|

市場調査レポート

商品コード

1406979

小麦タンパク質:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Wheat Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小麦タンパク質:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

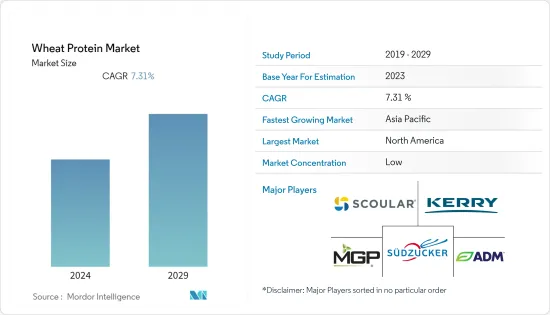

小麦タンパク質の市場規模は、2024年の11億3,000万米ドルから2029年には16億米ドルに成長し、予測期間中のCAGRは7.31%になると予測されています。

主なハイライト

- ビーガン食品に対する需要の高まりが、主に小麦タンパク質分野を牽引しています。牛乳タンパク質は、他のタンパク質の中でも最も一般的に入手可能なタンパク質の1つであり、個人の間で乳糖不耐症の発生率が増加していることから、小麦タンパク質のような代替タンパク質源の需要が増加しています。また、食肉代替品やその他の分野での小麦タンパク質の用途が増加していることも、市場セグメンテーションを後押ししています。市場に参入しているメーカーは革新的な代替肉製品を提供し、市場シェアをさらに伸ばしています。

- 例えば、The Archer-Daniels-Midland Company社は、味、機能、栄養のための原材料とソリューションの中で、革新的な小麦タンパク質濃縮物のシリーズであるNutrianceを提供しています。同社によれば、この製品は85%のタンパク質を供給し、グルタミン含有量が高く、消化性に優れているため、スポーツ栄養市場と高齢者栄養市場の両方に適しています。

- オーストラリア統計局によると、オーストラリアで生産される鶏肉の総額は、2021年の29億3,000万豪ドル(21億9,750万米ドル)から2022年には31億8,000万豪ドル(23億8,500万米ドル)に増加しました。動物またはペットの飼料における小麦タンパク質の利点に関する意識の高まりにより、動物飼料における小麦タンパク質の用途に対する需要が大幅に増加しており、これが小麦タンパク質の需要を促進すると予想されています。さらに、高い栄養価やビタミン・ミネラルの供給源といった利点に加え、動物飼料産業における技術の進歩や天然・有機代替品への需要の高まりが、調査期間中の市場成長をさらに促進すると予想されます。

- さらに、様々なメーカーによる小麦タンパク質原料の技術革新の増加も、世界の小麦タンパク質市場を牽引しています。例えば、2022年2月、MGP Ingredients社は、同社のProTerraシリーズのテクスチャライズドプロテインを製造するために、カンザス州に押出成形工場を新設すると発表しました。

- この1,670万米ドルの施設は、同社のアチソン工場に隣接し、当初は年間最大1,000万ポンドのProTerraを生産する予定です。この新工場は、植物性食肉代替品などの用途に使用されるエンドウ豆と小麦のタンパク質成分で構成されるProTerra製品ラインの需要増加に対応するためのMGP社の支援となります。このような技術革新は、様々なエンドユーザー産業における小麦タンパク質の需要増加と相まって、小麦タンパク質の世界市場を牽引すると期待されています。

小麦タンパク質の市場動向

フィットネス志向と植物性タンパク質の摂取増加

- 人口と福祉の増加に伴い、食品栄養成分としてのタンパク質の需要が急増しています。高タンパク動向は牽引力を増しており、今後も関心を呼び起こすと思われます。

- 多忙なライフスタイル、ヘルシーな包装食品消費の増加、朝食用シリアルの世界の消費の増加、食生活パターンの変化、コンビニエンスストアの増加により、調理が簡単な食事やすぐに食べられる食事に対する需要が高まっており、これが全世界の包装食品メーカー、特に発展途上国における小麦タンパク質原料の需要を牽引しています。このような植物ベースの食事への緩やかな傾斜は、持続可能性の問題、健康意識、倫理的または宗教的見解、環境や動物の権利などのさまざまな要因に大きく関連しています。

