|

|

市場調査レポート

商品コード

1597097

アジア太平洋のデータセンター建設市場:2030年までの予測 - 地域別分析 - 建設タイプ別、ティア基準別、業界別Asia Pacific Data Center Construction Market Forecast to 2030 - Regional Analysis - by Types of Construction, Tier Standards, and Industry Verticals |

||||||

|

|||||||

|

|||||||

| アジア太平洋のデータセンター建設市場:2030年までの予測 - 地域別分析 - 建設タイプ別、ティア基準別、業界別 |

|

出版日: 2024年10月03日

発行: The Insight Partners

ページ情報: 英文 88 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のデータセンター建設市場は、2022年に672億3,634万米ドルとなり、2030年までには1,479億8,747万米ドルに達すると予測され、2022年から2030年までのCAGRは10.4%と推定されます。

ハイパースケーラとコロケーションの導入増加がアジア太平洋のデータセンター建設市場を後押し

ハイパースケールは、多くの場合、弾力性のあるクラウドプラットフォームの形で、膨大なコンピューティング能力を提供する大規模データセンターの一種です。企業はハイパースケールを利用して、広範なアプリケーションやサービスを管理・提供します。ハイパースケーラの目的は、より広い範囲をカバーするために、より優れたレイテンシーを維持しながらサービス提供を拡大し、可用性を向上させることです。ハイパースケーラーは、社内の競合に加え、コロケーション・プロバイダーとの激しい競争にも直面しています。データセンターの容量の37%は、デジタルリアルティ、エクイニクス、サイラスワン、チンデータ、世界スイッチなどのコロケーションプロバイダーが所有し、32%はクラウドサービスプロバイダーとハイパースケーラー、20%は個人所有のデータセンター、11%は通信事業者が所有しています。

さらに、小規模企業にとって、データセンターの建設には莫大な資金が必要となります。これらの企業はデータセンターを建設するための予算や資本支出が限られているため、ROIは比較的低くなります。そのため、こうした企業の多くはコロケーションやクラウドサービスを選択しています。このような企業は多くのストレージスペースを必要としないため、自社でデータセンターを建設することは現実的ではありません。そのため、データの保管はコロケーションやCSPに依存しています。また、データセンター建設に必要な資金以外にも、メンテナンスやサービスなど、その他の費用や労力が負担となります。さらに、コロケーションサービスやハイパースケーラへの需要は、スケールメリットをもたらすため、メガデータセンターの建設増加につながっています。このように、ハイパースケーラとコロケーションの導入が増加していることから、予測期間中、アジア太平洋のデータセンター建設市場の成長に有利な機会が生まれると予想されます。

アジア太平洋のデータセンター建設市場の概要

アジア太平洋は、インターネットユーザー数が最も多い新興経済諸国で構成されています。この要因は、大手ソーシャルメディア・プレイヤーやインターネットベースのサービス・プロバイダーにとって、未開拓のアジア太平洋市場から利益を得る大きな機会となっています。安価なスマートフォンやタブレットが普及し、企業や家庭でのコンピューティング・デバイスの普及が進むにつれ、この地域はインターネット・ベースのサービスを求めるユーザー数の最大の伸びを占めています。このため、インターネットに接続するユーザーの大幅な増加と同地域の良好な経済成長が、企業やクラウド・サービス・プロバイダーがユーザーの近くにサーバーを設置し、待ち時間や反応時間を短縮してデータにアクセスできるようにする要因となっています。このような要因が、アジア太平洋のデータセンター建設市場の成長に寄与しています。

アジア太平洋のデータセンター建設市場の収益と2030年までの予測(金額)

アジア太平洋のデータセンター建設市場のセグメンテーション

アジア太平洋のデータセンター建設市場は、建設タイプ、ティア基準、業界別、国別に区分されます。

建設タイプ別に見ると、アジア太平洋のデータセンター建設市場は、一般建設、電気設計、機械設計に区分されます。2022年には、電気設計セグメントが最大のシェアを占めています。

ティア基準では、アジア太平洋のデータセンター建設市場はティア1・ティア2、ティア3、ティア4に区分されます。2022年にはティア3セグメントが最大のシェアを占めました。

