|

市場調査レポート

商品コード

1693879

中国の乳製品:市場シェア分析、産業動向と統計、成長予測(2025~2030年)China Dairy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の乳製品:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 251 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

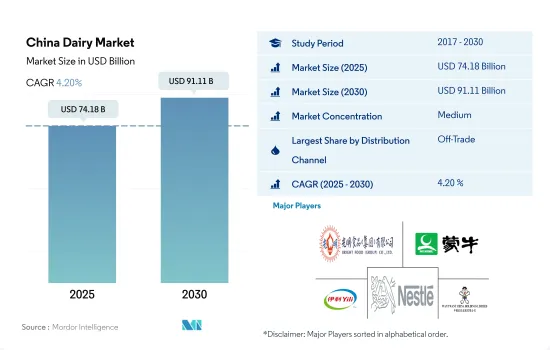

中国の乳製品市場規模は2025年に741億8,000万米ドルと推定・予測され、2030年には911億1,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは4.20%で成長すると予測されます。

拡大するストリートフード文化と家庭外消費の増加が市場成長の原動力

- この地域における乳製品の販売では、家庭外チャネルが大きな役割を果たしています。商業外チャネルの中では、スーパーマーケットとハイパーマーケットが中国の乳製品市場における最大の流通チャネルです。これらのチャネルは、特に大都市や市場において、消費者の購買意思決定に影響を与えるという点で有利です。2023年には、スーパーマーケットとハイパーマーケットが金額シェアの64%を占めました。

- オンラインチャネルは、オフトレードセグメントで最も急成長している流通チャネルになると予想されます。2023~2025年の間に、前年比22.4%の成長値を記録すると予測されています。食料品のオンラインショッピングに移行した買い物客の主要動機は利便性です。

- 中国全土で拡大するストリートフード文化は、予測期間中、チーズ、バター、乳製品デザートのような乳製品のオントレード消費を促進すると予想されます。サブウェイ、マクドナルド、バーガーキング、KFCなどのファーストフードブランドが、中国の外食フランチャイズ市場を独占しています。オンチャネルを通じた乳製品の販売額は、2022~2025年にかけて9.7%の成長が見込まれます。

- すべての乳製品の中で、牛乳はオフトレード小売チャネル全体のシェアの大半を占めています。2022年には、牛乳はカテゴリー全体の54.5%を占め、ヨーグルトは金額シェア38%で2位につけています。乳製品の旺盛な消費パターンと日常的な食生活における需要により、これらの製品の消費パターンがオフトレードとオントレードの両方のモードを通じて促進されると予想されます。オフチャネルを通じた乳製品消費は、2024~2027年の間に29%成長すると予測されます。

中国の乳製品市場の動向

国内での健康意識の高まりが乳製品と乳製品の消費を後押し

- 消費者の嗜好は、乳製品の消費要件を示唆する食品ベースの食生活指針に影響されます。中国住民のための食事指導では、流動食ベースで1日300gの乳製品摂取を推奨しており、同国における乳製品消費の継続的成長の可能性を示しています。生乳生産は主に中国北部に集中しており、次いで中国南部と東部となっています。チーズは、ピザ、ハンバーガー、パスタ、サンドイッチ、タコスなどの洋食志向が強いため、レストランからの需要が強く、消費される乳製品の中でも人気が高いです。チーズの一人当たり消費量は、2023~2024年にかけて7.10%増加すると推定されます。

- 消費者の健康意識の高まりも、特にCOVID-19の発生後、中国での乳製品消費を押し上げています。中国税関によると、2021年に中国が外国から購入したチーズは17万6,000トンで、2020年から36.3%増加し、ニュージーランド、オーストラリア、デンマークが輸出国トップ3でした。一人当たりのヨーグルト消費量が増加していることから、各社はグルテンフリーや非遺伝子組み換えを謳ったヨーグルト製品の開発に力を入れています。プレーンヨーグルトは、消費者の好みに応じて、無脂肪、低脂肪、全乳のバリエーションもあり、ディップ、スムージー、焼き菓子にも利用できます。低温殺菌牛乳とヨーグルトは2021年に全国学校給食用牛乳プログラムに追加され、これらの製品の需要を支えています。消費者のライフスタイルや食習慣の変化は、それに伴う利便性の要因から、粉ミルクのようなすぐに使える製品の需要を押し上げています。粉ミルクの一人当たり消費量は、2023~2024年にかけて1.14%増加すると推定されます。

中国の乳製品産業概要

中国の乳製品市場は適度に統合されており、上位5社で48.34%を占めています。この市場の主要企業は、Bright Food(Group)、China Mengniu Dairy Company Limited、Inner Mongolia Yili Industrial Group、Nestle SA、Want Want Holdings Limitedなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産量

- バター

- チーズ

- 牛乳

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- バター

- 製品タイプ別

- 培養バター

- 未加工バター

- チーズ

- 製品タイプ別

- 天然チーズ

- プロセスチーズ

- クリーム

- 製品タイプ別

- ダブルクリーム

- シングルクリーム

- ホイップクリーム

- その他

- 乳製品デザート

- 製品タイプ別

- チーズケーキ

- フローズンデザート

- アイスクリーム

- ムース

- その他

- 牛乳

- 製品タイプ別

- コンデンスミルク

- フレーバーミルク

- フレッシュミルク

- 粉ミルク

- UHTミルク

- ヨーグルト

- 製品タイプ別

- フレーバーヨーグルト

- ノンフレーバーヨーグルト

- バター

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Bright Food(Group)Co. Ltd

- China Mengniu Dairy Company Limited

- Danone SA

- Fonterra Co-operative Group Limited

- Inner Mongolia Yili Industrial Group Co. Ltd

- Junlebao Dairy Group

- Nestle SA

- Panda Dairy Group Co. Ltd

- VV Group Co. Ltd

- Want Want Holdings Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The China Dairy Market size is estimated at 74.18 billion USD in 2025, and is expected to reach 91.11 billion USD by 2030, growing at a CAGR of 4.20% during the forecast period (2025-2030).