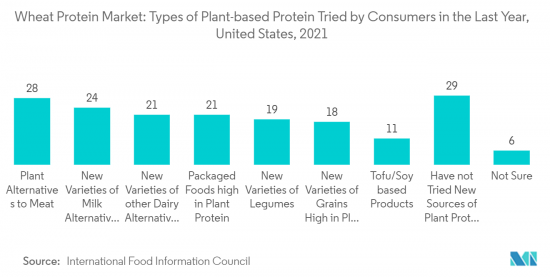

- 国際食品情報評議会(IFIC)が2021年に米国で発表した調査では、回答者のほぼ24%が前年に新しい代用乳を試したことがあると答えました。また、回答者のほぼ21%が、植物性タンパク質を相当量含むパッケージ食品を試したことがあると答えました。加えて、原材料の入手性が高いため小麦タンパク質の入手が容易であることと、タンパク質源として受け入れられていることが市場を牽引しています。

- International Health, Racquet &Sportsclub Associationによると、英国では過去数年間にジムの会員数が増加しています。英国のジム会員数は、2020年の828万人から2021年には957万人に増加します。タンパク質は筋肉の回復や筋肉量の維持に役立つため、フィットネス活動に傾倒する人々はタンパク質をより多く摂取する傾向にあり、この要因は植物由来の製品に対する需要の増加と相まって、予測期間中に調査された市場を牽引すると予想されます。

- さらに、改良された技術により、企業は本物の肉のような有機的特性を持つ革新的な製品を開発し、消費者をターゲットにしています。これらの代用肉は、所望の構造を得るために小麦と他の植物性タンパク質を組み合わせて作られます。新しい組成研究と改良された高水分押出工程が、小麦タンパク質市場の成長に貢献しています。

北米が最大の市場シェアを占める

- 北米は小麦タンパク質市場の主要地域です。小麦タンパク質を含む植物タンパク質の需要は、主にタンパク質機能に対するニーズの高まり、高タンパク質食に対する意識、新しい技術の進歩によってもたらされています。小麦タンパク質やその他の植物性タンパク質は肉の食感を再現できるため、肉代替食品の製造に使用することができ、北米全域のあらゆる飲食品カテゴリーで高い需要があります。

- 小麦タンパク質は小麦や小麦粉に由来するタンパク質で、製粉、ベーカリー製品、パスタ、肉代替食品、朝食用シリアル、ペットフード、水産飼料、牛乳代替食品など様々な用途に使用されます。小麦タンパク質のユニークな機能特性に対する認識の高まりと、あらゆる植物性タンパク質の使用の増加は、予測期間中の市場の大幅な成長を示唆しています。

- さらに、様々なアミノ酸を含有し、満腹感、筋肉修復、体重減少、エネルギーバランスなどの特定の目的を果たす、様々なメーカーによる栄養タンパク質の開拓の増加は、市場に大きな潜在的成長をもたらすと予想されます。米国農務省全米農業統計局が発表したデータによると、2022年の小麦生産量は約2億9,990万ブッシェルで、ノースダコタ州が最も小麦生産量の多い州に挙げられています。

- 2021年にはカンザス州の生産量が最も多く、約3億6,400万ブッシェルでした。このことは、小麦製品の原料が容易に入手できることにつながり、ひいては他の植物性タンパク質の中でも小麦タンパク質の価格が下がることにつながります。小麦タンパク質の価格低下は、同タンパク質の需要に逆影響を与え、市場をさらに牽引します。

小麦タンパク質の産業概要

小麦タンパク質市場は細分化されており、上位企業が主要な市場シェアを占めています。この市場の主要企業は、The Archer-Daniels-Midland Company、Kerry Group PLC、MGP Ingredients, Inc、The Scoular Company、Sudzucker AGなどです。市場の主要企業は、市場での地位を強化するために様々な戦略を用いています。市場の上位企業が一般的に採用している戦略には、イノベーション、パートナーシップ、事業拡大などがあります。さらに、各社は最先端の製造施設を建設するために多額の資金を投資しており、世界中の新市場に進出しています。さらに、その多くの利点のために小麦タンパク質の需要の急増に対応するために、企業は広く小麦タンパク質の生産を増強することに焦点を当てています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- フィットネス志向と植物性タンパク質摂取の増加