業界別では、アジア太平洋のデータセンター建設市場は、IT・通信、BFSI、政府、教育、製造、小売、運輸、メディア・娯楽、その他に区分されます。2022年にはIT・通信分野が最大のシェアを占めました。

国別に見ると、アジア太平洋のデータセンター建設市場は、オーストラリア、中国、インド、日本、韓国、その他アジア太平洋に分類されます。2022年のアジア太平洋のデータセンター建設市場は中国が独占しました。

Rittal GmbH &Co KG、Schneider Electric SE、DPR Construction Inc、AECOM、Turner Construction Co、Eaton Corp Plc、Nikom InfraSolutions Pvt. Ltdなどがアジア太平洋のデータセンター建設市場で事業を展開する主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋のデータセンター建設市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 アジア太平洋のデータセンター建設市場:主要市場力学

- アジア太平洋のデータセンター建設市場:主要市場力学

- 新しいエッジデータセンターの立ち上げの増加

- IoTサービスの急速な拡大

- データセンター建設活動の急増

- 市場抑制要因

- インフラ整備コストの上昇

- データセンターインフラとその構築の複雑さ

- 市場機会

- ハイパースケーラとコロケーションの導入拡大

- ティア4データセンターの建設増加

- 今後の動向

- グリーンデータセンターの採用増加

- 促進要因と抑制要因の影響

第6章 データセンター建設市場:アジア太平洋市場分析

- アジア太平洋のデータセンター建設市場収益、2022年~2030年

- アジア太平洋のデータセンター建設市場予測分析

第7章 アジア太平洋のデータセンター建設市場分析:建設タイプ別

- 電気工事

- 一般建設

- 機械建設

第8章 アジア太平洋のデータセンター建設市場分析:ティア基準別

- ティア3

- ティア4

- ティア1・ティア2

第9章 アジア太平洋のデータセンター建設市場分析:業界別

- IT・通信

- BFSI

- メディア・エンターテインメント

- 小売

- 製造業

- 政府機関

- 運輸

- その他

第10章 アジア太平洋のデータセンター建設市場:国別分析

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- アジア太平洋のその他諸国

第11章 競合情勢

- ヒートマップ分析:主要企業別

- 企業のポジショニングと集中度

第12章 業界情勢

- 市場イニシアティブ

第13章 企業プロファイル

- Rittal GmbH & Co KG

- Schneider Electric SE

- DPR Construction Inc

- AECOM

- Turner Construction Co

- Eaton Corp Plc

- Nikom InfraSolutions Pvt. Ltd

第14章 付録

List Of Tables

- Table 1. Asia Pacific Data Center Construction Market Segmentation

- Table 2. List of Vendors

- Table 3. Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million) - by Type of Construction

- Table 5. Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million) - by Tier Standard

- Table 6. Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million) - by Industry Vertical

- Table 7. Asia Pacific: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Country

- Table 8. China: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Type Of Construction

- Table 9. China: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Tier Standard

- Table 10. China: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Industry Vertical

- Table 11. Japan: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Type Of Construction

- Table 12. Japan: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Tier Standard

- Table 13. Japan: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Industry Vertical

- Table 14. South Korea: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Type Of Construction

- Table 15. South Korea: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Tier Standard

- Table 16. South Korea: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Industry Vertical

- Table 17. India: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Type Of Construction

- Table 18. India: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Tier Standard

- Table 19. India: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Industry Vertical

- Table 20. Australia: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Type Of Construction

- Table 21. Australia: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Tier Standard

- Table 22. Australia: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Industry Vertical

- Table 23. Rest of APAC: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Type Of Construction

- Table 24. Rest of APAC: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Tier Standard

- Table 25. Rest of APAC: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million) - by Industry Vertical

- Table 26. Heat Map Analysis By Key Players

List Of Figures

- Figure 1. Asia Pacific Data Center Construction Market Segmentation, by Country

- Figure 2. Ecosystem Analysis

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Asia Pacific Data Center Construction Market Revenue (US$ Million), 2022-2030

- Figure 5. Asia Pacific Data Center Construction Market Share (%) - by Type of Construction (2022 and 2030)

