|

市場調査レポート

商品コード

1684605

食品産業用熱処理機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Food Industry Heat Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 食品産業用熱処理機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月08日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

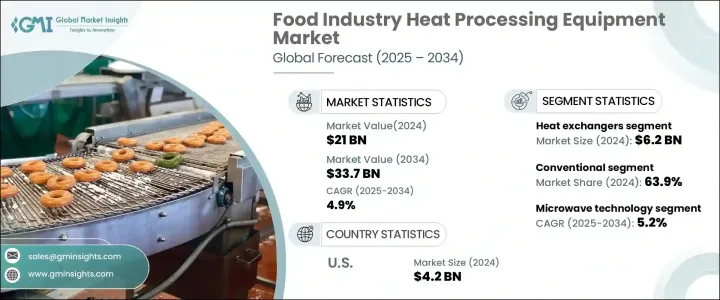

世界の食品産業用熱処理機器市場は2024年に210億米ドルと評価され、2025年から2034年にかけてCAGR4.9%の安定した成長を遂げる見込みです。

この成長の原動力となっているのは、世界人口の増加と消費者のライフスタイルの変化であり、これが調理済み食品や加工食品の需要を促進しています。消費者が利便性、保存期間の延長、安定した品質を優先する中、食品メーカーにとって高度な熱処理機器の採用が不可欠となっています。これらのシステムは生産効率を高めるだけでなく、厳格な食品安全基準や持続可能性の目標への準拠を確実にします。

マイクロ波や誘導システムなどの熱処理技術の進歩は、より高い精度とエネルギー効率を提供することで、市場に革命をもたらしています。これらの技術革新は、エネルギー消費を削減し、食品廃棄物を最小限に抑えるという世界の取り組みと一致しており、製造業者の間で好ましい選択となっています。国際食品保護協会(IAFP)によると、エネルギー効率の高いソリューションと厳格な食品安全要件を重視する規制の枠組みが、最先端機器の採用をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 210億米ドル |

| 予測金額 | 337億米ドル |

| CAGR | 4.9% |

熱交換器分野は2024年に62億米ドルに達し、2034年までCAGR5.2%で成長すると予測されます。熱交換器は低温殺菌、滅菌、調理などの用途で非常に効率的であり、乳製品や飲料など温度に敏感な製品の処理に不可欠です。エネルギー効率を促進しながら正確な温度制御を行うその能力は、業界における重要なコンポーネントとしての地位を確固たるものにしています。国際食品工業供給業者協会(IAFIS)のデータでは、熱交換器の市場シェアが大きく、その信頼性と操作上の利点が原動力となっていることが強調されています。

熱技術タイプ別では、従来型システムが2024年の市場を独占し、63.9%のシェアを獲得しました。ガスや電気ベースの加熱を含むこれらの技術は、様々な食品加工業務における入手可能性、費用対効果、汎用性により、引き続き広く採用されています。一方、マイクロ波技術は、2034年までCAGR5.2%で成長すると予想され、業界で急速に牽引力を増しています。その操作効率と迅速な処理能力で知られるマイクロ波加熱は、熱処理で支配的な力を確立しつつあります。

食品産業用熱処理機器の米国市場は、2024年に42億米ドルを生み出し、2034年まで5%のCAGRで成長すると予測されています。同国の広範な食品生産能力と技術の進歩がこの成長を後押ししています。加工食品に対する需要の高まりは、エネルギー効率の高いソリューションへの関心の高まりと相まって、この地域の市場拡大に大きく寄与しています。食品加工サプライヤー協会(FPSA)の洞察は、米国市場が継続的なイノベーションと持続可能性に重点を置いていることを強調し、高度な熱処理機器の採用における世界的リーダーとしての位置付けを明確にしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測パラメータ

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- 小売業者

- サプライヤーの状況

- 利益率分析

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 加工食品と調理済み食品の需要の高まり

- 熱処理機器の技術的進歩

- エネルギー効率と持続可能性への関心の高まり

- 食品の安全性と品質基準の高まり

- 業界の潜在的リスク・課題

- 高い初期投資コスト

- 複雑なメンテナンスと運用要件

- 成長促進要因

- 技術的展望

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 熱交換器

- 殺菌・滅菌装置

- 蒸発器

- 脱水装置

- フライヤー

- オーブン

- その他(ブランチャー、ロースターなど)

第6章 市場推計・予測:オペレーション別、2021年~2034年

- 主要動向

- 手動

- 半自動

- 全自動

第7章 市場推計・予測:熱技術別、2021年~2034年

- 主要動向

- 従来型(ガス、電気)

- 赤外線

- マイクロ波

- 誘導

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- ベーカリー、菓子類(パン、ケーキ)

- 肉、鶏肉、魚介類

- 乳製品(牛乳、チーズ)

- 果物・野菜

- 飲料(ジュース、ソフトドリンク)

- スナック(チップス、ナッツ)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Alfa Laval

- Barry-Wehmiller Companies, Inc.

