|

市場調査レポート

商品コード

1549804

アジア太平洋のデータセンター建設:市場シェア分析、産業動向と統計、成長予測(2024年~2030年)APAC Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のデータセンター建設:市場シェア分析、産業動向と統計、成長予測(2024年~2030年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

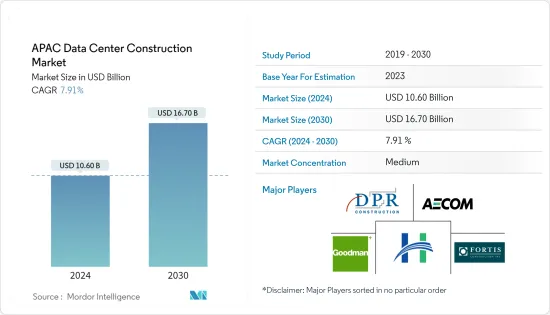

アジア太平洋のデータセンター建設市場規模は2024年に106億米ドルと推定され、2030年には167億米ドルに達し、予測期間中(2024~2030年)のCAGRは7.91%で成長すると予測されます。

アジア太平洋では、デジタル技術、クラウドコンピューティング、モノのインターネット(IoT)の急速な普及により、データセンターサービスの需要が急増しています。

建設中のIT負荷容量:アジア太平洋のデータセンター市場のIT負荷容量は、2030年までに2万1,000MWを超えると予想されます。

建設中の高床スペース:2030年までに、アジア太平洋の床面積は7,600万平方フィートを超えると予想されます。

計画中のラック:同地域の設置予定ラック総数は、2030年までに350万個を超えると予想されます。2030年までに最大数のラックが設置されるのはインドと予想されます。

アジア太平洋を結ぶ海底ケーブルシステムは160近くあり、その多くが建設中です。2024年に開通すると推定されているそのような海底ケーブルのひとつが、東南アジア-日本ケーブル2(SJC2)で、延長1万500kmを超え、中国、台湾、日本、韓国、タイ、ベトナムに陸揚げ地点を持っています。

さらに、すべての地域政府で持続可能エネルギーの導入が進んでいることから、既存のデータセンターや建設中のデータセンターの改修や新たなインフラ要件が増えると予想されます。台湾は、2025年までに風力発電と太陽光発電の推進計画によって電力の20%を発電し、再生可能エネルギーに依存することを目指しており、その結果、再生可能エネルギー発電容量は予測期間中に26GW以上に達します。

アジア太平洋のデータセンター建設市場の動向

格納式安全注射器セグメントは予測期間中に大きな成長が見込まれる

- オーストラリアはデータセンターソリューション市場の最前線に立っています。オーストラリア政府情報管理局(AGIMO)などの主導により、同国はオーストラリア政府データセンター戦略2010~2025を通じてデータセンター・リソースの最適化を推進しています。この戦略は、政府が運営するデータセンターから、サードパーティのマルチテナント施設へと移行する極めて重要な転換を意味します。さらに、オーストラリアの堅調なエネルギー部門がデータセンター市場の成長を後押ししています。

- シドニーは同地域の重要なハブとして際立っており、主に米国と英国から多額の投資を集めています。特に、再生可能エネルギーを重視するシドニーは、データセンターの重要な拠点として位置づけられています。特筆すべき成果シドニーは現在、ニューサウスウェールズ州の風力発電所と太陽光発電所から供給される再生可能エネルギーに依存しています。さらに、Central Coast Council、Hunter and Central Coast Development Corporation、主要産業関係者と協力し、グレーターシドニー委員会はセントラルコースト戦略の策定を主導しています。

- クラウドサービスは、特にオーストラリアで今話題になっている生成AI(GenAI)のような新興セグメントでのイノベーションを促進します。オーストラリアの企業では、ソフトウェアベースのビジネスアプリケーションからクラウドベースのビジネスアプリケーションへと移行し、アプリケーションの近代化が進んでいます。このシフトがSaaS投資の着実な増加に拍車をかけています。SaaSの採用はメリットをもたらすが、多くのベンダーが顧客の嗜好に関係なく、クラウドのみの提供に軸足を移しているため、SaaSの選択肢は少なくなりつつあります。

