|

市場調査レポート

商品コード

1549806

マレーシアのデータセンター建設:市場シェア分析、産業動向、成長予測(2024年~2030年)Malaysia Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マレーシアのデータセンター建設:市場シェア分析、産業動向、成長予測(2024年~2030年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

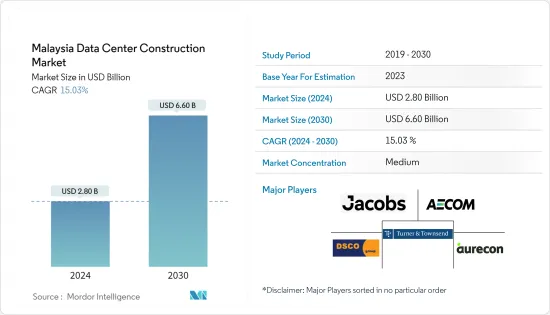

マレーシアのデータセンター建設市場規模は2024年に28億米ドルと推定され、2030年には66億米ドルに達すると予測され、予測期間中(2024~2030年)のCAGRは15.03%で成長する見込みです。

中小企業の間でクラウドコンピューティングの需要が高まっていること、国内のデータセキュリティを重視する政府規制が後押ししていること、国内参入企業による投資が活発化していることなどの要因が、マレーシア市場のデータセンター需要を促進する上で極めて重要です。

主要ハイライト

- 建設中のIT負荷容量:マレーシアのデータセンター建設市場における今後のIT負荷容量は、2030年までに1,460MWに達すると予想されます。

- 建設中の高床スペース:2030年までにマレーシアの床面積は520万平方フィートに増加する見込み。

- 計画中のラック:2030年までに設置されるラックの総数は26万3,359ユニットに達すると予想されます。サイバージャヤ・クアラルンプールは2030年までに最大数のラックを設置すると予想されます。

- 計画されている海底ケーブル:マレーシアを結ぶ海底ケーブルは23近くあり、その多くが建設中です。2025年にサービス開始が予定されている海底ケーブルのひとつがSeaMeWe-6で、マレーシアのモリブから陸揚げされる1万9,200km以上のケーブルです。

マレーシアのデータセンター建設市場動向

IT・通信セグメントが大きな市場シェアを獲得する見込み

- マレーシアの通信産業は現在、政府と主要な地元事業者の間で長期にわたる交渉段階にあります。最近の合意では、CelcomDigi、Maxis、U Mobile、Telekom Malaysia、YTL Power Internationalなどの大手通信事業者が、それぞれ約5,000万米ドルを投じてDNBの株式14%を購入することを約束しました。

- データセンターなどのデジタルインフラの整備は、5G用途の実現に不可欠です。このため、さまざまな投資家が5Gの開始に向けて契約を結んでいます。例えば、2024年6月、デュアルネットワーク5Gモデルを導入するマレーシアの事業者は、国営の5GネットワークであるDNB(Digital Nasional Berhad)の株式を取得することで最終合意したことを発表しました。

- さらに、政府は2つ目の5Gネットワークの計画を発表し、さまざまな業種に5G技術を導入することに重点を置いていることを強調しました。

- さらに、2024年4月までに、DNBの5Gネットワークは人口集中地域の81.5%をカバーし、普及率は39.2%に達しました。同国の5G契約数は累計1,320万件あります。これらの契約は、個人ユーザー向けが1,270万件、企業向けが42万2,609件に分かれています。契約数の増加により、データセンターへの依存度が高まることが予想されます。

- ITの面では、マレーシアはアジア太平洋市場で8位を確保し、CRIスコア68.5を誇った。特にクラウド規制では、マレーシアは24.9点を記録し、地域市場で8位にランクされました。大手プロバイダーのAmazon Web Services(AWS)は最近、マレーシア政府と新たなクラウドフレームワーク契約(CFA)を締結しました。この協業は、現地のITプロバイダーであるRadmik Solutions Sdn Bhdとともに、公共部門におけるクラウド導入を促進することを目的としています。このイニシアチブは、コスト削減、デジタルスキルの強化、政府機関全体のイノベーションの推進を目標としています。このような市場の動きは、データセンター構築の参入企業にとって今後数年でさらなるビジネス機会を生み出すと予想されます。

