|

市場調査レポート

商品コード

1639526

建築用接着剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Construction Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 建築用接着剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

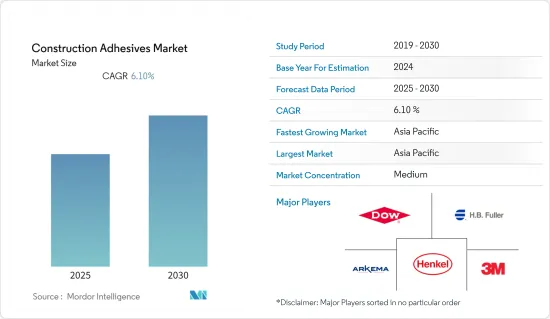

建設用接着剤市場は予測期間中に6.1%のCAGRで推移する見込みです。

COVID-19の発生は、建設産業に短期的・長期的ないくつかの影響をもたらし、建設用接着剤とシーラントの需要に影響を及ぼす可能性が高いです。全米ゼネコン協会(AGC)によると、作業の中断やプロジェクトの中止があり、オフィス、娯楽施設、スポーツ施設などの「非本質的」プロジェクトでは需要が減少する可能性があります。こうしたプロジェクトやその他の建設活動の停止により、建設用接着剤の需要は縮小する傾向にあります。

主要ハイライト

- 短期的には、新興国における住宅・建設プロジェクトの増加や建設産業への投資の増加が市場を牽引する主要要因となっています。

- しかし、排出ガスに関する厳しい環境規制が市場の成長を抑制する可能性が高いです。

- 建設セグメントでのバイオベースとハイブリッド接着剤への需要の増加と、グリーン建設への接着剤の貢献は、将来的に市場に機会を創出する可能性が高いです。

建設用接着剤市場の動向

市場を独占する住宅セグメント

- 住宅建設では、カーペットの敷設、カウンターのラミネート、フローリングの設置、壁紙の貼り付けなど、接着剤にはいくつかの用途セグメントがあります。接着剤を使用することで、ネジの使用を減らし、住宅の耐候性を高めることができます。

- 世界中の住宅建設は、人口増加、農村部からサービス業クラスターへの移行、核家族の増加傾向などの要因のために、過去数年間で大幅な成長を示しています。また、人口に対する土地の比率の低下や、高層住宅やタウンシップの建設動向の高まりが、世界中の住宅建設セグメントにおける接着剤の適用を促進しています。

- 世界的に、住宅需要を満たすための供給が大幅に不足しています。これは、開発を進めるために代替工法や新たなパートナーシップを採用する投資家や開発者にとって大きな機会となりました。

- Oxford Economicsの推定によると、2020年の世界の建設生産高は10兆7,000億米ドルで、2020~2030年にかけて42%増の4兆5,000億米ドル、15兆2,000億米ドルに達すると予想されています。例えば

- 米国では、World Construction Todayによると、全米ゼネコン協会(AGC)が連邦政府のデータを評価した結果、多くタイプの商業建設に対する需要は当面堅調に推移すると判断しました。

- インターナショナル・コンストラクションによると、中国政府は、パンデミックからの地域経済の回復を支援するため、2023年から大規模な建設インフラプロジェクトへの支出を前年比1兆8,000億米ドル増加させる予定です。

- カナダでは、アフォーダブル・ハウジング・イニシアチブ(AHI)、ニュー・ビルディング・カナダ・プラン(NBCP)、メイド・イン・カナダなど、さまざまな政府プロジェクトがこのセクターの拡大を支えています。

- ユーロ統計によると、2023年2月の建設生産は、2023年1月に比べ、ユーロ圏(EA20)で2.3%、EU-27で2.1%増加しました。

- 以上のような要因から、世界の建設産業は成長すると予想されるため、建設用接着剤の需要も増加すると見込まれます。

市場を独占するアジア太平洋

- アジア太平洋は、インド、中国、東南アジア各国の建設市場からの莫大な需要により、建設用接着剤の最大市場を占めています。

- この地域の商業オフィスやビルの数は、主要な経済ビジネスの中心地の成長と、魅力的な外観と持続可能で経済的な建設を求める建設業者間の競争により、過去10年来増加しています。

- 中国の建設産業が急速に開発されたのは、経済成長を維持する手段として中央政府が建設産業への投資を推し進めたためです。

- 中国国家統計局によると、中国の建設産業は2022年に約8兆3,000億元(1兆1,800億米ドル)の付加価値を生み出しました。

- 中国政府は、経済をよりサービス重視の形態にリバランスさせようと努力しているにもかかわらず、今後10年間で2億5,000万人を新たな巨大都市に移住させるなど、大規模な建設計画を展開しました。

- India Brand Equity Foundation(IBEF)によると、インドの建設産業は、2025年までに約1兆米ドルの規模を持つ世界第3位の市場に成長するといいます。

- 国土交通省(日本)によると、2022年に日本で着工された住宅戸数は約85万9,500戸です。経済調査会によると、2023年4月時点の日本の建設資材月次価格指数は147.8です。

- これらの要因がアジア太平洋の建設用接着剤市場を牽引すると予想されます。

建設用接着剤産業概要

世界の建設用接着剤市場は統合的な性格を持っています。主要参入企業には、Henkel Adhesives Technologies India Private Limited、Dow、H.B. Fuller、Arkema Group、3Mなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設産業への投資拡大

- 新興国における住宅・建設プロジェクトの増加

- その他の促進要因

- 抑制要因

- 厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ

- 水性

- 溶剤型

- ホットメルト

- 反応性

- その他

- 用途

- 住宅

- 商業

- インフラ

- 産業・施設

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析**/市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Adhesives Technology Corporation(ATC)

- Ashland

- Avery Dennison Corporation

- Bostik

- Don Construction Products Limited

- Dow

- Franklin International

- Gorilla Glue Inc.

