|

市場調査レポート

商品コード

1549811

中国データセンター建設:市場シェア分析、産業動向と統計、成長予測(2024年~2030年)China Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国データセンター建設:市場シェア分析、産業動向と統計、成長予測(2024年~2030年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

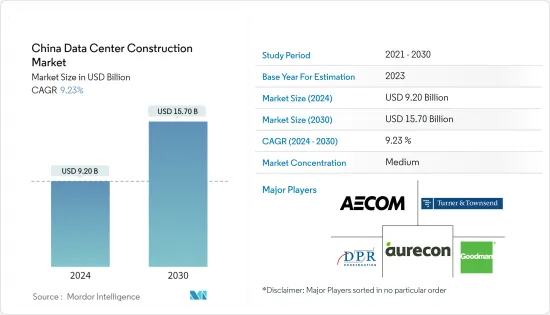

中国のデータセンター建設市場規模は、2024年に92億米ドルと推定され、2030年には157億米ドルに達すると予測され、予測期間(2024~2030年)のCAGRは9.23%で成長する見込みです。

中国には120を超えるデータセンター施設があり、アジア太平洋の大半を占めています。同国では、クラウドコンピューティング、モノのインターネット(IoT)、人工知能(AI)の導入が進んでいるため、より新しいデータセンターへの需要が高まっています。

主要ハイライト

- 同国のIT負荷容量は2030年までに3,400MWを超えると予測され、データセンター用ラックの需要を押し上げています。

- 国内のデータセンター用床面積は、2030年までに1,250万平方フィートに達すると予想されます。

- 国内のラック設置総数は、2030年までに62万個に達します。

- 現在、国内では5つの海底ケーブル・プロジェクトが建設中です。そのひとつがAsia Direct Cable(ADC)で、全長9800キロメートルに及び、中国の中虹角(チュンホムコク)と中国の汕頭(シャントウ)に陸揚げされ、2024年第4四半期に開通する予定です。

中国データセンター建設市場の動向

ティア3が最大のティアタイプ

- ティア3データセンターは、オンサイト支援、電力、冷却の冗長性などの特徴により、最も好まれています。このセグメントは、2023年の約1,300MWから2030年には1,900MWに成長すると予想されています。企業は主に、拡大するビジネスと拡大性のニーズに対応するため、ビジネスクリティカルなデータの保管と処理にこれらのデータセンターを選択します。上海には約110のティア3データセンターがあり、ティア3仕様のデータセンターが37カ所建設中です。

- 上海のティア3データセンター数は国内最多で、市場シェアは28.9%、次いで北京が26.3%、広東省が20.2%となっています。

- 2023年には、GDS Serviceが約70のTier 3認証データセンターを保有し、Chindata Group Holdings Ltdが15のデータセンター施設を、China Telecom Corporation Ltdが10のデータセンター施設を保有しています。

- 建設中の37のデータセンター施設がティア3基準で建設されており、予測期間中に稼動する見込みです。ティア3 DCの建設に携わる主要参入企業は、Princeton Digital Group、GDS Service、Chindata Group Holdingsです。建設は河北地域に集中し、北京、上海、江蘇がこれに続くと予測されています。

- Chindata Group Holdings Ltdは、河北省張家口市のキャンパスに26MWのハイパースケール・プロジェクト「CN23」を発表しました。このプロジェクトは2025年第1四半期に引き渡される予定で、著名な国際的クライアントのために設計され、ティア3の基準を満たすように設計されています。このような事例により、今後数年間は市場成長のための需要がさらに高まると予想されます。

IT・通信セグメントが主要シェアを占める見込み

- 中国政府の14カ年計画では、デジタルサービスを強化する取り組みが推進されています。同計画では、6G、集積回路、AIなどの最先端技術の調査を優先しています。こうした取り組みは、クラウドコンピューティングサービスに対する中国の需要増に対応するために戦略的に調整されています。

