|

|

市場調査レポート

商品コード

1406969

日本のタンパク質:市場シェア分析、産業動向と統計、成長予測、2024年~2029年Japan Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のタンパク質:市場シェア分析、産業動向と統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

日本のタンパク質市場規模は、2024年の5億2,568万米ドルから2029年には5億8,396万米ドルに成長し、予測期間(2024年~2029年)のCAGRは2.13%と予測されます。

主なハイライト

- 日本におけるタンパク質需要は成長を遂げており、この傾向は食生活の嗜好の変化とタンパク質摂取に関する消費者の意識の高まりが主な原因となって、今後数年間も続くか、あるいはさらに加速すると予想されます。日本人の食生活は進化しており、より欧米化した食生活への傾斜が強まっています。これには、肉、乳製品、卵、その他の植物性蛋白源など、蛋白質を多く含む食品の消費量の増加が含まれます。

- さらに、都市化によって生活様式や食生活パターンが変化する傾向があり、その結果、タンパク質が豊富なスナックや調理済みの食事を含む簡便食品の需要が高まることが多いです。こうした動向は、肉タンパク質、植物性タンパク質、微生物性タンパク質など、さまざまな種類のタンパク質に対する需要の伸びを促しています。こうした傾向は、国内のメーカーが加工時に高タンパク質を製品に組み込むことを後押ししています。

- また、日本ではベジタリアンの人口が急増しています。「隠れベジタリアン」(ベジタリアンであることを隠している人々)、「ゆるベジタリアン」(フレキシタリアン)、週に1回野菜を食べる人々です。これらの人々は、動物性タンパク質を補うために、大豆タンパク質やエンドウ豆タンパク質のような植物性タンパク質を毎日の食事で摂取しています。

- さらに、スキンケアやヘアケアを含むパーソナルケアの維持に対する消費者の傾倒は、様々なパーソナルケア製品メーカーやサプリメントメーカーによる、コラーゲン、カルミン、ゼラチンのような動物性タンパク質成分の需要をさらに押し上げています。このような原料を使用した製品を開発し、需要の増加により生産量を増やしているメーカーは、さらに使用量を増やすと予想されるため、国内での動物性タンパク質の需要が増加しています。

- 例えば、大塚製薬は2023年3月、女性の健康と美容をサポートするサプリメントブランド「EQUELLE(エクエル)」の新バージョン「EQUELLE gelee(エクエルジュレ)」を発売しました。コラーゲンやカルシウムを配合し、肌や髪の健康をサポートします。

- さらに、同国の大手企業は、植物性・動物性タンパク質生産に革命をもたらす革新的技術を開発する様々な企業への投資に注力しています。このような市場開拓は、同国における様々なタンパク質原料の需要をさらに押し上げ、最終的に市場の成長を促進すると予想されます。

日本のタンパク質市場動向

肉類似物に対する需要の増加

- 日本の消費者の蛋白質摂取量の増加と代替蛋白質オプションのブームにより、植物性蛋白質が引き続き成長源となっています。消費者は、動物性タンパク質の調達と生産に関連する環境への懸念と、植物や微生物などの持続可能なタンパク質源への切り替えの必要性をますます認識するようになっています。このような要因が、国内における様々な植物性タンパク質源の入手可能性と相まって、市場の成長を促進しています。

- 例えば、国内で入手可能な様々な植物性タンパク質源には、大豆タンパク質やエンドウ豆タンパク質などがあります。さらに、大豆に対する消費者の親しみやすさも、植物性蛋白源が日本で受け入れられている理由の一つです。例えば、豆腐や豆乳は長い間、変化に富んだ日本人の食生活の一部として食べられてきました。肉などの他の大豆ベースの代替食品は、この既存のパターンにうまく適合しています。

- さらに、このような要因により、いくつかのベンチャー企業がその可能性を開拓するために代替タンパク質の分野に投資するようになり、最終的に市場の成長につながった。食感大豆たん白は理想的な肉の代用品であり、菜食主義者や柔軟志向の消費者の間で高い支持を得ています。この現象は、ナゲット、ハンバーガーパティ、ソーセージ、クランブルのような偽肉や菜食主義者の肉製品のポートフォリオに肉のような食感と風味のプロファイルを提供する食品メーカーを支援し、タンパク質代替物市場の成長を増強しました。

- 各社は、日本の肉食に慣れ親しんだ消費者をターゲットに、植物性ハンバーグ、豆腐、餃子など、植物性タンパク質ベースの新しい肉製品で革新を図っています。

- 例えば、2023年1月、植物性原料の世界的リーダーであり、植物性タンパク質のパイオニアであるRoquette社は、株式会社ダイズへの出資を発表しました。この日本のフードテック新興企業は、植物性食品の食感、風味、栄養プロファイルを向上させるために、植物種子の発芽と押出工程を組み合わせた画期的な技術を開発しました。