- さらに、国内での5Gネットワークの普及率の上昇により、データ生成量が増加することが予想され、これらのデータを保存・処理するためのより多くのスペースの必要性が高まると考えられます。個人的な利用とは別に、5G技術は主に製造、鉱業、医療などの産業オートメーションに大きな影響を与えると予想されます。この動向は、今後数年間でデータセンターの稼働率を引き上げ、予測期間中の同国におけるデータセンター建設需要を促進すると予想されます。

- 2023年、オーストラリアの小売売上高は前年比2%増に減速しました。しかし、オンライン小売はこの動向に逆行し、約414億米ドルの売上高に急増しました。特筆すべきは、様々な店舗にまたがるオンライン市場の売上が9.1%増加したことです。さらに、オンライン食料品ショッピングの急増に牽引された食品・酒類セグメントは、オンライン小売全体の成長を推進する上で極めて重要でした。

予測期間中、北米が大きな市場シェアを占める見込み

- オーストラリア2024~2025年の連邦予算において、連邦政府は今後4年間にわたる技術システムとポリシー開発のために最低28億米ドルを計上しました。この配分は、前年度予算の20億米ドルを上回ります。さらに、デジタルIDの導入を強化するために、同じ4年間で2億8,810万米ドルが割り当てられました。

- First Nationsのデジタルインクルージョンプログラムは、2024年に6,800万米ドルの多額の資金を確保しました。この配分には、遠隔地へのコミュニティWi-Fi配備のための4,000万米ドルと、First Nationsのデジタルサポートハブの設立のための2,200万米ドルが含まれています。このイニシアティブは、オンラインサービスへのアクセスを強化し、First Nationsの人々のデジタルリテラシーと安全性を強化することを目的としたデジタルメンターのネットワークも構築します。さらに、First Nationsのデジタルインクルージョンの取り組みに関する全国的なデータ収集の強化に600万米ドルが割り当てられています。

- 中国2024年3月、中国はビッグデータとAIの研究開発(R&D)を強化する野心的な計画を発表しました。この構想には、「AIプラス」プログラムの立ち上げと、国際競合を目指したデジタル産業クラスターの設立が含まれます。AIプラス」構想は、中国のデジタル経済を発展させる上で極めて重要な役割を果たす用意があり、AIと実体経済とのより深い統合を促進します。この動きは、中国のハイテク部門を活性化し、経済成長に拍車をかけることになると考えられます。

- 中国のAI産業は2023年に急成長し、中核部門は5,000億元(694億8,000万米ドル)の規模に達し、4,400社以上の企業を誇った。中国情報産業開拓センターのデータでは、前年比110%の伸びを予測し、大型AIモデルの市場規模は21億米ドルに達すると予測しています。

- 2024年2月、インド政府は通信省(DoT)を通じて「Sangam:デジタルツイン」構想を発表しました。このイニシアチブは、産業リーダー、イノベーター、中小企業、新興企業、学界、先進的な思想を持つ企業など、幅広い参加者から関心表明(EOI)を募っています。Sangam:デジタルツイン」は、5G、IoT、AR/VR、AI、AIネイティブ6G、「デジタルツイン」技術、最先端の計算ツールの能力を活用することで、インフラ計画と設計に革命を起こすことを目指しています。

- 上記のような事例から、スマートフォンの普及、IoTデバイスの利用拡大、クラウドの導入など、政府の取り組みが全国的なデジタルサービスの導入に拍車をかけており、データストレージのニーズが急増しています。その結果、こうした需要の高まりが地域のデータセンター建設市場の成長を後押ししています。

アジア太平洋のデータセンター建設産業概要

アジア太平洋のデータセンター建設市場は細分化されており、上位5社が市場シェアの大半を占めています。この市場の主要企業は、AECOM、DPR Construction、Fortis Construction、Goodman Group、Hibiya Engineering Ltd.、Larsen & Toubro Limited、Citramas Groupがあります。

