米国のデータセンター建設:市場シェア分析、産業動向、成長予測(2025年~2030年)

United States (US) Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690781

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

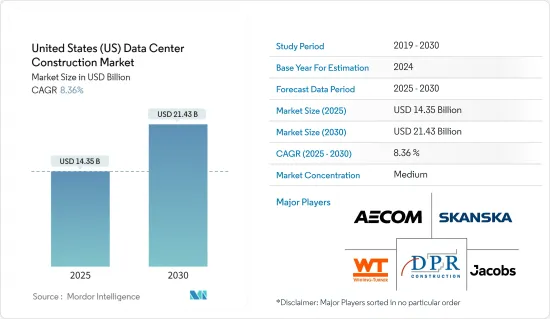

米国のデータセンター建設市場規模は2025年に143億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.36%で、2030年には214億3,000万米ドルに達すると予測されます。

主要ハイライト

- 米国市場は最も成熟しており、成長と運用の面で着実な成長を示しています。米国のデータセンター建設市場の成長は、IoTの採用拡大、5Gネットワークの市場開拓、企業によるクラウドベースのサービスの採用に起因しています。産業全体でデジタル化を採用することで、コロケーション、クラウド、インターネット、通信プロバイダによるデータセンター投資の増加や、オンラインエンターテイメントコンテンツの高速ストリーミングの需要に貢献すると考えられます。

- 同国のデータセンター市場は、ラックの電力密度の上昇、他国との接続性の向上、データセンターへのマイクログリッドの設置、5G接続、エッジデータセンター技術、新しいUPSバッテリー技術などにより成長が見込まれています。

- 米国政府は、開発用地の確保、電気料金の引き下げ、再生可能エネルギーの調達促進など、さまざまな手段でデータセンター投資を奨励しています。

- 例えば、アリゾナ州は外国貿易地区で事業を行う企業に対して様々な優遇措置を提供しています。貿易地区内の企業は、州の不動産・動産税が72.9%免除されます。このような取り組みは、今後10年間の米国のデータセンター建設市場の成長に貢献すると考えられます。

- 需要の高まりにもかかわらず、データセンター産業は高い需要を満たすためにいくつかの課題を抱えています。データセンター産業は、他の多くの不動産業と同様に、サプライチェーンの混乱による新たな建設の遅れに直面しています。人件費、建築資材、その他のコストの増加も資本支出を押し上げています。

- COVID-19の流行は、セクタを問わず経済全体にさらなる圧力をかけ、データセンターが提供するクラウドベースの作業環境の価値と可能性を浮き彫りにしました。COVID-19パンデミックの際、アメリカ人の53%がインターネットが不可欠だったと回答しました。このため、国内ではより多くのデータセンターが利用されるようになりました。

米国データセンター建設市場動向

電気インフラセグメントをリードするUPSシステム

- データセンターにとって無停電電源装置(UPS)システムは、サーバーやすべての機密コンピューティング機器が電力線の変動や電力品質の問題の影響を受けないようにするために不可欠です。停電はデータセンターのダウンタイムにつながり、データセンターの効率に影響を及ぼします。UPSシステムはまた、停電時に貴重なデータを自動的に保存するのに役立ちます。平均して、UPSシステムは8~10分間のバックアップを記載しています。

- 最近、国内の天候不順がデータセンターの運用に支障をきたしています。2024年1月から3月にかけて、国内は凍てつくような天候に見舞われ、カリフォルニア州とテキサス州の送電網の発電能力と稼働頻度に影響が出ました。電力供給の途絶は、同州のデータセンター運営に問題をもたらしました。UPSシステムの採用は、天候の変化によるこのような被害を軽減することにつながります。全国の様々な企業がデータセンターに依存しているため、無停電電源は極めて重要です。

- 長寿命、小型フォームファクタなど、いくつかの要因により、データセンターにリチウムイオンUPSシステムを採用する動向があります。国内のデータセンターによるエネルギー消費の増加は、リチウムイオンUPSシステムの採用を促進しています。

- ローレンスバークレー国立ラボによると、ハイパースケーラは通常、既存のデータセンターで1ラックあたり10~14kWを必要とするが、リソースを搭載したGPUを備えたAI対応ラックでは40~60kWに上昇するとみられます。つまり、米国全体のデータセンターの消費量は、2022年の17GWから2030年には35GWに達する見込みです。リチウムイオンUPSシステムは、大規模・小規模データセンター向けのUPSシステムに革命を起こすことになります。

- また、政府もデータセンターのエネルギー消費に向けた新たな取り組みを行っており、モジュール型UPSシステムの導入を促しています。米国政府は、2兆3,000億米ドルを拠出した2021年連結歳出法(Consolidated Appropriations Act 2021)の中で、データセンターのエネルギー効率目標と指標を盛り込みましたこの法律では、データセンターの使用によるエネルギーと水の消費に関する新たな調査と、そのようなデータセンターの効率を改善する方法を求めています。

- データセンターは運営経費の30%から50%を電力に費やしているため、データセンター管理への財務的影響も大きいです。米国国家資源防衛評議会によると、米国バージニア州北部のデータセンターの電力消費能力を合計すると、2023年には2.6GWに達し、世界最高となります。Cloudsceneによると、米国のデータセンター数は5381で、前年度の5375と比較して世界最多となっています。

医療セグメントが大きな成長を遂げる

- 電子カルテ(EMR)による医療記録のデジタル化は、膨大なデータ生成に大きく貢献しています。医療機器における最新の技術革新や、人員管理や患者対応システムの改善といった従来のオペレーティングシステムの近代化により、大量のデータが生成され、安全なデータセンターの需要がさらに高まっています。

- IoTのような技術は、遠隔モニタリングから医療機器の統合まで、医療に多くの応用があります。また、患者の健康と安全を維持し、医師がケアを提供する方法を改善する可能性もあります。しかし、センサ、ウェアラブル、遠隔モニター、その他の医療機器によって大量のデータが生成されています。

- 遠隔医療は、どの地域の消費者でも必要な医師にアクセスできるなど、さまざまな利点があるため、米国で利用が増加しています。通常予定されている診察が変更されることで費用と時間の両方が節約されるため、効率的な方法であり、それによって多くのデータが生成されるため、データセンターとデータセンター建設構想の必要性が強調されています。

- 米国国立衛生ラボによれば、2020年3月から2022年2月までの間に85万件以上の遠隔医療が行われ、その約62%がビデオ、約38%が電話によるものでした。また、Pharmaceutical Executive誌が398人の医療専門家を対象に行った調査によると、コロナウイルス(COVID-19)のパンデミック後も、患者の予約のほぼ20%が遠隔医療で行われると予測されています。

- 技術的なレベルでは、医療画像やゲノム研究の進歩により、新しいタイプのファイルサイズが大きくなっています。こうした要因が医療産業におけるデータ量の増加に寄与し、予測期間中の同地域におけるデータセンター建設の開発を後押ししています。

- さらに、同国政府は医療におけるデジタルヘルスと技術革新の役割を、成功する医療インフラの不可欠な要素として継続的に認識しています。同国政府は、医療部門を技術的に先進的ものにするために大きく前進しており、医療部門を支援するために医療支出を継続的に増やしています。例えば、CMS(Office of the Actuary)のデータによると、米国の国民医療費は2021年の4兆2,900億米ドルから2030年には6兆7,510億米ドルに達すると予測されています。

米国データセンター建設市場概要

米国のデータセンター建設市場は、AECOM、Whiting-turner Contracting Company、Jacobs Solutions Inc.、DPR Construction、Skanska USAなどの大手企業が存在し、半固体化しています。市場参入企業は、製品ラインナップを充実させ、市場での競合を維持するために、買収や提携などさまざまな戦略を採用しています。

- 2024年3月、スウェーデンを拠点とする著名な建設・開発企業であるSkanskaは、米国バージニア州で約2億4,200万米ドル相当の新規契約を締結したと発表しました。

- 2024年1月、Googleの完全子会社であるDesign LLCは、オレゴン州ワスコ郡に6億米ドルのデータセンターを建設するため、メリーランド州ボルチモアを拠点とするホワイティング・ターナーコントラクティング社を選定しました。この施設は29万平方フィートの計画で、オハイオ州、アイオワ州、ミズーリ州、アリゾナ州でも同様の投資が相次いでいます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場の促進要因

- クラウドアプリケーション、AI、ビッグデータの成長

- ハイパースケールデータセンターの採用増加

- 市場抑制要因

- 不動産コストの増加

- 市場の促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 米国の主要データセンター建設統計

- 米国のデータセンター数

- 米国で建設中のデータセンター(単位:MW)