Expanding street food culture and rising out-of-home consumption fuels the market growth

- The off-trade channel plays a major role in the sales of dairy products in the region. Among the off-trade channels, supermarkets and hypermarkets are the largest distribution channels in the Chinese dairy market. The proximity factor of these channels, especially in large and developed cities, provides them with an added advantage in influencing consumers' decisions to purchase among the large variety of products available in the market. In 2023, supermarkets and hypermarkets accounted for 64% of the value share.

- The online channel is expected to be the fastest-growing distribution channel in the off-trade segment. It is projected to register a growth value of 22.4% Y-o-Y during the period 2023-2025. Convenience is the primary motivation for shoppers who have transitioned to shopping for groceries online.

- The expanding street food culture across China is anticipated to drive the on-trade consumption of dairy products like cheese, butter, and dairy desserts during the forecast period. Fast food brands, including Subway, McDonald's, Burger King, and KFC, dominate the landscape for restaurant franchises in the country. The sales value of dairy products through the on-trade channel is anticipated to grow by 9.7% in 2025 from 2022.

- Among all the dairy products, milk accounted for the majority of the share in overall off-trade retail channels. In 2022, milk accounted for 54.5% of the total category, and yogurt stood in second place with 38% of the value share. The strong consumption patterns of dairy products and their demand in a regular diet are anticipated to drive the consumption patterns of these products through both off-trade and on-trade modes. Dairy consumption through the off-trade channel is anticipated to grow by 29% during 2024-2027.

China Dairy Market Trends

Growing health awareness in the country boosting the consumption of dairy and dairy products

- Consumer preference is influenced by food-based dietary guidelines, which suggest the consumption requirements of dairy. The Dietary Guidance for Chinese Residents recommends a daily intake of 300 grams of dairy products on a fluid milk basis, indicating the potential for continued growth in dairy consumption in the country. Raw milk production is mainly concentrated in northern China, followed by southern and eastern China. Cheese is popular among the dairy products consumed due to strong demand from restaurants as there is an inclination toward Western-style food like pizza, burgers, pasta, sandwiches, and tacos. The per capita consumption of cheese is estimated to increase by 7.10% from 2023 to 2024.

- Growing health consciousness among consumers is also boosting dairy consumption in China, especially post the COVID-19 outbreak. China Customs indicated that China bought 176,000 metric tons of cheese from foreign countries in 2021, up by 36.3% from 2020, with New Zealand, Australia, and Denmark as the top three exporters. Owing to the increasing per capita yogurt consumption, companies are focusing on developing yogurt products with gluten-free and non-GMO claims. Plain yogurts are also available in non-fat, low-fat, and whole-milk variants, as per consumer choice, and can be used in dips, smoothies, and baked foods. Pasteurized milk and yogurt were added to the National School Milk Program in 2021, which supports the demand for these products. The changing lifestyles of consumers and eating habits are boosting the demand for ready-to-use products such as milk powder due to the associated convenience factor. The per capita consumption of milk powder is estimated to increase by 1.14% from 2023 to 2024.

China Dairy Industry Overview

The China Dairy Market is moderately consolidated, with the top five companies occupying 48.34%. The major players in this market are Bright Food (Group) Co. Ltd, China Mengniu Dairy Company Limited, Inner Mongolia Yili Industrial Group Co. Ltd, Nestle SA and Want Want Holdings Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Butter

- 4.2.2 Cheese

- 4.2.3 Milk

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Butter

- 5.1.1.1 By Product Type

- 5.1.1.1.1 Cultured Butter

- 5.1.1.1.2 Uncultured Butter

- 5.1.2 Cheese

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Natural Cheese

- 5.1.2.1.2 Processed Cheese

- 5.1.3 Cream

- 5.1.3.1 By Product Type

- 5.1.3.1.1 Double Cream

- 5.1.3.1.2 Single Cream

- 5.1.3.1.3 Whipping Cream

- 5.1.3.1.4 Others

- 5.1.4 Dairy Desserts

- 5.1.4.1 By Product Type

- 5.1.4.1.1 Cheesecakes

- 5.1.4.1.2 Frozen Desserts

- 5.1.4.1.3 Ice Cream

- 5.1.4.1.4 Mousses

- 5.1.4.1.5 Others

- 5.1.5 Milk

- 5.1.5.1 By Product Type

- 5.1.5.1.1 Condensed milk

- 5.1.5.1.2 Flavored Milk

- 5.1.5.1.3 Fresh Milk

- 5.1.5.1.4 Powdered Milk

- 5.1.5.1.5 UHT Milk

- 5.1.6 Yogurt

- 5.1.6.1 By Product Type

- 5.1.6.1.1 Flavored Yogurt

- 5.1.6.1.2 Unflavored Yogurt

- 5.1.1 Butter

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Bright Food (Group) Co. Ltd

- 6.4.2 China Mengniu Dairy Company Limited

- 6.4.3 Danone SA

- 6.4.4 Fonterra Co-operative Group Limited

- 6.4.5 Inner Mongolia Yili Industrial Group Co. Ltd

- 6.4.6 Junlebao Dairy Group

- 6.4.7 Nestle SA

- 6.4.8 Panda Dairy Group Co. Ltd

- 6.4.9 VV Group Co. Ltd

- 6.4.10 Want Want Holdings Limited

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms