|

市場調査レポート

商品コード

1716708

中古車市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Used Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 中古車市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月03日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

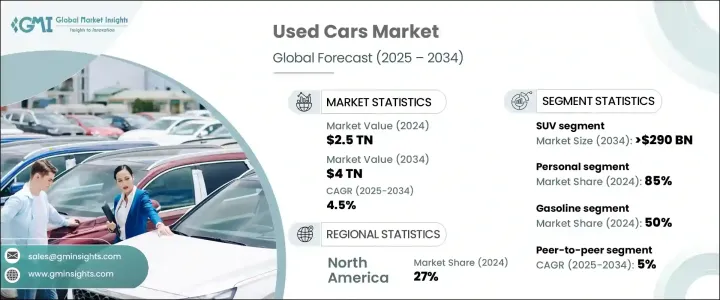

世界の中古車市場は2024年に2兆5,000億米ドルと評価され、2025年から2034年にかけてCAGR 4.5%で成長すると予測されています。

中古車需要の高まりは、新車に比べて手頃な価格であることに起因しており、予算重視の購入者にとって魅力的な選択肢となっています。新車は減価償却が早いため、消費者は比較的新しいモデルを元の価格の数分の一で手に入れることができます。この値ごろ感が、初めて車を購入する人、中間所得層の家族、大きな経済的負担をかけずに車両を拡大したい企業の需要を後押ししています。

経済の不確実性とインフレ圧力は、中古車市場の魅力をさらに高めています。サプライチェーンの混乱、半導体不足、製造経費の増加により新車コストが上昇する中、中古車は品質に妥協することなく、費用対効果の高い代替手段を提供しています。今日の消費者は、これまで以上に価値を重視し、長期的な信頼性とリセールバリューを提供する車を選んでいます。自動車メーカーやディーラーが支援する認定中古車(CPO)プログラムも人気を集めており、延長保証や品質保証を提供することで、消費者の市場に対する信頼感を高めています。さらに、デジタル・プラットフォームの普及により、購入者はオンラインで中古車の調査、比較、購入が容易になり、購入体験全体が合理化されています。AIを活用した価格設定ツールと車両履歴レポートの統合により透明性が確保され、市場の成長をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2兆5,000億米ドル |

| 予測金額 | 4兆ドル |

| CAGR | 4.5% |

多くの高所得者は、ライフスタイルと利便性のために自家用車の所有を好み続けています。経済的な節約だけでなく、特に公共交通機関が必ずしも信頼できるとは限らない都市部では、中古車は移動に対するニーズの高まりに対応しています。低燃費のコンパクトカーから機能満載のSUVや高級車まで、中古車には多様なモデルがあり、消費者の嗜好を満たしています。また、ライドヘイリングやリースプログラムなどのシェアードモビリティサービスの拡大も市場の成長に寄与しています。これらのサービスは定期的に車両を更新し、メンテナンスの行き届いた中古車を安定的に供給しているからです。

市場は、ハッチバック、セダン、SUV、その他など、車種別にセグメント化されています。SUVセグメントは2034年までに2,900億米ドルを創出すると予想され、その強力な体格、広々としたインテリア、市街地走行とオフロード走行の両方に対応する多用途性がその原動力となっています。消費者がSUVを好む理由は、その安全性の高さ、再販価値の高さ、道路状況の変化への適応性にあります。予測不可能な天候パターンが増えていることから、購入者の嗜好は耐久性が高く高性能な車へとシフトしています。コンパクトSUVとミッドサイズSUVは特に人気が高く、市場を再形成し、自動車メーカーの戦略に影響を与えています。

中古車市場は最終用途に基づき、個人向けセグメントと商業向けセグメントに分けられます。2024年には個人向けセグメントが市場シェアの85%を占め、圧倒的なシェアを占めています。中古車は消費者に実用的で費用対効果の高い所有体験を提供し、初期費用の低減、保険料の削減、魅力的な融資オプションへのアクセスを提供します。競合金利と柔軟な分割払いプランが中古車をより利用しやすくし、このセグメントの需要を促進しています。

北米の中古車市場は2024年に5,830億米ドルを生み出し、米国が自動車保有台数でリードしています。アメリカの道路には何百万台もの登録車両が走っているため、中古車の回転率が高く、安定した供給が確保されています。このダイナミックな市場は、継続的な車両入れ替えの恩恵を受けており、多様な中古車セレクションを容易に入手できます。デジタルマーケットプレース、ディーラーネットワーク、CPOプログラムが業界の拡大をさらにサポートし、世界の中古車市場における北米の主要プレーヤーとしての地位を強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- 最終用途