マレーシア市場ではティアIIIセグメントが大きなシェアを占める見込み

- マレーシアではティアIIIデータセンターが主に普及しており、その容量は2024年には575MWに達すると予測されています。このセグメントのCAGRは12.8%で、2029年にはIT負荷容量が1,186MWに達すると予測されています。

- 2023年時点で、マレーシアにはティアIII認証を受けたデータセンターが約45あり、累積IT負荷容量は約432MWです。信頼性と手頃な価格が、マレーシアのティアIIIデータセンター需要を促進する主要要因です。

- サイバージャヤは国内で最も多くのティアIIIデータセンターを擁しており、そのシェアは70.6%、次いでクアラルンプール、ジョホールバル、ジョージタウンとなっています。2023年には、VADS BERHAD(TMワン)がマレーシアでティアIII認証を取得したデータセンターを10カ所保有し、Open DC Sdn BhdとNTT Ltd.がそれぞれ4カ所でこれに続きます。

- マレーシアでは現在、10以上のデータセンター施設が建設中で、ティアIII規格に従って建設されています。ティアIII DCの建設に携わっている主要企業には、Bridge Data Center(Chindata Group)、Basis Bay、YTL Data Center Holdings Pte Ltd(YTL Power International Berhad)、Regal Orion Sdn Bhd、NTT Ltd.などがあります。建設はサイバージャヤ・クアラルンプール、ジョホールバル、ジョージタウンに集中すると予測されています。

- 2024年7月には、アジア太平洋データセンター企業のプリンストン・デジタルグループ(PDG)がマレーシアのジョホール・キャンパスの初期段階を完了し、52MWのIT負荷容量を誇った。こうした発展は、予測期間を通じて市場の成長を促進するものと考えられます。

マレーシアのデータセンター建設産業概要

マレーシアのデータセンター建設市場は、Aurecon Group Pty Ltd、AECOM、DSCO Group Pte Ltd、Turner &Townsend、Jacobs Engineering Groupなど数社の大手企業が半独立しています。

- 2024年4月、シンガポールの不動産会社であるAsia-Pacific Strategic Investments Limited(APS)は、マレーシアへの事業拡大を意図してデータセンター会社を買収しました。APSはホスピタリティ施設やリタイアメント・コミュニティの建設で知られ、今回の買収でデータセンター産業への初進出を果たしました。

- 2023年7月、Singtelはシンガポール政府首脳の国賓訪問に伴う同社との協議の中で、マレーシアのジョホール州にデータセンターを開発する計画を発表しました。これにより、同市場のベンダーにビジネス機会が生まれると期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場促進要因

- 企業や政府によるクラウドコンピューティングの急速な導入が市場の需要を牽引

- デジタル時代の近代化に向けた政府の取り組みが、全国的なデータセンター需要の高まりを促進

- 市場抑制要因

- 高い消費電力が投資を抑制

- 市場促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マレーシアの主要データセンター建設統計

- マレーシアのデータセンター数(2022年と2023年)

- マレーシアで建設中のデータセンター(MW)、2024~2029年

- マレーシアのデータセンター建設市場における平均設備投資額と平均運転費用額

- マレーシアのデータセンター電力吸収量(MW)、特定都市、2022年と2023年

- マレーシアにおけるデータセンターインフラへの設備投資額上位企業

第5章 市場セグメンテーション

- 市場セグメンテーション-インフラ別

- 市場セグメンテーション-電気インフラ別

- 配電ソリューション

- PDU-ベーシック&スマート-計量&スイッチソリューション

- 転送スイッチ

- 静的

- 自動(ATS)