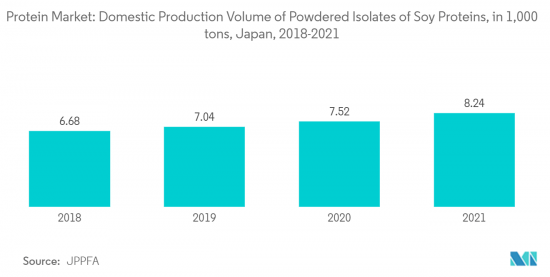

- さらに、植物性原料の需要増加に伴い、日本では様々な植物性タンパク質の生産も増加しており、十分な供給によって市場の成長を支えることが期待されています。例えば、Journal of Educational Development:によると、2021年の大豆たん白分離粉末の国内生産量は約8,240トンで、前年の7,520トンから増加しました。このような新興諸国の市場開拓は、予測期間中の市場の成長をさらに押し上げると予想されます。

食品・飲料が最大シェアを占める

- 日本は多様で伝統的な料理で知られ、その食生活には通常、植物性食品と動物性食品の両方が混在しています。しかし、食生活の嗜好の変化や健康意識の高まりなど様々な要因から、消費者が摂取する様々な飲食品を通じたタンパク質含有量の増加に関する意識が近年国内で高まっています。こうした要因が、同国の飲食品セグメントの市場を牽引しています。

- 2021年の日本市場では、植物由来の肉・乳製品が増加し、定期的に新製品が発売されました。国内企業は新たな代替タンパク質製品を発売しました。ほぼすべての大手食肉加工業者が植物性代替肉を発売しているほか、大手植物油粉砕業者や大豆系加工業者、乳製品加工業者、冷凍食品メーカー、健康食品・飲料メーカー、さらには多くの大手小売チェーンや大手カフェ・ハンバーガーチェーンの製品も発売されています。

- 従って、これらの要因は、同国におけるタンパク質代替原料の応用を増加させると予想されます。さらに、日本で利用されている植物性蛋白質は主に大豆蛋白質と小麦蛋白質を指し、これらは加工食品の原料として添加されたり、テクスチャードベジタブルタンパク質という形で肉の代用品として使用されたりします。

- これに伴い、企業はメーカーや消費者の要望に沿ったタンパク質原料の提供にも力を入れています。例えば、ADMは、様々な用途で栄養や機能性を提供できると主張する分離大豆蛋白を日本で提供しています。

- 同社によると、同社の分離大豆たん白は、飲食品から押し出しスナックやシリアル、さらにバー、乳製品代替品、肉および肉代替品、ソース、グレイビーソース、スープ、さらには飲食品やペットフードまで、幅広い用途に使用できます。こうした発展は、日本の飲食品業界からの蛋白質原料の需要をさらに押し上げ、ひいては市場の成長を牽引するものと予想されます。

日本のタンパク質産業概要

日本のタンパク質市場は断片化されており、さまざまな企業が需要に応えるために市場に参入しています。この市場の主要企業は、アーチャー・ダニエルズ・ミッドランド・カンパニー、ラクト・ジャパン、森永乳業、新田ゼラチン、ダーリング・イングリーディエンツです。その他にも、いくつかの中小企業や国際的な企業が、優位に立ち、需要の増加に対応するために、国内でタンパク質原料の製造と販売に携わっています。大手企業は、より多くのメーカーを惹きつけるため、グルテンフリーやクリーンラベルを謳ったオーガニック・タンパク質原料の提供に注力しています。さらに、各社は競争優位性を得るために、生産能力の拡大、戦略的パートナーシップ、製品ポートフォリオの拡大、M&Aに取り組んでいます。主要企業は生産技術の革新に積極的に取り組み、工業用に理想的な植物性タンパク質を提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 日本人の健康・フィットネス意識の高まり

- 食肉類似物に対する需要の増加

- 市場抑制要因

- 高い生産コストと限られた生産能力

- 業界の魅力 - ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 出典

- 動物性

- カゼインとカゼイネート

- コラーゲン

- 卵タンパク質

- ゼラチン

- 昆虫タンパク質

- ミルクタンパク質

- ホエイタンパク質

- その他の動物性タンパク質

- 微生物

- 藻類タンパク質

- マイコタンパク質

- 植物性

- 麻タンパク質

- エンドウ豆タンパク質

- ジャガイモタンパク質

- 米タンパク質

- 大豆タンパク質

- 小麦タンパク質

- その他の植物性タンパク質

- 動物性

- エンドユーザー

- 動物飼料

- パーソナルケアと化粧品

- 食品・飲料

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料・ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- サプリメント

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第6章 競合情勢

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- Archer Daniels Midland Company

- Arla Foods AMBA

- Bunge Limited

- Fuji Oil Holdings Inc.