- 肉の代替品に対する消費者の志向の高まり

- 市場抑制要因

- グルテン不耐症が市場を阻害する

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 濃縮物

- 単離液

- テクスチャード/加水分解

- エンドユーザー

- 動物飼料

- パーソナルケアおよび化粧品

- 食品・飲料

- ベーカリー

- 朝食用シリアル

- 調味料・ソース

- 菓子類

- 肉・鶏肉・魚介類および代替肉製品

- RTE/RTC食品

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- Archer Daniels Midland Company

- Cargill, Incorporated

- MGP Ingredients, Inc.

- Kerry Group PLC

- Sudzucker AG

- Roquette Freres

- A. Costantino & C. spa

- The Scoular Company

- AMCO Proteins

- Manildra Group

第7章 市場機会と今後の動向

The wheat protein market size is expected to grow from USD 1.13 billion in 2024 to USD 1.6 billion by 2029, at a CAGR of 7.31% during the forecast period.

Key Highlights

- A rise in demand for vegan food products primarily drives the wheat protein segment. Milk protein is one of the most commonly available proteins among others, and the increasing incidences of lactose intolerance among individuals have led to a rise in demand for alternative protein sources like wheat protein. The increasing application areas for wheat protein in the meat substitutes segment and others have also been propelling the market studied. Manufacturers operating in the market offer innovative meat alternative products, further increasing their market share.

- For instance, Archer Daniels Midland Company offers Nutriance, a range of innovative wheat protein concentrates, among its ingredients and solutions for taste, function, and nutrition. As per the company, the product delivers 85% protein and has a high glutamine content, as well as excellent digestibility, making it suitable for both the sports and senior nutrition markets.

- According to the Australian Bureau of Statistics, the gross value of poultry produced in Australia increased from AUD 2.93 billion (USD 2.1975 billion) in the year 2021 to AUD 3.18 billion (USD 2.385 billion) in the year 2022. There has been a significant increase in the demand for wheat protein applications in animal feed due to growing awareness regarding the benefit of wheat protein in animal or pet diets, which is anticipated to drive the demand for wheat protein. Moreover, significant benefits, such as high nutritional value and being a good source of several vitamins and minerals, coupled with technological advancements in the animal feed industry with growing demand for natural and organic substitutes, are expected to further drive market growth during the study period.

- Furthermore, the increasing innovations in wheat protein ingredients by various manufacturers have also been driving the global wheat protein market. For instance, in February 2022, MGP Ingredients announced the construction of a new extrusion plant in Kansas to manufacture its ProTerra line of texturized proteins.

- The USD 16.7 million facility will be located next to the company's Atchison site and will initially produce up to 10 million pounds of ProTerra per year. The new plant will assist MGP in meeting the rising demand for its ProTerra product line, which comprises pea and wheat protein ingredients used in applications such as plant-based meat substitutes. Such innovations, coupled with the rising demand for wheat protein across various end-user industries, are expected to drive the global wheat protein market.

Wheat Protein Market Trends

Inclination Towards Fitness and Increasing Intake of Plant-based Protein

- With the increasing population and welfare, the demand for protein as a food-nutritional component is rising sharply. The high protein trend is gaining traction and will continue to evoke interest in the upcoming years.

- There is a growing demand for easy-to-cook or ready-to-eat meals due to the busy lifestyle, rising healthy packaged food consumption, rising global consumption of breakfast cereal, changing dietary patterns, and an increasing number of convenience stores that are driving the demand for wheat protein ingredients among packaged food manufacturers across the globe, especially in developing countries. This gradual inclination toward a plant-based diet is largely associated with different factors, such as sustainability issues, health awareness, ethical or religious views, and environmental and animal rights.

- In a survey published by the International Food Information Council (IFIC) in the United States in 2021, almost 24% of respondents said they had experimented with new milk substitutes in the previous year. Almost 21% of respondents said they had tried packaged foods with substantial amounts of plant protein. Additionally, the easy availability of wheat protein due to the high availability of raw materials and the acceptance of the protein source have been driving the market.