- スイッチギア

- 低圧

- 高圧

- パワーパネルとコンポーネント

- その他の配電ソリューション

- 電源バックアップソリューション

- UPS

- 発電機

- サービス-デザイン&コンサルティング、インテグレーション、サポート&メンテナンス

- 市場セグメンテーション-機械インフラ別

- 冷却システム

- 液浸冷却

- ダイレクト・ツー・チップ冷却

- リアドア熱交換器

- 列内とラック内冷却

- ラック

- その他の機械インフラ

- 一般構造

- 市場セグメンテーション-電気インフラ別

- 市場セグメンテーション-ティアタイプ別

- ティアIとII

- ティアIII

- ティアIV

- 市場セグメンテーション-エンドユーザー別

- 銀行、金融サービス、保険

- IT・通信

- 政府・防衛

- 医療

- その他

第6章 競合情勢

- 企業プロファイル

- Aurecon Group Pty Ltd

- AECOM

- DSCO Group Pte Ltd

- Turner & Townsend

- Jacobs Engineering Group

- Gaw Capital Partners

- JLand Group(JLG)

- Cyclect Group

- Basis Bay

- Mah Sing Group Bhd

第7章 投資分析

第8章 市場機会と今後の動向

第9章 出版社について

- 対象産業

- 産業クライアント一覧

- 当社のカスタマイズ調査能力

The Malaysia Data Center Construction Market size is estimated at USD 2.80 billion in 2024, and is expected to reach USD 6.60 billion by 2030, growing at a CAGR of 15.03% during the forecast period (2024-2030).

Factors such as the rising demand for cloud computing among SMEs, bolstered by government regulations emphasizing local data security and amplified investments by domestic players, are pivotal in propelling the demand for data centers in the Malaysian market.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Malaysian data center construction market is expected to reach 1,460 MW by 2030.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 5.2 million sq. ft by 2030.

- Planned Racks: The country's total number of racks to be installed is expected to reach 263,359 units by 2030. Cyberjaya-Kuala Lumpur is expected to house the maximum number of racks by 2030.

- Planned Submarine Cables: There are close to 23 submarine cable systems connecting Malaysia, and many are under construction. One such submarine cable that is estimated to start service in 2025 is SeaMeWe-6, which stretches over 19,200 km with landing points from Morib, Malaysia.

Malaysia Data Center Construction Market Trends

IT and Telecom Segment Expected to Gain a Significant Market Share

- Malaysia's telecom industry is currently navigating an extended negotiation phase between the government and key local operators. In a recent agreement, major carriers, including CelcomDigi, Maxis, U Mobile, Telekom Malaysia, and YTL Power International, committed to purchasing a 14% stake in DNB, each investing approximately USD 50 million.

- The development of digital infrastructure, such as data centers, is central to enabling 5G applications. Owing to this, various investors are signing an agreement for the 5G launch. For instance, in June 2024, Malaysian operators implementing the dual-network 5G model announced that they were poised to finalize an agreement to acquire stakes in the state-operated 5G network, Digital Nasional Berhad (DNB).

- Further, the government announced its plans for a second 5G network, emphasizing its focus on implementing 5G technology across various verticals.

- Moreover, by April 2024, DNB's 5G network covered 81.5% of populated areas, with an adoption rate of 39.2%. The nation boasted a cumulative 13.2 million 5G subscriptions. These subscriptions were divided into 12.7 million for individual users and 422,609 for enterprises. The growing subscriptions are expected to increase dependency on data centers.

- In terms of IT, Malaysia secured the eighth spot in the Asia-Pacific market, boasting a CRI score of 68.5. Specifically, in cloud regulation, Malaysia notched a score of 24.9, ranking it 8th in the regional market. Leading provider Amazon Web Services (AWS) recently inked a fresh Cloud Framework Agreement (CFA) with the Malaysian government. This collaboration, alongside local IT provider Radmik Solutions Sdn Bhd, aims to expedite cloud adoption within the public sector. The initiative targets cost savings, enhanced digital skills, and a push for innovation across government agencies. Such instances in the market are expected to create more opportunities for data center construction players in the coming years.