- Darling Ingredients Inc.

- International Flavors & Fragrances Inc.

- Lacto Japan Co., Ltd.

- Morinaga Milk Industry Co., Ltd.

- Nagata Group Holdings, ltd.

- Nitta Gelatin, Inc.

第7章 市場機会と今後の動向

The Japan protein market size is expected to grow from USD 525.68 million in 2024 to USD 583.96 million by 2029, at a CAGR of 2.13% during the forecast period (2024-2029).

Key Highlights

- Protein demand in Japan is experiencing growth, and it is expected that this trend will continue or even accelerate in the following years, majorly due to changing dietary preferences and growing consumer awareness regarding protein intake. Japanese dietary habits have been evolving, with an increasing inclination towards a more Westernized diet. This includes a higher consumption of protein-rich foods like meat, dairy, eggs, and other plant protein sources.

- Additionally, urbanization tends to lead to changes in lifestyle and dietary patterns, often resulting in a higher demand for convenience foods, including protein-rich snacks and ready-to-eat meals. Such trends have been driving the growth in the demand for different types of protein, including meat protein, plant and microbial protein. They are driving manufacturers in the country to incorporate high protein into their products while processing.

- Also, Japan has been witnessing a surge in several vegetarian populations. This population can be divided into 3 types based on their consumption pattern: 'hidden veggies' (those who hide their vegetarianism),' 'yuruveggie' (flexitarian), and eating veggies once a week. These population groups consume plant-based proteins like soy protein and pea protein in their daily diet to compensate for animal proteins.

- Moreover, consumer's inclination towards the maintenance of personal care, including skincare and haircare, has further boosted the demand for animal-based protein ingredients like collagen, carmine, and gelatin from various personal care products manufacturers and supplement manufacturers. Manufacturers developing products with such ingredients and raising their production owing to the increasing demand are even expected to increase the usage, thus the demand for animal proteins in the country.

- For instance, in March 2023, Otsuka Pharmaceutical Co., Ltd. (Otsuka) launched a new version of EQUELLE gelee, an extension of the EQUELLE brand of supplements supporting women's health and beauty. The company claimed that its supplements include collagen and calcium that support skin and hair health.

- Furthermore, major players in the country are focused on investing in various companies that develop innovative technologies that aid in revolutionizing plant and animal-based protein production. Such developments are expected to further boost the demand for various protein ingredients in the country, which eventually drives the market's growth.

Japan Protein Market Trends

Increasing Demand for Meat Analogues

- Plant protein remained the growing source due to the Japanese consumers' rising protein intake and a boom in alternative protein options. Consumers are increasingly becoming aware of environmental concerns associated with the procurement and production of animal protein and their need to switch to sustainable protein sources, such as plant and microbial. Such factors, coupled with the availability of different plant-based protein sources in the country, are driving the growth of the market.

- For instance, various plant protein sources available in the country include soy protein and pea protein, among others. Additionally, consumers' familiarity with soy is one reason why plant-based protein sources have been accepted in Japan. For instance, tofu and soymilk have long been eaten as part of the varied Japanese diet. Other soy-based alternatives, such as meat, fit neatly into this existing pattern.

- Moreover, such factors have resulted in several ventures investing in alternative protein space to tap the potential, which led to the increasing growth of the market eventually. Textured soy protein is an ideal meat substitute and is gaining higher traction among vegan and flexitarian consumers. This phenomenon augmented the growth of the protein alternatives market, which helps food manufacturers provide meat-like texture and flavor profiles to their portfolio of faux meat or vegan meat products such as nuggets, burger patties, sausages, and crumbles.

- Companies are innovating with new plant protein-based meat offerings, including plant-based hamburgers, tofu, and gyoza dumplings, among others, to target consumers who are accustomed to Japan's meat-rich diet.

- For instance, in January 2023, Roquette, a global leader in plant-based ingredients and a pioneer of plant proteins, announced its investment in DAIZ Inc. This Japanese food tech startup has developed breakthrough technology utilizing the germination of plant seeds combined with an extrusion process to enhance the texture, flavor, and nutritional profile of plant-based foods.

- Furthermore, with the increasing demand for plant-based ingredients, the production of various plant proteins is also increasing in Japan, which is expected to support the market's growth by providing enough supply. For instance, according to the Journal of Educational Development: Foundations and Applications in Japan, in 2021, the domestic production volume of powdered isolates of soy proteins in Japan amounted to around 8.24 thousand tons, which increased from 7.52 thousand tons when compared to the previous year. Such developments happening in the country are further expected to boost the market's growth during the forecast period.