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 価格動向

- 影響要因

- 促進要因

- 手頃な価格とコスト削減

- 可処分所得の増加と都市化

- 新車の減価償却費の高騰

- オンライン・プラットフォームの成長とデジタル化

- 融資やローンオプションの利用可能性

- 業界の潜在的リスク&課題

- 標準化と品質保証の欠如

- 新車販売やリースモデルとの競合激化

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:自動車別、2021年~2034年

- 主要動向

- ハッチバック

- セダン

- SUV

- その他

第6章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

- ハイブリッド

- 電気

- その他

第7章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- ピアツーピア

- フランチャイズ・ディーラー

- 独立系ディーラー

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 個人

- 商業

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alibaba

- Asbury Automotive Group

- AUDI

- AutoNation

- Avis Budget Group

- CarMax

- CARS24

- Carvana

- eBay

- Group 1 Automotive

- Hendrick Automotive Group

- Hertz Global Holdings

- Lithia Motors

- Mahindra First Choice Wheels

- Maruti Suzuki True Value

- Penske Automotive Group

- Scout24 AG

- Sonic Automotive

- TrueCar

- Van Tuyl Group

The Global Used Car Market was valued at USD 2.5 trillion in 2024 and is projected to grow at a CAGR of 4.5% between 2025 and 2034. The rising demand for pre-owned vehicles stems from their affordability compared to new cars, making them an attractive option for budget-conscious buyers. As new vehicles depreciate rapidly, consumers can acquire relatively recent models at a fraction of the original price. This affordability factor drives demand among first-time buyers, middle-income families, and businesses looking to expand their fleets without a substantial financial burden.

Economic uncertainty and inflationary pressures have further strengthened the appeal of the used car market. With the cost of new vehicles rising due to supply chain disruptions, semiconductor shortages, and higher manufacturing expenses, pre-owned cars offer a cost-effective alternative without compromising on quality. Consumers today are more value-conscious than ever, opting for vehicles that provide long-term reliability and resale value. Certified pre-owned (CPO) programs backed by automakers and dealerships are also gaining traction, offering extended warranties and quality assurance, boosting consumer confidence in the market. Additionally, the growing adoption of digital platforms has made it easier for buyers to research, compare, and purchase used cars online, streamlining the entire buying experience. The integration of AI-powered pricing tools and vehicle history reports ensures transparency, further driving the market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Trillion |

| Forecast Value | $4 Trillion |

| CAGR | 4.5% |

Many high-income individuals continue to favor private vehicle ownership for lifestyle and convenience. Beyond financial savings, used cars cater to the increasing need for mobility, especially in urban areas where public transportation may not always be reliable. The wide variety of available pre-owned models meets diverse consumer preferences, from fuel-efficient compact cars to feature-packed SUVs and luxury vehicles. The expansion of shared mobility services, such as ride-hailing and leasing programs, has also contributed to the market's growth, as these services regularly refresh their fleets, supplying a steady stream of well-maintained used cars.

The market is segmented by vehicle type, including hatchbacks, sedans, SUVs, and others. The SUV segment is expected to generate USD 290 billion by 2034, driven by its strong build, spacious interiors, and versatility for both urban and off-road driving. Consumers favor SUVs due to their perceived safety, higher resale value, and adaptability to changing road conditions. With increasingly unpredictable weather patterns, buyers are shifting preferences toward durable and high-performing vehicles. Compact and mid-size SUVs are particularly popular, reshaping the market and influencing automakers' strategies.

Based on end-use, the used car market is divided into personal and commercial segments. The personal segment dominated in 2024, accounting for 85% of the market share. Used cars provide consumers with a practical and cost-effective ownership experience, offering lower initial costs, reduced insurance premiums, and access to attractive financing options. Competitive interest rates and flexible installment plans make pre-owned vehicles more accessible, fueling demand in this segment.

North America Used Car Market generated USD 583 billion in 2024, with the U.S. leading in vehicle ownership. Millions of registered vehicles on American roads create a high turnover, ensuring a steady supply of pre-owned cars. This dynamic market benefits from continuous vehicle replacements, making a diverse selection of used cars readily available. Digital marketplaces, dealership networks, and CPO programs further support industry expansion, reinforcing North America's position as a key player in the global used car market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 End Use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Price trends

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Affordability and cost savings

- 3.6.1.2 Rising disposable income and urbanization

- 3.6.1.3 High depreciation of new cars

- 3.6.1.4 Growth of online platforms and digitalization

- 3.6.1.5 Availability of financing and loan options

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Lack of standardization and quality assurance

- 3.6.2.2 Rising competition from new car sales and leasing models

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hatchback

- 5.3 Sedan

- 5.4 SUV

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Hybrid

- 6.5 Electric

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Peer-to-peer

- 7.3 Franchised dealers

- 7.4 Independent dealers

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alibaba

- 10.2 Asbury Automotive Group

- 10.3 AUDI

- 10.4 AutoNation

- 10.5 Avis Budget Group

- 10.6 CarMax

- 10.7 CARS24

- 10.8 Carvana

- 10.9 eBay

- 10.10 Group 1 Automotive

- 10.11 Hendrick Automotive Group

- 10.12 Hertz Global Holdings

- 10.13 Lithia Motors

- 10.14 Mahindra First Choice Wheels

- 10.15 Maruti Suzuki True Value

- 10.16 Penske Automotive Group

- 10.17 Scout24 AG

- 10.18 Sonic Automotive

- 10.19 TrueCar

- 10.20 Van Tuyl Group