- 中国のクラウド市場は、クラウドサービスに対する需要の高まりによって、2021年の300億米ドルから2025年には900億米ドルに急増し、市場規模は3倍になると予測されています。これらのサービスは、SaaS(Software-as-a-Service)、PaaS(Platform-as-a-Service)、IaaS(Infrastructure-as-a-Service)を含み、エンドユーザーが直接利用できます。

- ユーザーは、拡大性の高さからクラウドサービスをますます好むようになっています。これにより、中国の一大ショッピングイベントである「独身の日」のような特定のビジネスニーズに合わせて、ネットワーク、ストレージ、サーバーを調整することができます。ウェブサイトは魅力的なお買い得商品を提供し、大量のトラフィックとトランザクションを引き寄せる。クラウドインフラストラクチャは、この急増をシームレスに管理し、最適なパフォーマンスを保証します。

- クラウドコンピューティングは、追加のコンピューティング電力やデータストレージなどのサービスを、ウェブベースのインフラを通じてクライアントに記載しています。この費用対効果の高いクラウドインフラストラクチャは、データセンターに大規模なサーバーファームと高価なストレージ・セットアップを必要とする従来のシステムとは対照的です。

- さらに、ゲーム、ビデオ制作、モバイルインターネットなどの産業では、クラウドIaaSプラットフォームへの依存度が高まっています。迅速性、費用対効果、適応性を求めて企業がクラウドサービスにシフトする中、クラウドサービスへの需要もそれに伴って急増しています。

- 工業・情報化省のデータによると、IT・通信に関しては、2024年までに中国の5Gネットワークはすべての市町村と村落の90%以上をカバーすることになります。同国は圧倒的な情報通信ネットワークを誇っており、5G基地局の数は384万と、世界全体の60%以上を占めています。このような市場動向は、データセンターへの需要を喚起し、データセンター建設市場を活性化させるものと期待されています。

中国データセンター建設産業概要

中国のデータセンター建設市場は適度に細分化されており、上位5社が市場シェアの大半を占めています。この市場の主要企業は、AECOM、DPR Construction、Aurecon Group Pty Ltd、Goodman Group、Turner & Townsendなどがあります。

- シンガポールに本社を置く先進的なデータセンター・プロバイダーであるSpaceDCは、中国全土で著名なティア4データセンターとネットワーク・プロバイダーであるCentrin Dataと戦略的提携を結びました。この提携は、中国国内におけるCentrin Dataのデータセンターとサービスの販売に共同で取り組むというもので、特に金融産業の強固な顧客層を誇る武漢と昆山の施設にスポットを当てています。これらのデータセンターの総面積は20万6,532.41平方メートルで、最大4万ラックを収容できます。この開発は2段階に分けて計画されており、総容量225MWを目指し、初期段階は70MWに設定されています。同施設は予測期間中に稼動する予定です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場促進要因

- 中国のコンピューティング能力向上への取り組みがデータセンター建設需要を牽引

- デジタル時代の近代化に向けた中国政府の取り組みが、全国的なデータセンター需要の高まりに拍車をかけている

- 市場抑制要因

- データセンターの高い電力消費と排出貢献

- 市場促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 中国の主要データセンター建設統計

- 中国のデータセンター数(2022年と2023年)

- 中国のデータセンター建設中容量(MW)(2024~2029年)

- 中国のデータセンター建設における平均設備投資額と平均運転経費

- データセンターの電力吸収量(MW)(特定都市、中国、2022年と2023年)

- 中国のデータセンターインフラへの設備投資額上位企業

第5章 市場セグメンテーション

- 市場セグメンテーション:インフラ別

- 市場セグメンテーション:電気インフラ別

- 配電ソリューション

- PDU-基本とスマート-計量とスイッチソリューション

- 転送スイッチ

- 静的

- 自動(ATS)