Food and Beverages Accounts for the Largest Share

- Japan is known for its diverse and traditional cuisine, and its diet typically includes a mix of both plant-based and animal-based foods. However, the awareness regarding the increased intake of protein content through various foods and beverages consumed by consumers has been rising in the country in recent years due to various factors such as changing dietary preferences and increasing health awareness. These factors are driving the market of the food and beverages segment in the country.

- In the year 2021, there was an increase in plant-based meat and dairy products in the Japanese market, with new launches regularly. Domestic companies launched new alternative protein products. Nearly all major meat processors have released a plant-based meat alternative, as well as products from major plant oil crushers and soy-based processors, dairy processors, frozen food manufacturers, health food & drink manufacturers, as well as many major retail chains and major cafe and hamburger chains.

- Therefore, factors such as these are expected to increase the application of protein alternative ingredients in the country. Moreover, vegetable proteins utilized in Japan refer mainly to soy and wheat proteins, which can be added as an ingredient to processed foods or used as a meat substitute in the form of textured vegetable proteins.

- In line with this, players are also focused on offering protein ingredients that align with the manufacturers and the consumers' demands. For instance, ADM offers soy protein isolates in Japan that it claims can deliver nutrition and/or functionality in a variety of applications.

- According to the company, its soy protein isolates can be used in a long list of applications from beverages to extruded snacks and cereals, plus bars, dairy alternatives, meat and meat alternatives, sauces, gravies, and soups, and even feed & pet food. Such developments are expected to further boost the demand for protein ingredients from the food and beverages industries in the country, which eventually drives the market's growth.

Japan Protein Industry Overview

The Japan protein market is fragmented, with different players participating in the market to cater to the demand. The major players in this market are Archer Daniels Midland Company, Lacto Japan Co., Ltd., Morinaga Milk Industry Co., Ltd., Nitta Gelatin, Inc., and Darling Ingredients Inc. Several other small and international players are involved in the manufacturing and distribution of protein ingredients in the country to gain an advantage and cater to the growing demand. Major players are focused on offering organic protein ingredients with gluten-free and clean-label claims to attract more manufacturers. Furthermore, companies engage in capacity expansions, strategic partnerships, product portfolio expansions, and mergers & acquisitions to gain a competitive edge. Key players have been actively innovating production technologies and delivering ideal plant protein for industrial use.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Health and Fitness Consciousness Among Japanese

- 4.1.2 Increasing Demand for Meat Analogues

- 4.2 Market Restraints

- 4.2.1 Higher Production Costs and Limited Capacities

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

5 Market Segmentation

- 5.1 Source

- 5.1.1 Animal

- 5.1.1.1 Casein and Caseinates

- 5.1.1.2 Collagen

- 5.1.1.3 Egg Protein

- 5.1.1.4 Gelatin

- 5.1.1.5 Insect Protein

- 5.1.1.6 Milk Protein

- 5.1.1.7 Whey Protein

- 5.1.1.8 Other Animal Protein

- 5.1.2 Microbial

- 5.1.2.1 Algae Protein

- 5.1.2.2 Mycoprotein

- 5.1.3 Plant

- 5.1.3.1 Hemp Protein

- 5.1.3.2 Pea Protein

- 5.1.3.3 Potato Protein

- 5.1.3.4 Rice Protein

- 5.1.3.5 Soy Protein

- 5.1.3.6 Wheat Protein

- 5.1.3.7 Other Plant Protein

- 5.1.1 Animal

- 5.2 End-User

- 5.2.1 Animal Feed

- 5.2.2 Personal Care and Cosmetics

- 5.2.3 Food and Beverages

- 5.2.3.1 Bakery

- 5.2.3.2 Beverages

- 5.2.3.3 Breakfast Cereals

- 5.2.3.4 Condiments/Sauces

- 5.2.3.5 Confectionery

- 5.2.3.6 Dairy and Dairy Alternative Products

- 5.2.3.7 Meat/Poultry/Seafood and Meat Alternative Products

- 5.2.3.8 RTE/RTC Food Products

- 5.2.3.9 Snacks

- 5.2.4 Supplements

- 5.2.4.1 Baby Food and Infant Formula

- 5.2.4.2 Elderly Nutrition and Medical Nutrition

- 5.2.4.3 Sport/Performance Nutrition

6 Competitive Landscape

- 6.1 Strategies Adopted by Leading Players

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Archer Daniels Midland Company

- 6.3.2 Arla Foods AMBA

- 6.3.3 Bunge Limited

- 6.3.4 Fuji Oil Holdings Inc.

- 6.3.5 Darling Ingredients Inc.

- 6.3.6 International Flavors & Fragrances Inc.

- 6.3.7 Lacto Japan Co., Ltd.

- 6.3.8 Morinaga Milk Industry Co., Ltd.

- 6.3.9 Nagata Group Holdings, ltd.

- 6.3.10 Nitta Gelatin, Inc.