- Figure 6. Electrical Construction: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 7. General Construction: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Mechanical Construction: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Asia Pacific Data Center Construction Market Share (%) - by Tier Standard (2022 and 2030)

- Figure 10. Tier 3: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Tier 4: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Tier 1 and Tier 2: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Asia Pacific Data Center Construction Market Share (%) - by Industry Vertical (2022 and 2030)

- Figure 14. IT and telecommunication: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. BFSI: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Media and Entertainment: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Retail: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Manufacturing: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Government: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 20. Transportation: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Others: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Asia Pacific Data Center Construction Market- Revenue by Key Countries 2022 (US$ Million)

- Figure 23. Asia Pacific: Data Center Construction Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 24. China: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million)

- Figure 25. Japan: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million)

- Figure 26. South Korea: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million)

- Figure 27. India: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million)

- Figure 28. Australia: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million)

- Figure 29. Rest of APAC: Data Center Construction Market - Revenue and Forecast to 2030(US$ Million)

- Figure 30. Company Positioning & Concentration

The Asia Pacific data center construction market was valued at US$ 67,236.34 million in 2022 and is expected to reach US$ 1,47,987.47 million by 2030; it is estimated to register at a CAGR of 10.4% from 2022 to 2030.

Increasing Implementation of Hyperscalers and Colocation Boosts Asia Pacific Data Center Construction Market

A hyperscale is a kind of large-scale data center that offers vast computing capabilities, often in the form of an elastic cloud platform. Organizations use them to manage and deliver extensive applications and services. The objective of hyperscalers is to expand their service offerings while maintaining better latency as well as improve availability in order to cover more ground. They face intense competition from colocation providers in addition to internal competitors. 37% of the capacity of data centers is owned by colocation providers such as Digital Realty, Equinix, CyrusOne, Chindata, and Global Switch; 32% by cloud service providers and hyperscalers; 20% by privately owned data centers; and 11% by telecoms.

Moreover, for small enterprises, constructing their data center involves huge capital. Since these enterprises have a limited budget or capital expenditure to construct a data center, the ROI is comparatively low. As a result, most of these enterprises are choosing colocation or cloud services. These companies do not require much storage space, and constructing their own data center is not feasible. Therefore, they depend on colocation or CSPs to store their data. Also, apart from the capital required to build a data center, other expenses and efforts such as maintenance and service become a burden for these companies. Moreover, the demand for colocation services and hyperscalers is leading to the rise in the construction of mega data centers as they offer economies of scale. Thus, the increasing implementation of hyperscalers and colocation is anticipated to create lucrative opportunities for the Asia Pacific data center construction market growth during the forecast period.

Asia Pacific Data Center Construction Market Overview

APAC comprises the majority of developing economies with the largest number of internet users. This factor presents significant opportunities for leading social media players and internet-based service providers to profit from the untapped APAC market. With the proliferation of cheap smartphones and tablets and increasing penetration of computing devices in businesses and households, the region accounts for the largest growing user base seeking internet-based services. Thus, the strong growth of internet-connected users coupled with good economic growth in the region are the factors encouraging the enterprise and cloud service providers to establish servers in proximity to the users, enabling them to access data with reduced latency and reaction time. This factor contributes to the growth of the Asia Pacific data center construction market in the region.

Asia Pacific Data Center Construction Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Data Center Construction Market Segmentation

The Asia Pacific data center construction market is segmented based on types of construction , tier standards , industry verticals , and country.

Based on types of construction, the Asia Pacific data center construction market is segmented into general construction, electrical design, and mechanical design. The electrical design segment held the largest share in 2022.

In terms of tier standards, the Asia Pacific data center construction market is segmented into tier 1 & tier 2, tier 3, and tier 4. The tier 3 segment held the largest share in 2022.

By industry verticals, the Asia Pacific data center construction market is segmented into IT & telecommunication, BFSI, government, education, manufacturing, retail, transportation, media & entertainment, and others. The IT & telecommunication segment held the largest share in 2022.

Based on country, the Asia Pacific data center construction market is categorized into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific data center construction market in 2022.

