|

|

市場調査レポート

商品コード

1452649

アジア太平洋のパン:2030年までの市場予測 - 地域別分析 - タイプ別、カテゴリー別、流通チャネル別Asia Pacific Bread Market Forecast to 2030 - Regional Analysis - by Type ; Category ; and Distribution Channel |

||||||

|

|||||||

|

|||||||

| アジア太平洋のパン:2030年までの市場予測 - 地域別分析 - タイプ別、カテゴリー別、流通チャネル別 |

|

出版日: 2024年01月16日

発行: The Insight Partners

ページ情報: 英文 76 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のパン市場は2023年に741億9,931万米ドルとなり、2030年には995億6,089万米ドルに達すると予測され、2023年から2030年までのCAGRは4.3%で成長すると予測されています。

簡便性と調理済み製品への需要増加がアジア太平洋のパン市場を後押し

アジア太平洋のパン市場は、簡便性とすぐに食べられる製品への嗜好の高まりにより需要が急増しています。現代の消費者の多忙なライフスタイルと、素早く簡単な食事ソリューションへのニーズが相まって、パンの消費が大幅に増加しています。調理のしやすさ、保存期間の長さ、持ち運びやすさといった利便性主導の要因により、パンは多忙な人々の間で人気の選択肢となっています。さらに、ローブ、サンドイッチ用パン、バゲット、ハンバーガー用バンズなど、多種多様なパンの選択肢が利用可能なため、多様な消費者の嗜好や食事要件に対応しています。

さらに、COVID-19の大流行もパン市場の急増に寄与しています。閉鎖や制限の間、消費者は保存が容易で賞味期限が長いパンのような主食に目を向けた。パンデミックによる家庭でのパン作りや料理活動の活発化も、人々が手作りの食事やスナックに安らぎを求め、パンの需要を押し上げました。その結果、ベーカリーやパン・メーカーは売上を伸ばし、消費者の嗜好の変化に対応するために製品ラインナップを拡大しました。

結論として、便利ですぐに食べられる製品に対する需要の増加とCOVID-19パンデミックの影響は、世界のパン市場の成長に大きく貢献しています。消費者が手軽で簡単な食事の解決策を求める中、多様なパン製品に対する需要は高まり続けています。市場が発展するにつれ、メーカーは消費者のニーズや嗜好の変化に対応するためにさらなる技術革新を進めるとみられ、アジア太平洋のパン市場の拡大を牽引しています。

アジア太平洋のパン市場概要

アジア太平洋のベーカリー産業は、インド、日本、中国、その他の国々におけるベーカリー製品の消費増加により、著しい成長を示しています。米国国際農産物貿易報告書によると、2021年の中国と日本の一人当たりのベーカリー製品消費量はそれぞれ7.2kg/年、22.5kg/年でした。また、中国における焼き菓子の小売売上高は2025年までに530億米ドルに達し、2021年比で53%増加すると予想されています。アジア太平洋では、便利ですぐに食べられる食品、特に焼き菓子(パン、バゲット、バンズ・ロール)に対する消費者の嗜好の高まりに加え、欧米スタイルの食生活へのシフトにより、さまざまなタイプのパンに対する需要が増加しています。さらに、都市化が加速し、ライフスタイルがますます多忙になるにつれて、この地域の消費者は手早く便利な食事の選択肢を求めるようになり、消費しやすいパンは魅力的な選択肢となっています。健康とウェルネスに関する意識の高まりは、消費者に全粒粉、多穀物、グルテンフリーなど、栄養面で利点のあるより健康的なパンを求めるよう促しています。そのため、この地域の消費者は食事に雑穀ベースの食品を選ぶようになっています。消費者の雑穀ベースのベーカリー製品の需要に対応するため、アジア太平洋のベーカリー・ブランドは新製品をますます発売しています。例えば、2023年4月、Bonn GroupのブランドであるBritanniaは、インドの消費者向けにマイダ添加ゼロの「Millet Bread」を発売しました。このパン製品にはラギ、ジョワール、バジュラ、オーツ麦が配合され、食物繊維とミネラルが含まれているため、消費者は食事に雑穀を使った選択肢を便利に取り入れることができます。このように、主要企業による栄養価の高い製品のイノベーションが、この地域のパン市場を牽引しています。しかし、インド、中国、韓国、その他のアジア太平洋諸国では、伝統的な食習慣や文化的嗜好が依然としてパンよりも米、小麦、雑穀、豆類、乳製品、野菜、果物、麺類、その他の主食を優先しているため、アジア太平洋でのパン市場の浸透は限定的です。

