脂肪、牧草飼育、オーガニックなどの健康的な乳製品への需要が、予測期間中の同地域の市場成長を促進すると予想されます。2018~2022年にかけて、ブラジルの生鮮乳製品消費量は約7%増加し、2021年には1人当たりほぼ76.8kgに達しました。生乳の生産量の多さ、高品質の乳製品に対する消費者の嗜好の高まり、これらの製品の製造を促進するための適切な産業規制が、主要な促進要因として特定されています。

南米の乳製品市場動向

タンパク質が豊富な食品を積極的に求める消費者の健康志向の高まりがセグメントに大きく影響

- 南米の乳製品市場は、主にタンパク質が豊富な食品を積極的に求める消費者の健康意識の高まりによって牽引されています。肥満関連の問題(糖尿病、高血圧、心臓病)と闘うために政府が実施する健康増進キャンペーンの増加などの要因が、消費者に健康的な製品の購入を促し、乳製品の消費を直接的に押し上げています。

- チーズは、サンドイッチ、ハンバーガー、ピザ、パスタなどに広く使われているため、最も消費量の多い乳製品のひとつです。そのため、より高品質で、よりおいしく、より健康的で健全な品質のチーズに対する需要が、消費者の間で関心事となっています。例えば、アルゼンチンのチーズは、同国で最も生産量の多い乳製品です。また、アルゼンチンはラテンアメリカで最もチーズを消費する国でもあります。したがって、2023~2024年にかけて、チーズの一人当たり消費量は2.87%増加すると推定されます。

- 南米地域内では、ブラジルが最も消費量が多く、乳製品市場全体を支配しています。ブラジルには現在推定1,822の酪農場があります。近年、チーズの生産は主に家庭消費者と食品サービス/レストラン部門からの強い需要により増加しています。2023年のブラジル人のチーズ消費量は1人当たり年間約6.07キログラムで、世界平均を30%以上下回っており(国連食糧農業機関(FAO)調べ)、消費拡大の可能性が大きいです。

- ペルー、パラグアイ、エクアドル、ウルグアイといった国々では、政府の積極的な取り組みにより、予測期間中に乳製品の消費量がより高い割合で増加すると予想されます。

南米の乳製品産業概要

南米の乳製品市場はセグメント化されており、上位5社で21.46%を占めています。この市場の主要企業は、Danone SA、Groupe Lactalis、Laticinios Bela Vista Ltda、Mastellone Hermanos SA、Nestle SAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たりの消費量

- 原料/商品生産量

- バター

- チーズ

- 牛乳

- 規制の枠組み

- アルゼンチン

- ブラジル

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- バター

- 製品タイプ別

- 培養バター

- 未加工バター

- チーズ

- 製品タイプ別

- 天然チーズ

- プロセスチーズ

- クリーム

- 製品タイプ別

- ダブルクリーム

- シングルクリーム

- ホイップクリーム

- その他

- 乳製品デザート

- 製品タイプ別

- チーズケーキ

- フローズンデザート

- アイスクリーム

- ムース

- その他

- 牛乳

- 製品タイプ別

- コンデンスミルク

- フレーバーミルク

- フレッシュミルク

- 粉ミルク

- UHTミルク

- サワーミルクドリンク

- ヨーグルト

- 製品タイプ別

- フレーバーヨーグルト

- ノンフレーバーヨーグルト

- バター

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Alpina Productos Alimenticios SA BIC

- Danone SA

- Groupe Lactalis

- Lacteos Betania SA

- Laticinios Bela Vista Ltda

- Mastellone Hermanos SA

- Nestle SA

- SanCor Cooperativas Unidas Limitada

- Sucesores de Alfredo Williner SA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50000760

The South America Dairy Market size is estimated at 56.78 billion USD in 2025, and is expected to reach 74.79 billion USD by 2030, growing at a CAGR of 5.66% during the forecast period (2025-2030).

Widespread adoption of distribution channels, led by remarkable sales through supermarkets and hypermarkets is propelling the growth

- The off-trade segment dominates the distribution channels of the South American dairy market. In the off-trade segment, consumers prefer buying dairy products majorly from convenience stores, as people get discount coupons for bulk shopping. As a result, convenience stores are considered the primary sales channel for the sales of dairy products, as they hold more than 48.5% of the overall sales across the country.

- Supermarkets and hypermarkets are the second most widely preferred off-trade distribution channels after convenience stores for purchasing dairy products in South America. In 2022, supermarkets and hypermarkets accounted for 43.9% of the value share.

- Different supermarket and hypermarket chains like Grupo Exito, Carrefour, Walmart, and Jumbo offer different loyalty benefits to retain consumers. The growth of these retail formats, along with factors like business expansion and the increase in supermarkets and hypermarkets, has positively impacted the purchase of dairy products in South America. In 2021, Grupo Exito stood in the top place with more than 2,600 locations across South America. Carrefour stood in second place and operated more than 1,200 outlets across the region.

- Dairy products are commonly used in South American restaurants and foodservice channels, which is further boosting the market growth. Major restaurant chains in South America add milk, yogurt, and cheese to their menus. Dairy sales in the on-trade channel are anticipated to grow by 9% in 2025 compared to 2022. The growth is expected to be aided by consumers preferring dining out or ordering takeout.