2024年3月、BW DigitalとCitramas Groupは、インドネシア・バタム島のノンサ・デジタルパーク(NDP)内でキャリアニュートラルなデジタルエコシステムを開発する覚書に調印しました。この動きは、BWデジタルが最近、バタム島のシトラマス所有のノンサ・デジタルパークに5万5,000平方メートルを超える土地を取得したことに伴うものです。これは、BW Digitalが東南アジアで初めてデータセンターを設立し、アジア太平洋におけるデジタルインフラのプレゼンスを強化することを目的としています。

2024年3月、オーストラリアの産業スペシャリストであるGoodman Groupは、香港のチュンワンに50メガワットの最新データセンターを着工しました。この開発は、Goodmanにとって香港データセンター市場への8回目の進出となります。このプロジェクトは、香港の主要データセンター・アベイラビリティ・ゾーンの中心に位置する旧工業用地、Goodman Texaco Centreを改造するものです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- ドイツ

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場促進要因

- アジア太平洋では、持続可能性がますますデータセンター建設サービスの需要を形成

- デジタル経済とコネクティビティを促進するための政府による主要取り組み

- 市場抑制要因

- 国家安全保障上の懸念から、最近データ規制が強化され、データセンター建設市場の拡大を阻害

- 市場促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- アジア太平洋のデータセンター建設に関する主要統計

- アジア太平洋におけるデータセンター数(2022年と2023年)

- アジア太平洋におけるデータセンター建設中容量(MW)(2024~2029年)

- アジア太平洋のデータセンター建設の平均設備投資額と平均運転経費

- データセンターの電力吸収量(MW)(特定都市、アジア太平洋、2022年と2023年)

- アジア太平洋におけるデータセンターインフラへのCAPEX支出上位企業

第5章 市場セグメンテーション

- 市場セグメンテーション-インフラ別

- 市場セグメンテーション-電気インフラ別

- 配電ソリューション

- PDU:ベーシック&スマート-メータード&スイッチドソリューション

- 転送スイッチ

- 静的

- 自動(ATS)

- 開閉装置

- 低圧

- 高圧

- パワーパネルとコンポーネント

- その他

- パワーバックアップソリューション

- UPS

- 発電機

- サービス-デザイン&コンサルティング、インテグレーション、サポート&メンテナンス

- 市場セグメンテーション-機械インフラ別

- 冷却システム

- 液浸冷却

- ダイレクト・ツー・チップ冷却

- リアドア熱交換器

- インローとインラック冷却

- ラック

- その他の機械インフラ

- 一般構造

- 市場セグメンテーション-電気インフラ別

- 市場セグメンテーション-ティアタイプ別

- ティアIとII

- ティアIII

- ティアIV

- 市場セグメンテーション-エンドユーザー別

- 銀行、金融サービス、保険

- IT・通信

- 政府・防衛

- 医療

- その他

- 市場セグメンテーション-国別

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

第6章 競合情勢

- 企業プロファイル

- AECOM

- DPR Construction

- Fortis Construction

- Goodman Group

- Hibiya Engineering Ltd.

- Larsen & Toubro Limited

- GIC Private Limited.

- Sino Group

- Citramas Group

- Aurecon Group Pty Ltd.

第7章 投資分析

第8章 市場機会と今後の動向

第9章 出版社について

- 対象産業

- 産業クライアント一覧

- 当社のカスタマイズ調査能力

The APAC Data Center Construction Market size is estimated at USD 10.60 billion in 2024, and is expected to reach USD 16.70 billion by 2030, growing at a CAGR of 7.91% during the forecast period (2024-2030).

The demand for data center services in the Asia-Pacific region is surging, driven by the rapid adoption of digital technologies, cloud computing, and the Internet of Things (IoT).

Under Construction IT Load Capacity: The upcoming IT load capacity of the Asia-Pacific data center market is expected to reach above 21,000 MW by 2030.

Under Construction Raised Floor Space: The country's construction of raised floor areas is expected to exceed 76 million sq. ft. by 2030.