Rittal GmbH & Co KG, Schneider Electric SE, DPR Construction Inc, AECOM, Turner Construction Co, Eaton Corp Plc, and Nikom InfraSolutions Pvt. Ltd are some of the leading companies operating in the Asia Pacific data center construction market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Data Center Construction Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain

5. Asia Pacific Data Center Construction Market - Key Market Dynamics

- 5.1 Asia Pacific Data Center Construction Market - Key Market Dynamics

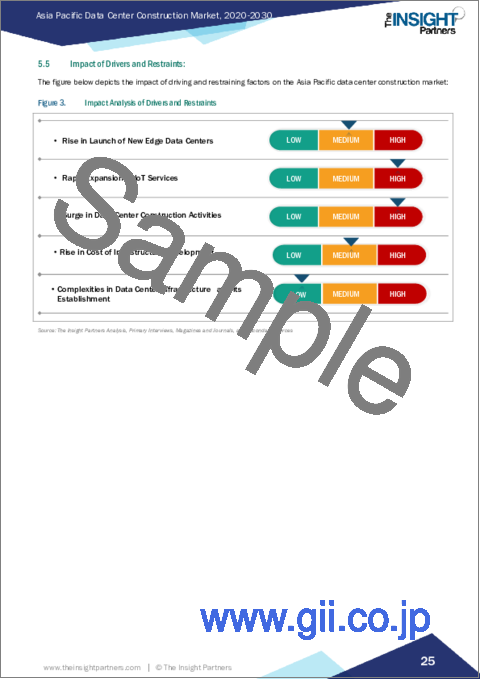

- 5.1.1 Rise in Launch of New Edge Data Centers

- 5.1.2 Rapid Expansion of IoT Services

- 5.1.3 Surge in Data Center Construction Activities

- 5.2 Market Restraints

- 5.2.1 Rise in Cost of Infrastructure Development

- 5.2.2 Complexities in Data Center Infrastructure and its Establishment

- 5.3 Market Opportunities

- 5.3.1 Increasing Implementation of Hyperscalers and Colocation

- 5.3.2 Growing Construction of Tier 4 Data Centers

- 5.4 Future Trends

- 5.4.1 Increasing Adoption of Green Data Centers

- 5.5 Impact of Drivers and Restraints:

6. Data Center Construction Market - Asia Pacific Market Analysis

- 6.1 Asia Pacific Data Center Construction Market Revenue (US$ Million), 2022-2030

- 6.2 Asia Pacific Data Center Construction Market Forecast Analysis

7. Asia Pacific Data Center Construction Market Analysis - by Type of Construction

- 7.1 Electrical Construction

- 7.1.1 Overview

- 7.1.2 Electrical Construction: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 General Construction

- 7.2.1 Overview

- 7.2.2 General Construction: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3 Mechanical Construction

- 7.3.1 Overview

- 7.3.2 Mechanical Construction: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Data Center Construction Market Analysis - by Tier Standard

- 8.1 Tier 3

- 8.1.1 Overview

- 8.1.2 Tier 3: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 Tier 4

- 8.2.1 Overview

- 8.2.2 Tier 4: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3 Tier 1 and Tier 2

- 8.3.1 Overview

- 8.3.2 Tier 1 and Tier 2: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Data Center Construction Market Analysis - by Industry Vertical

- 9.1 IT and telecommunication

- 9.1.1 Overview

- 9.1.2 IT and telecommunication: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.2 BFSI

- 9.2.1 Overview

- 9.2.2 BFSI: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.3 Media and Entertainment

- 9.3.1 Overview

- 9.3.2 Media and Entertainment: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 Retail

- 9.4.1 Overview

- 9.4.2 Retail: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 Manufacturing

- 9.5.1 Overview

- 9.5.2 Manufacturing: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.6 Government

- 9.6.1 Overview

- 9.6.2 Government: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.7 Transportation

- 9.7.1 Overview

- 9.7.2 Transportation: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 9.8 Others

- 9.8.1 Overview

- 9.8.2 Others: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

10. Asia Pacific Data Center Construction Market -Country Analysis

- 10.1 Asia Pacific

- 10.1.1 Asia Pacific: Data Center Construction Market - Revenue and Forecast Analysis - by Country

- 10.1.1.1 Asia Pacific: Data Center Construction Market - Revenue and Forecast Analysis - by Country