- Bühler Group

- FMT Food Machinery &Technology

- GEA Group

- Heat and Control, Inc.

- IDMC Limited

- JBT Corporation

- Krones AG

- Marel

- Scherjon Dairy Equipment

- SPX FLOW

- Tetra Pak

- Thermo Fisher Scientific

- TSC Food Processing Equipment

The Global Food Industry Heat Processing Equipment Market, valued at USD 21 billion in 2024, is set to grow at a steady CAGR of 4.9% between 2025 and 2034. This growth is fueled by the increasing global population and changing consumer lifestyles, which are driving demand for ready-to-eat and processed food products. As consumers prioritize convenience, extended shelf life, and consistent quality, the adoption of advanced heat processing equipment is becoming essential for food manufacturers. These systems not only enhance production efficiency but also ensure compliance with stringent food safety standards and sustainability goals.

Advancements in heat processing technologies, such as microwave and induction systems, are revolutionizing the market by offering greater precision and energy efficiency. These innovations align with global efforts to reduce energy consumption and minimize food waste, making them a preferred choice among manufacturers. According to the International Association for Food Protection (IAFP), regulatory frameworks emphasizing energy-efficient solutions and strict food safety requirements are further encouraging the adoption of cutting-edge equipment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21 Billion |

| Forecast Value | $33.7 Billion |

| CAGR | 4.9% |

The heat exchangers segment reached USD 6.2 billion in 2024 and is forecast to grow at a CAGR of 5.2% through 2034. Heat exchangers are highly efficient in applications like pasteurization, sterilization, and cooking, making them indispensable for processing temperature-sensitive products such as dairy and beverages. Their ability to provide precise temperature control while promoting energy efficiency has solidified their position as a critical component in the industry. Data from the International Association for Food Industry Suppliers (IAFIS) highlights the significant market share of heat exchangers, driven by their reliability and operational benefits.

In terms of heat technology types, conventional systems dominated the market in 2024, capturing a 63.9% share. These technologies, including gas and electricity-based heating, remain widely adopted due to their availability, cost-effectiveness, and versatility across various food processing operations. Meanwhile, microwave technology is expected to grow at a CAGR of 5.2% through 2034, rapidly gaining traction in the industry. Known for its operational efficiency and quick processing capabilities, microwave heating is establishing itself as a dominant force in heat processing.

The U.S. market for food industry heat processing equipment generated USD 4.2 billion in 2024 and is anticipated to grow at a 5% CAGR through 2034. The country's extensive food production capacity, combined with technological advancements, is driving this growth. Rising demand for processed foods, coupled with a growing focus on energy-efficient solutions, significantly contributes to market expansion in the region. Insights from the Food Processing Suppliers Association (FPSA) underscore the U.S. market's emphasis on continuous innovation and sustainability, positioning it as a global leader in the adoption of advanced heat processing equipment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for processed and ready-to-eat foods

- 3.6.1.2 Technological advancements in heat processing equipment

- 3.6.1.3 Increasing focus on energy efficiency and sustainability

- 3.6.1.4 Growing food safety and quality standards

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment costs

- 3.6.2.2 Complex maintenance and operational requirements

- 3.6.1 Growth drivers

- 3.7 Technological landscape

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Heat Exchangers

- 5.3 Pasteurizers & Sterilizers

- 5.4 Evaporators

- 5.5 Dehydration Equipment

- 5.6 Fryers

- 5.7 Ovens

- 5.8 Others (blanchers, roasters, etc.)

Chapter 6 Market Estimates and Forecast, By Operation, 2021 – 2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Fully automatic

Chapter 7 Market Estimates and Forecast, By Heat Technology, 2021 – 2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Conventional (gas, electricity).

- 7.3 Infrared

- 7.4 Microwave

- 7.5 Induction

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Bakery and confectionery (bread, cakes).

- 8.3 Meat, poultry, and seafood.

- 8.4 Dairy products (milk, cheese).

- 8.5 Fruits and vegetables.

- 8.6 Beverages (juices, soft drinks).

- 8.7 Snacks (chips, nuts).

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Alfa Laval

- 11.2 Barry-Wehmiller Companies, Inc.

- 11.3 Bühler Group

- 11.4 FMT Food Machinery & Technology

- 11.5 GEA Group

- 11.6 Heat and Control, Inc.

- 11.7 IDMC Limited

- 11.8 JBT Corporation

- 11.9 Krones AG

- 11.10 Marel

- 11.11 Scherjon Dairy Equipment

- 11.12 SPX FLOW

- 11.13 Tetra Pak

- 11.14 Thermo Fisher Scientific

- 11.15 TSC Food Processing Equipment