|

市場調査レポート

商品コード

1692578

建設用接着剤とシーリング剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 建設用接着剤とシーリング剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 339 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

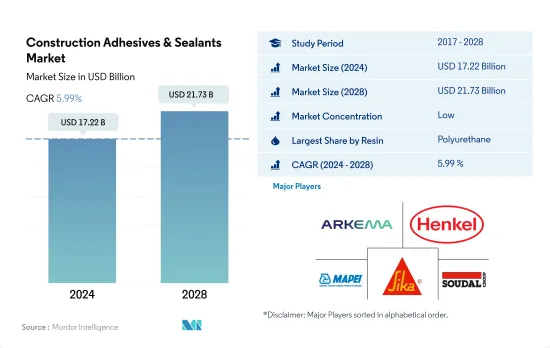

建設用接着剤とシーリング剤の市場規模は2024年に172億2,000万米ドルと推定・予測され、2028年には217億3,000万米ドルに達し、予測期間(2024~2028年)のCAGRは5.99%で成長すると予測されます。

建設用接着剤とシーリング剤の成長を支えるインフラプロジェクト

- 世界的には、ポリウレタン樹脂、アクリル樹脂、シリコーン樹脂、ポリサルファイド樹脂をベースとする接着剤とシーリング剤が最も顕著です。これらの製品に対する世界需要は、アジア太平洋と欧州における建設活動の減少により、2017~2019年にかけて成長が鈍化しました。これら2つの地域の需要は、この期間にそれぞれ-1.82%と0.73%のCAGRを記録しました。建設用接着剤とシーリング剤の需要は、COVID-19の流行による原料や作業員の不足などにより、2020年にはすべての地域で減少しました。全樹脂の中で、シアノアクリレート樹脂をベースとする接着剤の需要が最悪の打撃を受け、2019年比で6.19%減少しました。

- 2021年には規制が緩和され、建築用接着剤とシーリング剤の需要は急速に流行前の水準に回復しました。オーストラリアにおけるホームビルダープログラムのような支援制度が、需要拡大に重要な役割を果たしました。この成長動向は予測期間を通じて続くと予想され、建設用接着剤とシーリング剤の需要は予測期間2022~2028年にCAGR 4.13%を記録すると予想されます。

- アクリル樹脂をベースとする建築用接着剤とシーリング材は、その強力な結合力により、すべての樹脂の中で最大の需要シェアを占めています。アクリル樹脂の需要シェアは予測期間中最も高いままであると予想されます。予測期間中、シリコーン樹脂ベースの建築用接着剤とシーリング剤の需要成長がアクリル樹脂ベースの建築用接着剤とシーリング剤の需要成長を上回ると予想されます。

アジア太平洋の建設セクタからの需要の高まりが、接着剤とシーリング剤の世界売上高を牽引する見込み

- アジア太平洋は、中国、日本、韓国、インド、オーストラリア、その他の国々で多くの建設活動が行われているため、調査期間を通じて建設用接着剤とシーリング剤の需要で最大のシェアを占めています。中国は世界最大の建設市場であり、同国の人口の多さと都市化の進展により、アジア太平洋の需要の最大71%を生み出しています。

- 2017~2019年にかけては、アルゼンチンなどの国の中央銀行による金融市場のボラティリティ上昇と金利上昇のため、欧州と中南米の一部の国で建設活動が減少したため、建設用接着剤とシーリング剤の需要は低迷しました。

- 2020年には、建設用接着剤とシーリング剤の需要が数カ国で最大27%減少したが、南アフリカやブラジルなど一部の国では建設活動が不可欠とみなされていたため、世界の影響は深刻ではありません。ロシアのように、パンデミック後に建設現場が最初に再開された国もいくつかありました。こうした要因がCOVID-19パンデミックの世界市場への影響を緩和し、減少幅を7.6%に抑えました。

- 2021年には、米国、オーストラリア、EU諸国などの救済策や支援制度により、建設活動は急速にパンデミック前の水準に達し、建設用接着剤とシーリング剤の需要を押し上げました。インフラ建設用接着剤とシーリング剤は、欧州、南米、アジア太平洋諸国における投資と予算配分の増加により、予測期間中に他の建設用接着剤とシーリング剤タイプの中で最大の成長を示すことが期待されています。