- 10.1.1.2 China: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.1 China: Data Center Construction Market Breakdown, by Type Of Construction

- 10.1.1.2.2 China: Data Center Construction Market Breakdown, by Tier Standard

- 10.1.1.2.3 China: Data Center Construction Market Breakdown, by Industry Vertical

- 10.1.1.3 Japan: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.1 Japan: Data Center Construction Market Breakdown, by Type Of Construction

- 10.1.1.3.2 Japan: Data Center Construction Market Breakdown, by Tier Standard

- 10.1.1.3.3 Japan: Data Center Construction Market Breakdown, by Industry Vertical

- 10.1.1.4 South Korea: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.4.1 South Korea: Data Center Construction Market Breakdown, by Type Of Construction

- 10.1.1.4.2 South Korea: Data Center Construction Market Breakdown, by Tier Standard

- 10.1.1.4.3 South Korea: Data Center Construction Market Breakdown, by Industry Vertical

- 10.1.1.5 India: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.5.1 India: Data Center Construction Market Breakdown, by Type Of Construction

- 10.1.1.5.2 India: Data Center Construction Market Breakdown, by Tier Standard

- 10.1.1.5.3 India: Data Center Construction Market Breakdown, by Industry Vertical

- 10.1.1.6 Australia: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.6.1 Australia: Data Center Construction Market Breakdown, by Type Of Construction

- 10.1.1.6.2 Australia: Data Center Construction Market Breakdown, by Tier Standard

- 10.1.1.6.3 Australia: Data Center Construction Market Breakdown, by Industry Vertical

- 10.1.1.7 Rest of APAC: Data Center Construction Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.7.1 Rest of APAC: Data Center Construction Market Breakdown, by Type Of Construction

- 10.1.1.7.2 Rest of APAC: Data Center Construction Market Breakdown, by Tier Standard

- 10.1.1.7.3 Rest of APAC: Data Center Construction Market Breakdown, by Industry Vertical

- 10.1.1 Asia Pacific: Data Center Construction Market - Revenue and Forecast Analysis - by Country

11. Competitive Landscape

- 11.1 Heat Map Analysis by Key Players

- 11.2 Company Positioning & Concentration

12. Industry Landscape

- 12.1 Overview

- 12.2 Market Initiative

13. Company Profiles

- 13.1 Rittal GmbH & Co KG

- 13.1.1 Key Facts

- 13.1.2 Business Description

- 13.1.3 Products and Services

- 13.1.4 Financial Overview

- 13.1.5 SWOT Analysis

- 13.1.6 Key Developments

- 13.2 Schneider Electric SE

- 13.2.1 Key Facts

- 13.2.2 Business Description

- 13.2.3 Products and Services

- 13.2.4 Financial Overview

- 13.2.5 SWOT Analysis

- 13.2.6 Key Developments

- 13.3 DPR Construction Inc

- 13.3.1 Key Facts

- 13.3.2 Business Description

- 13.3.3 Products and Services

- 13.3.4 Financial Overview

- 13.3.5 SWOT Analysis

- 13.3.6 Key Developments

- 13.4 AECOM

- 13.4.1 Key Facts

- 13.4.2 Business Description

- 13.4.3 Products and Services

- 13.4.4 Financial Overview

- 13.4.5 SWOT Analysis

- 13.4.6 Key Developments

- 13.5 Turner Construction Co

- 13.5.1 Key Facts

- 13.5.2 Business Description

- 13.5.3 Products and Services

- 13.5.4 Financial Overview

- 13.5.5 SWOT Analysis

- 13.5.6 Key Developments

- 13.6 Eaton Corp Plc

- 13.6.1 Key Facts

- 13.6.2 Business Description

- 13.6.3 Products and Services

- 13.6.4 Financial Overview

- 13.6.5 SWOT Analysis

- 13.6.6 Key Developments

- 13.7 Nikom InfraSolutions Pvt. Ltd

- 13.7.1 Key Facts

- 13.7.2 Business Description

- 13.7.3 Products and Services

- 13.7.4 Financial Overview

- 13.7.5 SWOT Analysis

- 13.7.6 Key Developments

14. Appendix

- 14.1 About The Insight Partners