Planned Racks: The region's total number of racks to be installed is expected to reach more than 3.5 million units by 2030. India is expected to house the maximum number of racks by 2030.

Close to 160 submarine cable systems are connecting the Asia-Pacific, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 km and has a landing point in China, Taiwan, Japan, South Korea, Thailand, and Vietnam.

In addition, the growing adoption of sustainable energy across all regional governments is expected to drive more renovations and new infrastructure requirements in the existing and under-construction data centers. Taiwan aims to rely on renewable energy by generating 20% of its electricity through wind and solar PV promotion plans by 2025, resulting in renewable power capacity reaching over 26 GW during the forecast period.

APAC Data Center Construction Market Trends

Retractable Safety Syringes Segment Expected to Witness Significant Growth During the Forecast Period

- Australia stands at the forefront of the data center solutions market. Spearheaded by initiatives such as the Australia Government Information Management Office (AGIMO), the nation is driving the optimization of data center resources through its Australia Government Data Centre Strategy 2010-2025. This strategy marks a pivotal shift, moving away from government-operated data centers towards third-party, multi-tenant facilities. Additionally, Australia's robust energy sector bolsters the growth of its data center market.

- Sydney stands out as a pivotal hub in its region, drawing significant investments primarily from the United States and the United Kingdom. Notably, Sydney's emphasis on renewable energy has positioned it as a prominent center for data centers. A standout achievement: Sydney now exclusively relies on renewable energy sourced from local wind and solar farms in regional NSW. Moreover, in collaboration with the Central Coast Council, the Hunter and Central Coast Development Corporation, and key industry players, the Greater Sydney Commission is spearheading the development of the Central Coast Strategy.

- Cloud services drive innovation, especially in emerging fields like generative AI (GenAI), which is now making waves in Australia. Australian organizations are increasingly modernizing their applications, transitioning from software-based to cloud-based business applications. This shift is fueling a steady rise in SaaS investments. While SaaS adoption brings benefits, it's becoming less of a choice as numerous vendors are pivoting to cloud-only delivery, irrespective of customer preferences.

- Furthermore, an increase in the penetration rate of the 5G network in the country is expected to increase data generation, which would raise the need for more space for storing and processing these data. Apart from personal usage, 5G technology is expected to heavily influence industrial automation, primarily in manufacturing, mining, and healthcare. This trend is expected to raise the occupancy rate in data centers in the coming years, driving the demand for data center construction in the country during the forecast period.

- In 2023, Australia's retail sales growth decelerated to 2% year-on-year (YoY). However, online retail bucked the trend, surging to approximately USD 41.4 billion in sales. Notably, online marketplaces, spanning a range of stores, experienced a robust 9.1% uptick in sales. Moreover, the food and liquor segment, driven by a spike in online grocery shopping, was pivotal in propelling the overall online retail growth.

North America Expected to Hold Significant Market Share During the Forecast Period

- Australia: In the 2024-2025 Federal budget, the federal government earmarked a minimum of USD 2.8 billion for technology systems and policy development, spanning the next four years. This allocation surpasses the previous year's budget of USD 2 billion. Additionally, a specific allocation of USD 288.1 million over the same four-year period is designated to enhance the adoption of Digital ID.

- First Nations digital inclusion programs secured substantial funding of USD 68 million in 2024. This allocation includes USD 40 million earmarked for deploying community wi-fi in remote areas; another USD 22 million is designated for establishing a First Nations Digital Support Hub. This initiative will also create a network of digital mentors aimed at enhancing online service accessibility and bolstering digital literacy and safety for First Nations individuals. Additionally, USD 6 million has been allocated to enhance the national data collection pertaining to First Nations' digital inclusion efforts.

- China: In March 2024, it unveiled ambitious plans to intensify its focus on research and development (R&D) in big data and AI. This initiative includes launching an 'AI Plus' program and establishing digital industry clusters aimed at global competitiveness. The 'AI Plus' initiative is poised to play a pivotal role in advancing China's digital economy, facilitating a deeper integration of AI with the real economy. This move is set to invigorate China's high-tech sector and spur economic growth.

- China's AI industry surged in 2023, with the core sector hitting a scale of 500 billion yuan (USD 69.48 billion) and boasting over 4,400 enterprises. Data from the China Center for Information Industry Development projects a 110% year-on-year increase, forecasting the market scale for large AI models to hit USD 2.1 billion.

- India: In February 2024, the government of India, through the Department of Telecommunications (DoT), introduced the 'Sangam: Digital Twin' initiative. This initiative calls for Expressions of Interest (EOI) from a wide spectrum of participants, including industry leaders, innovators, MSMEs, startups, academia, and forward-thinkers. 'Sangam: Digital Twin' aims to revolutionize infrastructure planning and design by harnessing the capabilities of 5G, IoT, AR/VR, AI, AI-native 6G, 'Digital Twin' technology, and cutting-edge computational tools.

- From the above instances, government initiatives are spurring the adoption of digital services nationwide, such as smartphone penetration, increasing the usage of IoT devices, Cloud adoption, and others, driving a surge in data storage needs. Consequently, this uptick in demand is fueling growth in the regional data center construction market.

APAC Data Center Construction Industry Overview

The Asia-Pacific Data Center Construction Market is fragmented, with the top five companies occupying most of the market share. The major players in this market are AECOM, DPR Construction, Fortis Construction, Goodman Group, Hibiya Engineering Ltd., Larsen & Toubro Limited, Citramas Group, and others.

In March 2024, BW Digital and Citramas Group inked a memorandum of understanding (MoU) to develop a carrier-neutral digital ecosystem within Batam's Nongsa Digital Park (NDP), Indonesia. This move comes on the heels of BW Digital's recent land acquisition, spanning over 55,000 square meters at Citramas-owned Nongsa Digital Park in Batam. The purpose is to establish BW Digital's first data center in Southeast Asia, bolstering its digital infrastructure presence in Asia-Pacific.

In March 2024, the Australian industrial specialist, the Goodman Group, broke ground on its latest 50MW data center in Tsuen Wan, Hong Kong. This development represents Goodman's eighth foray into the Hong Kong data center market. Notably, the project involves transforming the Goodman Texaco Centre, a former industrial site situated at the heart of Hong Kong's key data center availability zone.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Germany

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 In the Asia Pacific region, sustainability is increasingly shaping the demand for data center construction services

- 4.2.1.2 Major initiatives undertaken by government to promote digital economy and connectivity

- 4.2.2 Market Restraints

- 4.2.2.1 Several nations, citing national security concerns, have recently bolstered their data regulations, impeding the expansion of the data center construction market.

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key APAC Data Center Construction Statistics

- 4.4.1 Number of Data Centers In the APAC, 2022 And 2023

- 4.4.2 Data Center Under Construction in the APAC, In MW, 2024 ? 2029

- 4.4.3 Average Capex and Opex For the APAC Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption In MW, Selected Cities, APAC, 2022 and 2023

- 4.4.5 The top CAPEX spenders on Data center infrastructure in the APAC.

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU: Basic & Smart - Metered & Switched solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-Voltage

- 5.1.1.1.3.2 Medium-Voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Others

- 5.1.1.2 Power Back up Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-To-Chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-Row and In-Rack Cooling

- 5.1.2.1.5 Racks

- 5.1.2.1.6 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier-I and II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Market Segmentation - By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 Indonesia

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AECOM

- 6.1.2 DPR Construction

- 6.1.3 Fortis Construction

- 6.1.4 Goodman Group

- 6.1.5 Hibiya Engineering Ltd.

- 6.1.6 Larsen & Toubro Limited

- 6.1.7 GIC Private Limited.

- 6.1.8 Sino Group

- 6.1.9 Citramas Group

- 6.1.10 Aurecon Group Pty Ltd.

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

- 9.1 Industries Covered

- 9.2 Illustrative List of Clients in the Industry

- 9.3 Our Customized Research Capabilities