- 開閉装置

- 低圧

- 高圧

- 電力パネルとコンポーネント

- その他のインフラ

- 電源バックアップソリューション

- UPS

- 発電機

- サービス-設計・コンサルティング、統合、サポート、メンテナンス

- 市場セグメンテーション-機械インフラ別

- 冷却システム

- 液浸冷却

- ダイレクト・ツー・チップ冷却

- リアドア熱交換器

- 列内とラック内冷却

- ラック

- その他の機械インフラ

- 一般構造

- 市場セグメンテーション:電気インフラ別

- 市場セグメンテーション-ティアタイプ別

- ティア1と2

- ティア3

- ティア4

- 市場セグメンテーション:エンドユーザー別

- 銀行、金融サービス、保険

- IT・通信

- 政府と防衛

- 医療

- その他

第6章 競合情勢

- 企業プロファイル

- AECOM

- DPR Construction

- Aurecon Group Pty Ltd

- Goodman Group

- Turner & Townsend

- DSCO Group Pte Ltd

- Hensel Phelps

- HP Construction

- M+W Shanghai Co. Ltd

- Gammon Construction Limited

第7章 投資分析

第8章 市場機会と今後の動向

第9章 出版社について

- 対象産業

- 産業クライアント一覧

- 当社のカスタマイズ調査能力

The China Data Center Construction Market size is estimated at USD 9.20 billion in 2024, and is expected to reach USD 15.70 billion by 2030, growing at a CAGR of 9.23% during the forecast period (2024-2030).

China houses more than 120 data center facilities, and it holds a majority in Asia-Pacific. The country's demand for newer data centers is due to the growing adoption of cloud computing, the Internet of Things (IoT), and artificial intelligence (AI).

Key Highlights

- The upcoming IT load capacity in the country is projected to cross 3,400 MW by 2030, boosting the demand for data center racks.

- The construction of raised floor area for data centers in the country is expected to reach 12.5 million sq. ft by 2030 for under construction raised floor space.

- The country's total number of installed racks will reach 620k units by 2030.

- Currently, five submarine cable projects are under construction in the country. One such submarine cable is Asia Direct Cable (ADC), stretching over 9,800 kilometers with landing points in Chung Hom Kok, China, and Shantou, China, expected to come into service from Q4 2024.

China Data Center Construction Market Trends

Tier 3 is the Largest Tier Type

- Tier 3 data centers are the most preferred due to features such as on-site assistance, power, and cooling redundancy. The segment is expected to grow from around 1300 MW in 2023 to 1,900 MW by 2030. Companies mainly choose these data centers for storing and processing business-critical data to cater to growing business and scalability needs. The country has around 110 tier 3 data centers, and around 37 upcoming data centers are under construction with tier 3 specifications.

- Shanghai hosts the country's maximum number of tier 3 data centers, with a market share of 28.9%, followed by Beijing at 26.3% and Guangdong at 20.2%.

- In 2023, GDS Service Co. Ltd had around 70 data centers with Tier 3 certification, followed by Chindata Group Holdings Ltd with 15 data center facilities and China Telecom Corporation Ltd with 10 data center facilities.

- Thirty-seven data center facilities under construction are being built with tier 3 standards and are expected to operate during the forecast period. Major players involved in tier 3 DC construction are Princeton Digital Group, GDS Service Co. Ltd, and Chindata Group Holdings. The construction is projected to be more concentrated in the Hebei region, followed by Beijing, Shanghai, and Jiangsu.

- Chindata Group has unveiled CN 23, a 26 MW hyperscale project set in a Zhangjiakou City, Hebei Province campus. The project is slated for delivery in Q1 of 2025 and is tailored for a prominent international client, designed to meet tier 3 standards. Such instances in the market are expected to create more demand for market growth in the coming years.

The IT and Telecommunications Segment is Expected to Hold the Major Share

- The Chinese government's 14th Year Plan drives initiatives to boost digital services. It prioritizes research in cutting-edge technologies like 6G, integrated circuits, and AI. These efforts are strategically aligned to meet China's rising demand for cloud computing services.