アジア太平洋のパン市場の収益と2030年までの予測(10億米ドル)

アジア太平洋のパン市場セグメンテーション

アジア太平洋のパン市場は、タイプ、カテゴリー、流通チャネル、国によって区分されます。

タイプ別では、アジア太平洋のパン市場はローブ、サンドイッチブレッド、バゲット、バーガーバンズ、その他に区分されます。2022年の市場シェアはパン類が最大でした。

カテゴリー別に見ると、アジア太平洋のパン市場はオーガニックと従来型に二分されます。2022年には従来型セグメントがより大きな市場シェアを占めました。

流通チャネル別では、アジア太平洋のパン市場はスーパーマーケットとハイパーマーケット、専門店、オンライン小売、その他に区分されます。スーパーマーケットとハイパーマーケットのセグメントが2022年に最大の市場シェアを占めました。

国別では、アジア太平洋のパン市場は中国、インド、韓国、オーストラリア、日本、その他アジア太平洋に区分されます。その他アジア太平洋が2022年のアジア太平洋のパン市場シェアを独占しました。

Campbell Soup Co.、Groupo Bimbo SAB de CV、Dr Schar AG、Bakers Delight Holdings、Britannia Industries Limitedなどがアジア太平洋のパン市場で事業を展開する大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- アジア太平洋の主要洞察

- アジア太平洋市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋のパン市場情勢

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- エコシステム分析

- 原材料

- 製造プロセス

- 混合原料

- ライジング(発酵)

- 混練

- プルーフィング(二次発酵)

- 焼成

- 冷却

第5章 アジア太平洋のパン市場:主要産業力学

- 市場促進要因

- 簡便性と調理済み製品に対する需要の増加

- eコマースを通じたパンの入手可能性の増加

- 主な市場抑制要因

- 原材料価格の変動

- 主な市場機会

- 製品のイノベーション

- 今後の動向

- グルテンフリー製品に対する需要の高まり

- 促進要因と抑制要因の影響

第6章 アジア太平洋のパン市場分析

- アジア太平洋のパン市場収益、2022年~2030年

- アジア太平洋のパン市場の予測と分析

第7章 アジア太平洋のパン市場分析:タイプ

- ローフ

- サンドイッチブレッド

- バゲット

- ハンバーガーバンズ

- その他

第8章 アジア太平洋のパン市場収益分析:カテゴリー別

- オーガニック

- 従来

第9章 アジア太平洋のパン市場収益分析-流通チャネル別

- スーパーマーケットとハイパーマーケット

- 専門店

- オンライン小売

- その他

第10章 アジア太平洋のパン市場:国別分析

- アジア太平洋

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- APACのその他諸国

第11章 アジア太平洋のパン市場-COVID-19パンデミックの影響

- COVID-19前後の影響

第12章 企業プロファイル

- Dr Schar AG

- Britannia Industries Ltd

- Bakers Delight Holdings Ltd

- Campbell Soup Co

- Grupo Bimbo SAB de CV

第13章 付録

List Of Tables

- Table 1. Asia Pacific Bread Market Revenue and Forecasts To 2030 (US$ Billion)

- Table 2. Australia: Bread Market, by Category Revenue and Forecast to 2030 (US$ Billion)

- Table 3. Australia: Bread Market, by Distribution Channel Revenue and Forecast to 2030 (US$ Billion)

- Table 4. China: Bread Market, by Type Revenue and Forecast to 2030 (US$ Billion)

- Table 5. China: Bread Market, by Category Revenue and Forecast to 2030 (US$ Billion)

- Table 6. China: Bread Market, by Distribution Channel Revenue and Forecast to 2030 (US$ Billion)

- Table 7. India: Bread Market, by Type Revenue and Forecast to 2030 (US$ Billion)

- Table 8. India: Bread Market, by Category Revenue and Forecast to 2030 (US$ Billion)

- Table 9. India: Bread Market, by Distribution Channel Revenue and Forecast to 2030 (US$ Billion)

- Table 10. Japan: Bread Market, by Type Revenue and Forecast to 2030 (US$ Billion)

- Table 11. Japan: Bread Market, by Category Revenue and Forecast to 2030 (US$ Billion)

- Table 12. Japan: Bread Market, by Distribution Channel Revenue and Forecast to 2030 (US$ Billion)

- Table 13. South Korea: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- Table 14. South Korea: Bread Market, by Type Revenue and Forecast to 2030 (US$ Billion)

- Table 15. South Korea: Bread Market, by Distribution Channel Revenue and Forecast to 2030 (US$ Billion)

- Table 16. Rest of APAC: Bread Market, by Type Revenue and Forecast to 2030 (US$ Billion)

- Table 17. Rest of APAC: Bread Market, by Category Revenue and Forecast to 2030 (US$ Billion)

- Table 18. Rest of APAC: Bread Market, by Distribution Channel Revenue and Forecast to 2030 (US$ Billion)

List Of Figures

- Figure 1. Asia Pacific Bread Market Segmentation, By Country

- Figure 2. Porter's Five Forces Analysis

- Figure 3. Ecosystem: Asia Pacific Bread Market

- Figure 4. Asia Pacific Bread Market - Key Industry Dynamics

- Figure 5. Impact Analysis of Drivers and Restraints

- Figure 6. Asia Pacific Bread Market Revenue (US$ Billion), 2022 - 2030

- Figure 7. Asia Pacific Bread Market Share (%) - Type, 2022 and 2030

- Figure 8. Loaves: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 9. Sandwich Breads: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 10. Baguettes: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 11. Burger Buns: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 12. Others: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 13. Asia Pacific Bread Market Revenue Share, By Category (2022 and 2030)

- Figure 14. Organic: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 15. Conventional: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 16. Asia Pacific Bread Market Revenue Share, By Distribution Channel (2022 and 2030)

- Figure 17. Supermarkets and Hypermarkets: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 18. Specialty Stores: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 19. Online Retail: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 20. Others: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- Figure 21. Asia Pacific: Bread Market (US$ Bn) (2022)

- Figure 22. Asia Pacific: Bread Market Revenue Share, By Key Country (2022 and 2030)

- Figure 23. Australia: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 24. Australia: Bread Market, by Type Revenue and Forecast to 2030 (US$ Billion)

- Figure 25. China: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 26. India: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 27. Japan: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 28. South Korea: Bread Market, by Category Revenue and Forecast to 2030 (US$ Billion)

- Figure 29. Rest of APAC: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

The Asia Pacific bread market was valued at US$ 74,199.31 million in 2023 and is expected to reach US$ 99,560.89 million by 2030; it is estimated to grow at a CAGR of 4.3% from 2023 to 2030.

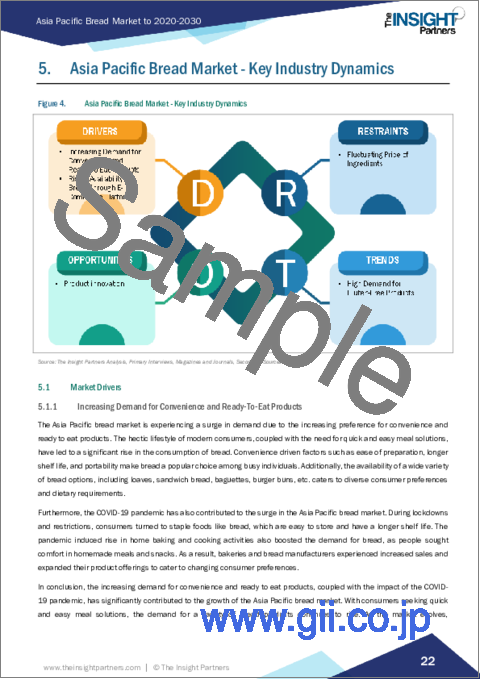

Increasing Demand for Convenience and Ready-To-Eat Products Fuel the Asia Pacific Bread Market

The Asia Pacific bread market is experiencing a surge in demand due to the increasing preference for convenience and ready to eat products. The hectic lifestyle of modern consumers, coupled with the need for quick and easy meal solutions, have led to a significant rise in the consumption of bread. Convenience driven factors such as ease of preparation, longer shelf life, and portability make bread a popular choice among busy individuals. Additionally, the availability of a wide variety of bread options, including loaves, sandwich bread, baguettes, burger buns, etc. caters to diverse consumer preferences and dietary requirements.

Furthermore, the COVID-19 pandemic has also contributed to the surge in the bread market. During lockdowns and restrictions, consumers turned to staple foods like bread, which are easy to store and have a longer shelf life. The pandemic induced rise in home baking and cooking activities also boosted the demand for bread, as people sought comfort in homemade meals and snacks. As a result, bakeries and bread manufacturers experienced increased sales and expanded their product offerings to cater to changing consumer preferences.

In conclusion, the increasing demand for convenience and ready to eat products, coupled with the impact of the COVID-19 pandemic, has significantly contributed to the growth of the global bread market. With consumers seeking quick and easy meal solutions, the demand for a variety of bread products continues to rise. As the market evolves, manufacturers are likely to innovate further to meet the changing needs and preferences of consumers, driving the expansion of the Asia Pacific bread market.

Asia Pacific Bread Market Overview

The bakery industry in Asia Pacific has shown significant growth owing to the rising consumption of bakery products in India, Japan, China, and other countries in the region. According to the US International Agricultural Trade Report, in 2021, per capita consumption of baked products in China and Japan was 7.2 kg/year and 22.5 kg/ year, respectively. Also, retail sales of baked goods in China are expected to reach US$ 53 billion by 2025, a 53% increase compared to 2021. The demand for different types of bread is increasing in Asia Pacific due to a rising consumer preference for convenient and ready-to-eat food products especially baked goods (bread, baguettes, and buns and rolls), along with the shift toward Western-style diets. Furthermore, as urbanization continues to accelerate and lifestyles become increasingly hectic, the consumers in the region are seeking quick and convenient meal options, making bread an attractive choice due to its ease of consumption. The growing awareness regarding health and wellness has prompted consumers to look for healthier bread options, such as whole-grain, multigrain, and gluten-free varieties, which offers nutritional benefits. Therefore, consumers in the region are increasingly opting for millet-based food products in their meals. To cater to the millet-based bakery products demand of the consumers, Asia Pacific bakery brands are increasingly launching new products. For instance, in April 2023, Britannia, a brand of Bonn Group, launched "Millet Bread" with zero added Maida for Indian consumers. This bread product is incorporated with ragi, jowar, bajra, and oats and has fiber and minerals that provide consumers with a convenient way to include millet-based options in their meals. Thus, nutritional product innovations by the key players are driving the bread market across the region. However, in India, China, South Korea, and other Asian countries, traditional food habits and cultural preferences still prioritize rice, wheat, millet, pulses, dairy, vegetables, fruits, noodles, and other staple foods over bread, thereby limiting its market penetration in Asia Pacific.

Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

Asia Pacific Bread Market Segmentation

The Asia Pacific bread market is segmented based on type, category, distribution channel, and country.

By type, the Asia Pacific bread market is segmented into loaves, sandwich bread, baguettes, burger buns, and others. The loaves segment held the largest market share in 2022.

Based on category, the Asia Pacific bread market is bifurcated into organic and conventional. The conventional segment held a larger market share in 2022.

By distribution channel, the Asia Pacific bread market is segmented into supermarkets and hypermarkets, specialty stores, online retail, and others. The supermarkets and hypermarkets segment held the largest market share in 2022.

In terms of country, the Asia Pacific bread market is segmented into China, India, South Korea, Australia, Japan, and the Rest of Asia Pacific. The Rest of Asia Pacific dominated the Asia Pacific bread market share in 2022.

Campbell Soup Co., Groupo Bimbo SAB de CV, Dr Schar AG, Bakers Delight Holdings, and Britannia Industries Limited are some of the leading players operating in the Asia Pacific bread market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Asia Pacific Key Insights

- 2.2 Asia Pacific Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Bread Market Landscape

- 4.1 Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 The threat of New Entrants

- 4.2.4 The Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Ecosystem Analysis

- 4.3.1 Raw Materials

- 4.3.2 Manufacturing Process

- 4.3.2.1 Mixing Ingredients

- 4.3.2.2 Rising (Fermentation)

- 4.3.2.3 Kneading

- 4.3.2.4 Proofing (Second Rising)

- 4.3.2.5 Baking

- 4.3.2.6 Cooling

5. Asia Pacific Bread Market - Key Industry Dynamics

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Convenience and Ready-To-Eat Products

- 5.1.2 Rising Availability of Bread Through E-Commerce Platforms

- 5.2 Key Market Restraints:

- 5.2.1 Fluctuating Price of Ingredients

- 5.3 Key Market Opportunities:

- 5.3.1 Product innovation

- 5.4 Future Trends:

- 5.4.1 High Demand for Gluten-Free Products

- 5.5 Impact of Drivers and Restraints:

6. Bread Market - Asia Pacific Market Analysis

- 6.1 Asia Pacific Bread Market Revenue (US$ Billion), 2022 - 2030

- 6.2 Asia Pacific Bread Market Forecast and Analysis

7. Asia Pacific Bread Market Analysis - Type

- 7.1 Loaves

- 7.1.1 Overview

- 7.1.2 Loaves: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 7.2 Sandwich Breads

- 7.2.1 Overview

- 7.2.2 Sandwich Breads: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 7.3 Baguettes

- 7.3.1 Overview

- 7.3.2 Baguettes: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 7.4 Burger Buns

- 7.4.1 Overview

- 7.4.2 Burger Buns: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 7.5 Others

- 7.5.1 Overview

- 7.5.2 Others: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

8. Asia Pacific Bread Market Revenue Analysis - By Category

- 8.1 Overview

- 8.2 Asia Pacific Bread Market, By Category (2022 and 2030)

- 8.3 Organic

- 8.3.1 Overview

- 8.3.2 Organic: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 8.4 Conventional

- 8.4.1 Overview

- 8.4.2 Conventional: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

9. Asia Pacific Bread Market Revenue Analysis - By Distribution Channel

- 9.1 Overview

- 9.2 Asia Pacific Bread Market, By Distribution Channel (2022 and 2030)

- 9.3 Supermarkets and Hypermarkets

- 9.3.1 Overview

- 9.3.2 Supermarkets and Hypermarkets: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 9.4 Specialty Stores

- 9.4.1 Overview

- 9.4.2 Specialty Stores: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 9.5 Online Retail

- 9.5.1 Overview

- 9.5.2 Online Retail: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 9.6 Others

- 9.6.1 Overview

- 9.6.2 Others: Asia Pacific Bread Market Revenue and Forecast to 2030 (US$ Billion)

10. Asia Pacific Bread Market - Country Analysis

- 10.1 Overview: Asia Pacific Bread Market

- 10.1.1 Asia Pacific: Bread Market Revenue and Forecast to 2030 (US$ Billion)

- 10.1.2 Asia Pacific: Bread Market, By Key Country

- 10.1.2.1 Australia: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- 10.1.2.1.1 Australia: Bread Market, by Type

- 10.1.2.1.2 Australia: Bread Market, by Category

- 10.1.2.1.3 Australia: Bread Market, by Distribution Channel

- 10.1.2.2 China: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- 10.1.2.2.1 China: Bread Market, by Type

- 10.1.2.2.2 China: Bread Market, by Category

- 10.1.2.2.3 China: Bread Market, by Distribution Channel

- 10.1.2.3 India: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- 10.1.2.3.1 India: Bread Market, by Type

- 10.1.2.3.2 India: Bread Market, by Category

- 10.1.2.3.3 India: Bread Market, by Distribution Channel

- 10.1.2.4 Japan: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- 10.1.2.4.1 Japan: Bread Market, by Type

- 10.1.2.4.2 Japan: Bread Market, by Category

- 10.1.2.4.3 Japan: Bread Market, by Distribution Channel

- 10.1.2.5 South Korea: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- 10.1.2.5.1 South Korea: Bread Market, by Type

- 10.1.2.5.2 South Korea: Bread Market, by Category

- 10.1.2.5.3 South Korea: Bread Market, by Distribution Channel

- 10.1.2.6 Rest of APAC: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

- 10.1.2.6.1 Rest of APAC: Bread Market, by Type

- 10.1.2.6.2 Rest of APAC: Bread Market, by Category

- 10.1.2.6.3 Rest of APAC: Bread Market, by Distribution Channel

- 10.1.2.1 Australia: Bread Market Revenue and Forecasts to 2030 (US$ Billion)

11. Asia Pacific Bread Market - Impact of COVID-19 Pandemic

- 11.1 Pre & Post Covid-19 Impact

12. Company Profiles

- 12.1 Dr Schar AG

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Britannia Industries Ltd

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Bakers Delight Holdings Ltd

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Campbell Soup Co

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Grupo Bimbo SAB de CV

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

13. Appendix

- 13.1 Appendix