- 米国データセンター建設の平均設備投資額とオペックス

- データセンターの電力吸収量(MW)(特定都市、米国)

- COVID-19の市場への影響評価

第5章 市場セグメンテーション

- インフラ別

- 電気インフラ

- UPSシステム

- その他の電気インフラ

- 機械インフラ

- 冷却システム

- ラック

- その他機械インフラ

- 一般建設

- 電気インフラ

- ティアタイプ別

- ティア-Iと-II

- ティア-III

- ティア-IV

- エンドユーザー別

- 銀行、金融サービス、保険

- IT・通信

- 政府・防衛

- 医療

- その他

第6章 競合情勢

- 企業プロファイル

- AECOM

- Whiting-turner Contracting Company

- Jacobs Solutions Inc.

- DPR Construction

- Skanska USA

- Balfour Beatty US

- Hensel Phelps

- McCarthy Building Companies Inc.

- Gilbane Building Company

- Brasfield & Gorrie LLC

第7章 投資分析

第8章 市場機会と今後の動向

目次

The United States Data Center Construction Market size is estimated at USD 14.35 billion in 2025, and is expected to reach USD 21.43 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

Key Highlights

- The US market is the most mature and shows steady growth in terms of growth and operations. The growth of the US data center construction market is attributed to the increasing adoption of IoT, the development of 5G networks, and the adoption of cloud-based services by businesses. Adopting digitalization across industries would contribute to a rise in data center investments by colocation, cloud, internet, and telecommunication providers, as well as the demand for the streaming of online entertainment content at high speeds.

- The country's data center market is expected to grow owing to a rise in rack power density, connectivity improvements with other nations, the installation of microgrids in data centers, 5G connectivity, edge data center technology, and new UPS battery technologies.

- The US government is encouraging data center investments by a various means, including increasing the availability of land for development, lowering electricity tariffs, and encouraging the procurement of renewable energy.

- For example, Arizona state offers various incentives to businesses that operate in the foreign trade zone. Businesses in a trade zone are entitled to a 72.9% exemption in state real and personal property taxes. Consequently, such initiatives would contribute to the growth of the data center construction market in the United States over the next decade.

- Despite the escalating demand, the data center industry is found to be prone to some challenges when it comes to satisfying high demand. The data center industry faces new construction delays due to supply chain disruptions, as in many other real estate verticals. Increasing labor, building materials, and other costs have also boosted capital expenditures.

- The COVID-19 pandemic placed additional pressure on the overall economy across sectors and highlighted the value and potential of the cloud-based work environment provided by data centers. During the COVID-19 pandemic, 53% of Americans said that the internet had been vital. This has increased the use of more data centers in the country.

United States (US) Data Center Construction Market Trends

UPS Systems to Lead the Electrical Infrastructure Segment

- An uninterruptible power supply (UPS) system is imperative for data centers to ensure that servers and all sensitive computing equipment are never susceptible to power line fluctuations and power quality issues. Any power failure can result in data center downtime, affecting the data center's efficiency. UPS systems also assist in saving valuable data automatically during a power outage. On average, a UPS system offers backup for 8-10 minutes.

- Lately, the unfavorable weather conditions in the country have caused interruptions in data center operations. From January 2024 to March 2024, the country was hit by freezing weather, which affected the grid generation capacity and operating frequency of California and Texas. The disruption in the power supply led to issues with the state's operation of data centers. The adoption of UPS systems results in mitigating such damages by weather changes. Various companies nationwide rely on data centers, which makes an uninterrupted power source crucial.

- There is a trend in adopting lithium-ion UPS systems in data centers due to several factors, such as longer life, small form factor, etc. The increasing consumption of energy by data centers in the country has been promoting the adoption of lithium-ion UPS systems.

- As per the Lawrence Berkeley National Laboratory, while the hyperscalers typically need 10-14 kW per rack in existing data centers, this is likely to rise to 40-60 kW for AI-ready racks equipped with resource-equipped GPUs. This means that overall consumption of data centers across the United States is expected to reach 35 GW by 2030, up from 17 GW in 2022. Lithium-ion UPS systems are set to revolutionize UPS systems for large and micro data centers.

- The government has also been taking new initiatives toward energy consumption by data centers, triggering modular UPS systems. In the USD 2.3 trillion-backed Consolidated Appropriations Act 2021, the US government included data center energy efficiency targets and metrics. The act calls for a new study on energy and water consumption by data center use and ways to improve the efficiency of such data centers.