Brazil and Argentina are the major dairy producing countries of the South America which boost the overall region's volume sales

- The dairy industry in South America witnessed a growth of 3.24% in 2022. The growth was due to the rising consciousness about health, as dairy products offer a significant volume of essential nutrients. One cup of milk offers 3.4 grams of protein, 5 grams of carbohydrates, 0.6 grams of saturated fat, and other nutrients. This has led to an increased interest in dairy products as people seek to maintain a healthy diet. Thus, the dairy industry is expected to grow by 3.51% during the forecast period.

- Brazil holds the major share in the South American dairy industry. The rise of long-life milk has transformed the fresh milk industry in Brazil. Nowadays, rather than buying fresh milk every day, consumers purchase 12-liter packs and store them. The fact that many places in Brazil lack refrigeration has also boosted the geographical distribution of long-life milk across the country. In 2021, Brazil imported whey, milk albumin, and casein products worth USD 149 million. However, due to the challenges like high production costs and unpredictable weather and economic conditions, the dairy industry may face some hindrances during the forecast period.

- Demand for healthy dairy variants such as no or reduced sugar, low-fat content, grass-fed, and organic is anticipated to drive market growth in the region during the forecast period. Between 2018 and 2022, fresh dairy product consumption in Brazil rose by around 7%, reaching almost 76.8 kg per person in 2021. High production of raw milk, rising consumer preference for quality dairy products and adequate industry regulation to facilitate the manufacturing of these products are identified as the key driving factors.

South America Dairy Market Trends

Rising health consciousness among consumers who actively seek protein-rich food products has largely impacted the segment

- The South American dairy market is primarily driven by rising health consciousness among consumers who actively seek protein-rich food products. Factors such as increasing government-run health and wellness campaigns designed to combat obesity-related problems (diabetes, high blood pressure, and heart disease) encourage consumers to purchase healthier products, directly boosting the consumption of dairy products.

- Cheese is one of the highest consumed dairy products due to its widespread usage in sandwiches, burgers, pizzas, pasta, etc., Thus, demand for higher-quality, better-tasting, and healthier, wholesome quality cheese has become a point of concern among consumers. For example, Argentine cheese is by far the most-produced dairy product in the country. Argentina is also the prominent Latin American country that consumes the most cheese. Thus, the per capita consumption of cheese is estimated to increase by 2.87% during 2023-2024.

- Within the South American region, Brazil dominates the overall dairy market with the highest consumption. There are currently an estimated 1,822 dairies in Brazil. In recent years, the production of cheese has increased mainly due to strong demand from household consumers and foodservice/restaurant sectors. In 2023, Brazilians consumed around 6.07 kilograms of cheese per person/year, which is almost more than 30% below the global average (according to the UN Food and Agriculture Organization - FAO), meaning there is much potential for consumption growth.

- The consumption of dairy products in countries like Peru, Paraguay, Ecuador, and Uruguay is expected to increase at a higher rate during the forecast period due to favorable initiatives from the government.

South America Dairy Industry Overview

The South America Dairy Market is fragmented, with the top five companies occupying 21.46%. The major players in this market are Danone SA, Groupe Lactalis, Laticinios Bela Vista Ltda, Mastellone Hermanos SA and Nestle SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Butter

- 4.2.2 Cheese

- 4.2.3 Milk

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Butter

- 5.1.1.1 By Product Type

- 5.1.1.1.1 Cultured Butter

- 5.1.1.1.2 Uncultured Butter

- 5.1.2 Cheese

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Natural Cheese

- 5.1.2.1.2 Processed Cheese

- 5.1.3 Cream

- 5.1.3.1 By Product Type

- 5.1.3.1.1 Double Cream

- 5.1.3.1.2 Single Cream

- 5.1.3.1.3 Whipping Cream

- 5.1.3.1.4 Others

- 5.1.4 Dairy Desserts

- 5.1.4.1 By Product Type

- 5.1.4.1.1 Cheesecakes

- 5.1.4.1.2 Frozen Desserts

- 5.1.4.1.3 Ice Cream

- 5.1.4.1.4 Mousses

- 5.1.4.1.5 Others

- 5.1.5 Milk

- 5.1.5.1 By Product Type

- 5.1.5.1.1 Condensed milk

- 5.1.5.1.2 Flavored Milk

- 5.1.5.1.3 Fresh Milk

- 5.1.5.1.4 Powdered Milk

- 5.1.5.1.5 UHT Milk

- 5.1.6 Sour Milk Drinks

- 5.1.7 Yogurt

- 5.1.7.1 By Product Type

- 5.1.7.1.1 Flavored Yogurt

- 5.1.7.1.2 Unflavored Yogurt

- 5.1.1 Butter

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alpina Productos Alimenticios SA BIC

- 6.4.2 Danone SA

- 6.4.3 Groupe Lactalis

- 6.4.4 Lacteos Betania SA

- 6.4.5 Laticinios Bela Vista Ltda

- 6.4.6 Mastellone Hermanos SA

- 6.4.7 Nestle SA

- 6.4.8 SanCor Cooperativas Unidas Limitada

- 6.4.9 Sucesores de Alfredo Williner SA

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

南米の乳製品:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 259 Pages

- 納期

- 2~3営業日