Tier-III Segment Expected to Hold a Major Share in the Malaysian Market

- Tier-III data centers are majorly popular in Malaysia, with their capacity projected to reach 575 MW in 2024. The segment is estimated to reach an IT load capacity of 1,186 MW by 2029 while recording a CAGR of 12.8%.

- In 2023, there were around 45 data centers in Malaysia with tier-III certification and a cumulative IT load capacity of around 432 MW. Reliability and affordability are the major factors driving the country's demand for tier-III data centers.

- Cyberjaya hosts the maximum number of tier-III data centers in the country, with a share of 70.6%, followed by Kuala Lumpur, Johor Bahru, and George Town. In 2023, VADS BERHAD (TM One) had 10 data centers with tier-III certification in Malaysia, followed by Open DC Sdn Bhd and NTT Ltd, with four data center facilities each.

- More than 10 data center facilities are currently under construction in Malaysia and are being built in accordance with tier-III standards. Major players involved in tier-III DC construction include Bridge Data Center (Chindata Group), Basis Bay, YTL Data Center Holdings Pte Ltd (YTL Power International Berhad), Regal Orion Sdn Bhd, and NTT Ltd. The constructions are projected to be more concentrated in Cyberjaya-Kuala Lumpur, Johor Bahru, and George Town.

- In July 2024, Princeton Digital Group (PDG), an APAC data center company, completed the initial phase of its Johor campus in Malaysia, boasting an IT load capacity of 52 MW. Such developments are poised to fuel market growth through the forecast period.

Malaysia Data Center Construction Industry Overview

The Malaysian data center construction market is semi-consolidated, with a few major players, such as Aurecon Group Pty Ltd, AECOM, DSCO Group Pte Ltd, Turner & Townsend, and Jacobs Engineering Group.

- In April 2024, Asia-Pacific Strategic Investments Limited (APS), a Singaporean real estate firm, acquired a data center company with intentions to expand its operations into Malaysia. APS, known for its expertise in constructing hospitality establishments and retirement communities, marked its inaugural foray into the data center industry with this acquisition.

- In July 2023, Singtel announced plans to develop a data center in Johor, Malaysia, during discussions with the company on a state visit by the head of the Singaporean government. This is expected to create opportunities for the vendors in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 The Rapid Adoption of Cloud Computing by Enterprise and Government Drives Demand in the Market

- 4.2.1.2 Government Initiatives to Modernize in the Digital Era Fueling Heightened Demand for Data Centers Nationwide

- 4.2.2 Market Restraints

- 4.2.2.1 High Power Consumption can Deter Investments

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Malaysia Data Center Construction Statistics

- 4.4.1 Number of Data Centers In Malaysia, 2022 and 2023

- 4.4.2 Data Centers Under Construction in Malaysia, in MW, 2024 - 2029

- 4.4.3 Average Capex and Opex for the Malaysian Data Center Construction Market

- 4.4.4 Data Center Power Capacity Absorption in MW, Selected Cities, Malaysia, 2022 and 2023

- 4.4.5 Top Capex Spenders on Data Center Infrastructure in Malaysia

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU - Basic & Smart - Metered & Switched Solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-voltage

- 5.1.1.1.3.2 Medium-voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Other Power Distribution Solutions

- 5.1.1.2 Power Back Up Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-to-Chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-row and In-rack Cooling

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier-I and-II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aurecon Group Pty Ltd

- 6.1.2 AECOM

- 6.1.3 DSCO Group Pte Ltd

- 6.1.4 Turner & Townsend

- 6.1.5 Jacobs Engineering Group

- 6.1.6 Gaw Capital Partners

- 6.1.7 JLand Group (JLG)

- 6.1.8 Cyclect Group

- 6.1.9 Basis Bay

- 6.1.10 Mah Sing Group Bhd

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

- 9.1 Industries Covered

- 9.2 Illustrative List of Clients in the Industry

- 9.3 Our Customized Research Capabilities