- The financial impact for data center management is also huge as a data center spends between 30% and 50% of its operational expenditure on electricity. According to the United States National Resources Defense Council, the combined electricity consumption capacity of data centers in Northern Virginia, United States, amounted to 2.6 GW in 2023, the highest globally. According to Cloudscene, the United States also has the largest number of data centers globally with 5381 currently ccompared to 5375 data centers in the previous year.

Healthcare Sector to Witness Major Growth

- Digitization of consumer health records in the form of electronic medical records (EMR) has significantly contributed to massive data generation. The latest innovations in the medical equipment and the modernization of legacy operating systems, such as management of personnel and improvement in patient response systems, generate multitude of data, further boosting the demand for secured data centers.

- Technologies like IoT have a lot of applications in healthcare, from remote monitoring to medical device integration. It has also potential to keep patients healthy and safe and improve how physicians deliver care. However, a massive amount of data is being produced by sensors, wearables, remote monitors, and other medical devices.

- Telemedicine is increasing in usage in the United States, owing to various advantages, such as consumers from any region being able to gain access to required doctors. It is an efficient method, as both money and time are being saved due to the change in typically scheduled visits, thereby generating a lot of data and thus emphasizing the need for data centers and data center construction initiatives.

- As per the National Institutes of Health, between March 2020 and February 2022, more than 850,000 telemedicine visits occurred, with approximately 62% of visits by video and 38% by telephone. Besides, according to a survey of 398 healthcare professionals conducted by the Pharmaceutical Executive magazine, it has been predicted that after the coronavirus (COVID-19) pandemic, almost 20% of patient appointments will still be conducted via telemedicine compared to 2% beforehand and 61% perhaps during the pandemic.

- At the technical level, advances in medical imaging and genomic research are introducing new types of file types that are larger in size. These factors contribute to the increasing amount of data in the healthcare industry, which boosts the data center construction developments in the region during the forecast period.

- Moreover, the government of the country continuously recognizes the role of digital health and technological innovation in healthcare as an integral part of successful healthcare infrastructure. The government is making significant strides to make the healthcare sector technologically advanced and continuously increasing its healthcare expenditure to support the healthcare sector. For instance, according to the data from CMS (Office of the Actuary), the forecasted U.S. national health expenditure was expected to reach USD 6.751 trillion in 2030 from USD 4.29 trillion in 2021.

United States (US) Data Center Construction Market Overview

The US data center construction market is semi-consolidated with the presence of major players like AECOM, Whiting-turner Contracting Company, Jacobs Solutions Inc., DPR Construction, and Skanska USA. The market players are adopting various strategies, including acquisitions and partnerships to enhance their product offerings and remain competitive in the market.

- In March 2024, Sweden-based Skanska, a prominent construction and development company, announced a new contract worth approximately USD 242 million in Virginia, the United States.

- In January 2024, Design LLC, a wholly-owned subsidiary of Google, selected Baltimore, Maryland, based Whiting-Turner Contracting Co. to build a USD 600 million data center in Wasco County, Oregon. The facility is planned for 290,000 sq. ft. and will be the latest in a string of similar investments in Ohio, Iowa, Missouri, and Arizona.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Growing Cloud Applications, AI, and Big Data

- 4.2.1.2 Rising Adoption of Hyperscale Data Centers

- 4.2.2 Market Restraints

- 4.2.2.1 Increase in Real Estate Costs

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key United States Data Center Construction Statistics

- 4.4.1 Number of Data Centers in the United States

- 4.4.2 Data Center Under Construction in the United States, in MW

- 4.4.3 Average Capex and Opex for the United States Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption, in MW, Selected Cities, United States

- 4.5 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Infrastructure

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 UPS Systems

- 5.1.1.2 Other Electrical Infrastructure

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Electrical Infrastructure

- 5.2 By Tier Type

- 5.2.1 Tier-I and -II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AECOM

- 6.1.2 Whiting-turner Contracting Company

- 6.1.3 Jacobs Solutions Inc.

- 6.1.4 DPR Construction

- 6.1.5 Skanska USA

- 6.1.6 Balfour Beatty US

- 6.1.7 Hensel Phelps

- 6.1.8 McCarthy Building Companies Inc.

- 6.1.9 Gilbane Building Company

- 6.1.10 Brasfield & Gorrie LLC

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日