- According to the International Health, Racquet & Sportsclub Association, the number of people with memberships to gyms in the United Kingdom has witnessed an increase over the past few years. The number of gym members in the United Kingdom increased from 8.28 million in 2020 to 9.57 million in the year 2021. As protein helps in muscle recovery and in maintaining muscle mass, people who are inclined towards fitness activities tend to consume more protein, and this factor, coupled with increasing demand for plant-based products, is expected to drive the market studied over the forecast period.

- Additionally, with the modified technologies, companies are targeting consumers by coming up with innovative products that have organoleptic properties like that of real meat. These meat substitutes are made with a combination of wheat and other plant proteins to attain the desired structure. The new compositional research and modified high-moisture extrusion process are helping the wheat protein market's growth.

North America Holds the Largest Market Share

- North America is the dominant region for the wheat protein market. The demand for plant proteins, including wheat protein, is primarily driven by the rising need for protein functions, awareness of diets that are high in protein, and new technical advancements. As wheat protein and other plant proteins can replicate the texture of meat, they can be used in the manufacturing of meat substitutes and are in high demand across all food and beverage categories across North America.

- Wheat proteins are proteins derived from wheat or wheat flour used in various applications, including flour milling, bakery products, pasta, meat replacer, breakfast cereal, pet food, aquafeed, milk replacer, and more. The increasing awareness of wheat protein's unique functional properties and the growing use of all vegetable proteins augurs significant market growth over the forecast period.

- Additionally, a rise in the development of dietary proteins by different manufacturers that contain a variety of amino acids and serve certain purposes, such as satiety, muscle repair, weight loss, and energy balance, is anticipated to present the market with tremendous potential growth. As per the data published by the US Department of Agriculture National Agricultural Statistics Service, with around 299.9 million bushels of wheat produced in 2022, North Dakota was listed as the state with the highest wheat production.

- In 2021, Kansas produced the most, at around 364 million bushels. This leads to the easy availability of raw materials for wheat products, which in turn leads to a reduction of prices of wheat protein among the rest of the plant-based proteins. The lower prices of wheat protein inversely affect the demand for the same, further driving the market.

Wheat Protein Industry Overview

The wheat protein market is fragmented, with the top companies owning the major market shares. The major players in this market include The Archer-Daniels-Midland Company, Kerry Group PLC, MGP Ingredients, Inc., The Scoular Company, and Sudzucker AG. The top players in the market use various strategies to strengthen their position in the market. Some of the commonly adopted strategies by the top players in the market include innovations, partnerships, and expansions. Furthermore, the companies have been investing a substantial amount of money to build cutting-edge manufacturing facilities and are expanding to new markets across the globe. Moreover, to cater to the surging demand for wheat protein owing to its numerous benefits, the players are widely focusing on augmenting their production of wheat protein.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Inclination Towards Fitness and Increasing Intake of Plant-based Protein

- 4.1.2 Increase in Consumer Inclination Towards Meat Substitutes

- 4.2 Market Restraints

- 4.2.1 Gluten-Intolerance Among the Population Hindering the Market

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Concentrates

- 5.1.2 Isolates

- 5.1.3 Textured/Hydrolyzed

- 5.2 End-User

- 5.2.1 Animal Feed

- 5.2.2 Personal Care and Cosmetics

- 5.2.3 Food and Beverages

- 5.2.3.1 Bakery

- 5.2.3.2 Breakfast Cereals

- 5.2.3.3 Condiments/Sauces

- 5.2.3.4 Confectionery

- 5.2.3.5 Meat/Poultry/Seafood and Meat Alternative Products

- 5.2.3.6 RTE/RTC Food Products

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategies Adopted by Leading Players

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Archer Daniels Midland Company

- 6.3.2 Cargill, Incorporated

- 6.3.3 MGP Ingredients, Inc.

- 6.3.4 Kerry Group PLC

- 6.3.5 Sudzucker AG

- 6.3.6 Roquette Freres

- 6.3.7 A. Costantino & C. spa

- 6.3.8 The Scoular Company

- 6.3.9 AMCO Proteins

- 6.3.10 Manildra Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS