ステビア:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Stevia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939010

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

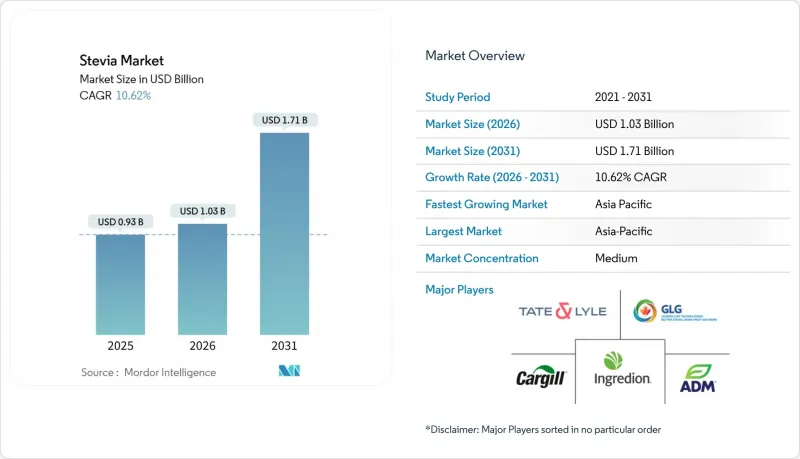

2026年のステビア市場規模は10億3,000万米ドルと推定され、2025年の9億3,000万米ドルから成長が見込まれます。

2031年までの予測では17億1,000万米ドルに達し、2026年から2031年にかけてCAGR10.62%で拡大する見通しです。

この成長は、レバウディオサイドMや酵素修飾グリコシドに対するFDAのGRAS(一般に安全と認められる)通知など、規制面の支援強化によって推進されています。これらは製品の安全性を確保し、より広範な採用を促進します。砂糖摂取に対する健康懸念の高まりと、肥満や糖尿病の増加傾向が相まって、メーカーは植物由来の代替品を採用するよう迫られており、ステビアは砂糖削減の重要な解決策となっています。アジア太平洋地域は、その規模と専門性からステビア栽培・加工の主導的地位を維持しております。しかしながら、関税政策や労働慣行への監視強化といった課題により、買い手は代替調達先の模索を迫られております。加えて、バイオ変換技術や精密発酵技術の進歩により、ステビアの生産コスト削減と風味プロファイルの改善が進み、より幅広い用途での利用が可能となっております。

世界のステビア市場の動向と洞察

消費者嗜好の自然由来・植物性甘味料への移行

人工甘味料に代わる天然由来の代替品を求める消費者の嗜好が、甘味料市場におけるステビアの優位性を牽引しております。特にクリーンラベルへの要求や原材料の透明性が購買行動に影響を与える先進国市場において顕著です。2025年5月に米国食品医薬品局(FDA)がステビオール配糖体のGRAS(一般に安全と認められる)承認を行ったような規制面の進展は、安全性と汎用性を確認することで信頼性を高めています。外食産業事業者や製造業者を含む機関購買者も、健康志向で持続可能な製品への需要に応えるためステビアを採用しています。ステビアの安定した需要は、甘味料市場における主要な促進要因としての地位を確立し、業界の進化において重要な役割を担っています。

ステビアを特徴とした新製品発売による市場成長の加速

メーカー各社は、飲料・乳製品・焼き菓子におけるステビアの汎用性を活用し、味覚面の課題を解決しながら製品革新を推進しています。例えばカーギル社とDSM-フィルメニヒ社の「エバースイート」シリーズは精密発酵技術により、後味のない砂糖類似のレブM・レブD分子を生成しています。2024年には欧州連合が発酵ベースのステビア製品を承認し、同地域での幅広い展開が可能となりました。製造プロセスの改善によりコストも低下し、ステビアは人工甘味料に代わる現実的な選択肢となっています。コカ・コーラなどの飲料大手は、優れた味覚特性、規制面の支援、コスト効率を背景にゼロシュガー製法の研究開発に投資しており、飲食品カテゴリー全体でのイノベーションを促進しています。

農業要因によるステビア葉価格の変動性

ステビア生産者は、変動する農産物価格、予測困難な天候、地政学的イベントによる課題に直面しています。これらはサプライチェーンを混乱させ、価格予測を複雑化させます。特定地域への生産集中は、気候変動によって悪化する地域的な供給障害のリスクを高めています。米国税関が強制労働懸念から中国産ステビア抽出物を差し押さえた事例など、地政学的緊張が脆弱性を浮き彫りにしています。中国・インドからの輸入品に対する関税は、メーカーの調達先多様化を促し、短期的なコスト上昇をもたらす一方、国内生産を促進しています。スプレンダ社が2023年3月に稼働を開始したフロリダ州の5,000万米ドル規模の施設は、国際市場への依存度低減を目的としています。各社は垂直統合の推進や精密発酵技術の探求を通じて、サプライチェーンの強化と持続可能なステビア市場の確保に取り組んでいます。

セグメント分析

2025年現在、粉末ステビアは94.78%の市場シェアを占め、飲食品製造における主要選択肢としての地位を確立しています。その優位性は、安定性、長期保存性、製造プロセスとの適合性に起因します。粉末形態は取り扱い容易性、精密な計量、コスト効率の高い生産性から好まれ、大規模用途に最適です。ホーエンハイム大学の調査によれば、その汎用性は飲料分野で160~700mg/kg、乳製品デザート分野で500~1000mg/kgの使用レベルが確認されています。耐湿性と熱安定性を備えるため、液状製品では品質が損なわれる可能性のある製パン用途にも適しています。

液体ステビアは、2026年から2031年にかけてCAGR12.31%と予測される、最も成長が著しい形態セグメントとして台頭しています。この成長は、溶解性と味に関する従来の課題を解決した技術的進歩によって推進されています。完全な溶解と精密な甘味制御を必要とするゼロ糖飲料への需要増加が、液体形態の採用を促進する重要な要因です。コカ・コーラなどの業界リーダーは、革新的な組成や噴霧乾燥製法を通じてレバウディオサイドMの溶解性向上に積極的に取り組んでおります。さらに、イングレディオン社の「クリーンテイスト溶解性ソリューション」は、液体ステビア応用における進歩を示しており、飲料メーカーの進化するニーズに応えるため、味と機能性の両方を向上させております。

地域別分析

2025年時点で、アジア太平洋地域は世界のステビア市場において31.05%のシェアを占めており、2026年から2031年にかけてCAGR11.94%で成長すると予測されています。この成長は、中国、インド、日本における確立された栽培基盤と消費量の増加によって牽引されています。インド化学工業協会は、栽培から製造に至るシームレスなサプライチェーンを同地域の強みとして挙げています。しかしながら、中国が主導的立場にある一方で、米国税関による強制労働疑惑をめぐる規制上の課題に直面しており、メーカーは調達先の見直しを迫られています。一方、政府の施策に支えられたインドの成長著しいステビア産業が代替案を提供しています。ステビオシド蓄積のためのナノテクノロジーなどの革新技術は、同地域の地位をさらに強化しています。

北米では、確立された規制と消費者の受容があるもの、伝統的な飲食品分野の市場飽和により成長は鈍化しています。テート・ライル社のマヌス社との提携は、ステビアReb M生産におけるサプライチェーンの進展を示しています。欧州市場では、クリーンラベル製品や低糖製品への需要を背景に、プレミアムステビア用途への移行が進んでいます。開発企業は、乳製品・飲料・ベーカリー製品向けに、風味マスキング技術や新規ブレンドによる味覚課題の解決に取り組んでいます。ステビア原産の南米では、栽培ノウハウと新興の加工技術が融合しています。ただし、マクロ経済の変動やインフラ問題が規模拡大の障壁となっています。生産者は職人的な栽培と持続可能な調達に注力し、世界のバイヤーはトレーサビリティとESG基準を優先しています。パラグアイは伝統的な葉栽培の中心地であり、本物を求めるブランドに支持されています。中東・アフリカでは健康意識と規制支援が高まっていますが、現地生産は限定的です。サウジアラビアとUAEにおける砂糖入り飲料への50%の物品税がステビア採用を促進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 消費者の嗜好が天然由来・植物性甘味料へ移行

- ステビアを主成分とする新製品の発売が市場成長の急拡大を促進

- 医薬品および栄養補助食品におけるステビアの利用拡大

- ステビア抽出・加工技術の進歩

- 世界の糖尿病および肥満の増加傾向

- 機能性食品および強化食品におけるステビアの使用拡大

- 市場抑制要因

- 農業要因によるステビア葉価格の変動性

- 甘味料分野における厳しい規制要件と長い承認プロセス

- サプライチェーンの混乱による製品供給への影響

- 従来の甘味料と比較した高い生産コスト。

- 消費者行動分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- フォーマット別

- 粉末

- 液体

- 成分タイプ別

- オーガニック

- 従来型

- 用途別

- ベーカリー

- 菓子類

- 飲料

- 乳製品

- 卓上用甘味料

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cargill, Incorporated

- Ingredion Incorporated

- Tate & Lyle PLC

- Archer Daniels Midland Company

- GLG Life Tech Corporation

- Morita Kagaku Kogyo Co. Ltd

- Pyure Brands LLC

- Sunwin Stevia International, Inc.

- Evolva Holding SA

- Wisdom Natural Brands(SweetLeaf)

- SweeGen Inc.

- Arzeda Corp.

- Guilin Layn Natural Ingredients Corp.

- Zhucheng Haotian Pharma Co. Ltd

- Steviva Brands Inc.

- Xinghua GL Stevia Co., Ltd

- Ganzhou Julong High-Tech Industrial Co. Ltd

- Shandong Huaxian Stevia Co., Ltd.

- Jining Aoxing Stevia Products Co., Ltd.

- The Real Stevia Company AB

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日