- H.B. Fuller Company

- Henkel Adhesives Technologies India Private Limited

- Huntsman International LLC

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

第7章 市場機会と今後の動向

- 建設産業におけるバイオベース接着剤とハイブリッド接着剤の需要増加

- グリーンコンストラクションに貢献する接着剤

The Construction Adhesives Market is expected to register a CAGR of 6.1% during the forecast period.

The outbreak of COVID-19 brought several short-term and long-term consequences in the construction industry, which is likely to affect the demand for construction adhesives and sealants. According to the Associated General Contractors of America (AGC), there were disruptions to work or canceled projects, and the demand may be potentially less for 'non-essential' projects, like offices, entertainment, and sports facilities. Due to the shutdown of such projects and other construction activities, the demand for construction adhesives tends to constrain.

Key Highlights

- In the short term, major factors driving the market studied are the increase in housing and construction projects in emerging countries and increasing investments in the construction industry.

- However, stringent environmental regulations related to emissions will likely restrain the market's growth.

- Increasing demand for bio-based and hybrid adhesives in the construction sector and adhesive contribution to green construction is likely to create opportunities for the market in the future.

Construction Adhesives Market Trends

Residential Segment to Dominate the Market

- In residential construction, adhesives have several application areas like carpet laying, laminating countertops, installing flooring, wallpapering, etc. The use of adhesives can reduce the usage of screws and help in weatherproofing the house.

- Residential construction across the globe has been witnessing significant growth over the past few years owing to factors like population growth, migration from rural areas to service sector clusters, and the growing trend of nuclear families. Besides, the decreasing land-to-population ratio and the growing trend of constructing high-rise residential buildings and townships have been driving the application of adhesives in the residential construction segment across the globe.

- Globally, there has been a significant undersupply to meet the demand for housing. This presented a major opportunity for the investors and developers to embrace alternative construction methods and new partnerships to bring forward development.

- According to Oxford Economics Estimates, in 2020, the global construction output was USD 10.7 trillion and is expected to grow by 42% or USD 4.5 trillion between 2020 and 2030 to reach USD 15.2 trillion. For instance:

- In the United States, according to World Construction Today, the Associated General Contractors of America's- AGC evaluation of the federal data determined that the demand for numerous kinds of commercial construction will remain strong for the immediate future.

- According to International Construction, the Chinese government is set to increase its spending on large construction and infrastructure projects by USD 1.8 trillion year-on-year starting from 2023 to help regional economies recover from the pandemic.

- Various government projects in Canada, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, have supported the sector's expansion.

- According to Eurostat, in February 2023, construction production increased by 2.3% in the euro area (EA20) and 2.1% in EU-27 compared to January 2023.

- Due to all the factors above, the global construction industry is expected to grow, so the demand for construction adhesives is also expected to increase.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounted for the largest market for construction adhesives, owing to huge demand from the construction market in India, China, and various countries in Southeast Asia.

- The number of commercial offices and buildings in the region has increased since the last decade, owing to major economic and business centers' growth and competition among the construction players for attractive looks and sustainable and economical construction.

- China's construction industry developed rapidly due to the central government's push for investment in the construction industry as a means to sustain economic growth.

- China's construction industry generated an added value of around 8.3 trillion yuan (USD 1.18 trillion) in 2022, according to the National Bureau of Statistics of China.

- The Chinese government rolled out massive construction plans, including making provision for the movement of 250 million people to its new megacities over the next ten years, despite efforts to rebalance its economy to a more service-oriented form.

- According to the India Brand Equity Foundation (IBEF), India's construction industry is set to emerge as the third-largest market in the world, with a size of almost USD 1 trillion by 2025.

- According to MLIT (Japan), around 859.5 thousand housing units were initiated in Japan in 2022. According to the Economic Research Association, as of April 2023, Japan's construction materials monthly price index stood at 147.8.

- These factors are expected to drive the construction adhesives market in the Asia-Pacific region.

Construction Adhesives Industry Overview

The global construction adhesive market is consolidated in nature. Some of the major players include Henkel Adhesives Technologies India Private Limited, Dow, H.B. Fuller, Arkema Group, and 3M.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Investments in the Construction Industry

- 4.1.2 Increase in Housing and Construction Projects in Emerging Countries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-melt

- 5.1.4 Reactive

- 5.1.5 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Adhesives Technology Corporation (ATC)

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Bostik

- 6.4.6 Don Construction Products Limited

- 6.4.7 Dow

- 6.4.8 Franklin International

- 6.4.9 Gorilla Glue Inc.

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel Adhesives Technologies India Private Limited

- 6.4.12 Huntsman International LLC

- 6.4.13 MAPEI S.p.A.

- 6.4.14 RPM International Inc.

- 6.4.15 Sika AG

- 6.4.16 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase In Demand for Bio-based and Hybrid Adhesives in the Construction Industry

- 7.2 Adhesives Contribute to Green Construction