- The Chinese cloud market is poised to triple in value, surging from USD 30 billion in 2021 to a projected USD 90 billion by 2025, driven by escalating demands for cloud services. These services, encompassing software-as-a-service (SaaS), platform-as-a-service (PaaS), and infrastructure-as-a-service (IaaS), are directly accessible to end users.

- Users increasingly favor cloud services for their enhanced scalability. This allows them to adjust their networks, storage, and servers to meet specific business needs, such as China's Singles Day, a major shopping event. Websites offer enticing deals that draw in massive traffic and transactions. Cloud infrastructure makes managing this surge seamless, ensuring optimal performance.

- Cloud computing delivers services like additional computing power and data storage to clients through a web-based infrastructure. This cost-effective cloud infrastructure contrasts with traditional systems, which require large server farms and costly storage setups in data centers.

- Further, industries like gaming, video production, and mobile internet increasingly depend on the Cloud IaaS platform. With businesses shifting to cloud services for their swiftness, cost-effectiveness, and adaptability, the demand for cloud services has surged in tandem.

- According to data from the Ministry of Industry and Information Technology, in terms of telecommunication, by 2024, China's 5G network will blanket every city, town, and over 90% of its villages. The country boasts a dominant information and communication network, spearheaded by a staggering 3.84 million 5G base stations, representing over 60% of the world's total. Such instances in the market are expected to create more demand for data centers, thereby boosting the data center construction market.

China Data Center Construction Industry Overview

The Chinese data center construction market is moderately fragmented, with the top five companies occupying most of the market share. The major players in this market are AECOM, DPR Construction, Aurecon Group Pty Ltd, Goodman Group, and Turner & Townsend.

- SpaceDC, a forward-thinking data center provider headquartered in Singapore, has forged a strategic partnership with Centrin Data, a prominent tier 4 data center and network provider across China. This collaboration entails joint efforts to market Centrin Data's data centers and services within China, notably spotlighting Wuhan and Kunshan facilities, which boast a robust clientele in the financial sector. These data centers span a combined area of 206,532.41 m2 and can accommodate up to 40,000 racks. The development is planned in two stages, aiming for a total capacity of 225 MW, with the initial phase set at 70 MW. The facility is expected to come into operation during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 China Initiatives to Increase the Computing Power Drives the Demand for Data Center Construction

- 4.2.1.2 The Chinese Government's Initiatives to Modernize in the Digital Era are Fueling a Heightened Demand for Data Centers Across the Nation

- 4.2.2 Market Restraints

- 4.2.2.1 High Power Consumption and Emission Contribution of Data Centers

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key China Data Center Construction Statistics

- 4.4.1 Number of Data Centers In the China, 2022 and 2023

- 4.4.2 Data Center Under Construction in the China, in MW, 2024-2029

- 4.4.3 Average Capex and Opex For the China Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption In MW, Selected Cities, China, 2022 and 2023

- 4.4.5 The Top CAPEX Spenders on Data Center Infrastructure in China

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU - Basic and Smart - Metered and Switched Solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-voltage

- 5.1.1.1.3.2 Medium-voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Other Infrastructure

- 5.1.1.2 Power Back-up Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design and Consulting, Integration, Support and Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-to-chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-row and In-rack Cooling

- 5.1.2.1.5 Racks

- 5.1.2.1.6 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AECOM

- 6.1.2 DPR Construction

- 6.1.3 Aurecon Group Pty Ltd

- 6.1.4 Goodman Group

- 6.1.5 Turner & Townsend

- 6.1.6 DSCO Group Pte Ltd

- 6.1.7 Hensel Phelps

- 6.1.8 HP Construction

- 6.1.9 M+W Shanghai Co. Ltd

- 6.1.10 Gammon Construction Limited

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

- 9.1 Industries Covered

- 9.2 Illustrative List of Clients in the Industry

- 9.3 Our Customized Research Capabilities