世界の建設用接着剤とシーリング剤の市場動向

住宅とインフラ開発の拡大による建設セクタの繁栄

- 建築・建設産業は着実な成長を示し、2017~2019年のCAGRは2.6%でした。この成長は、世界の経済活動の上向きと一戸建て住宅の需要増加が原動力となっています。2020年、COVID-19パンデミックは世界の建築・建設産業に大きな影響を与えました。労働力供給の制約、建設財政とサプライチェーンの混乱、経済の不確実性が世界の建築・建設産業にマイナスの影響を与えました。

- 2021年にはプラス成長を示したもの、パンデミックによるサプライチェーンへの影響は原料価格の高騰を招き、いまだ産業を悩ませています。しかし、建設産業は国の経済に大きな影響を与えるため、北米、アジア太平洋の国々は、支援制度を提供することで、経済サイクルを再起動させるために建設産業を利用してきました。支援制度には、オーストラリアのホームビルダープログラムやEU諸国の景気回復計画などがあります。

- アジア太平洋は、建設活動量が最も多く、中国、インド、日本、インドネシア、韓国などの国々における膨大な人口、都市化の進展、インフラ開拓への投資の増加により、2028年まで最大の建設市場であり続けると予想されます。

- グリーンビルディングの重視が高まり、世界の建設活動からの排出を削減する取り組みが進むことで、予測期間中、よりサステイナブル運営手順が実現すると予想されます。例えばフランスは、低炭素エネルギー経済への転換を図るため、建設産業に75億ユーロの予算を計上しています。

建設用接着剤とシーリング剤産業概要

建設用接着剤とシーリング剤市場は細分化されており、上位5社で27.89%を占めています。この市場の主要企業は、Arkema Group、Henkel AG & Co. KGaA、MAPEI S.p.A.、Sika AG、Soudal Holding N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 建築・建設

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- 中国

- EU

- インド

- インドネシア

- 日本

- マレーシア

- メキシコ

- ロシア

- サウジアラビア

- シンガポール

- 南アフリカ

- 韓国

- タイ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

- 技術

- ホットメルト

- 反応性

- シーリング剤

- 溶剤型

- 水性

- 地域

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他のアジア太平洋

- 欧州

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他の欧州

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- アルゼンチン

- ブラジル

- その他の南米

- アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Aica Kogyo Co..Ltd.

- Arkema Group

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- MAPEI S.p.A.

- Momentive

- RPM International Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤とシーリング剤産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92415

The Construction Adhesives & Sealants Market size is estimated at 17.22 billion USD in 2024, and is expected to reach 21.73 billion USD by 2028, growing at a CAGR of 5.99% during the forecast period (2024-2028).

Infrastructure projects to support the growth of construction adhesives and sealants

- Globally, the most prominent are adhesives and sealants based on polyurethane, acrylic, silicone, and polysulphide resins. Global demand for these products witnessed slow growth during 2017-2019 due to a decline in construction activities in the Asia-Pacific and European regions. The demand from these two regions recorded CAGRs of -1.82% and 0.73%, respectively, in this period. The demand for construction adhesives and sealants declined in 2020 from all regions due to a shortage of raw materials, workers, and other factors due to the COVID-19 pandemic. Among all resins, the demand for adhesives based on cyanoacrylate resins took the worst hit and declined by 6.19% compared to 2019.

- In 2021, as restrictions eased, the demand for construction adhesives and sealants quickly rebounded to the pre-pandemic levels. Support schemes like the Homebuilder program in Australia played a crucial role in the demand growth. This growth trend is expected to continue throughout the forecast period, and the demand for construction adhesives and sealants is expected to record a CAGR of 4.13% during the forecast period 2022-2028.

- Construction adhesives and sealants based on acrylic resin occupied the largest share of the demand among all resins because of their strong bonds. The demand share for acrylic resins is expected to remain the highest during the forecast period. The demand growth for silicone resin-based construction adhesives and sealants is expected to outpace the demand growth for acrylic resin-based construction adhesives and sealants over the forecast period.

Inflating demand from Asia-Pacific's construction sector likely to drive the global sales of adhesive and sealants

- Asia-Pacific accounted for the largest share of the demand for construction adhesives and sealants throughout the study period because of the large number of construction activities in China, Japan, South Korea, India, Australia, and other countries in the region. China has the largest construction market globally and generates up to 71% of the demand from Asia-Pacific due to the country's large population and increasing urbanization.

- In 2017-2019, the demand for construction adhesives and sealants was sluggish due to a decline in construction activities in a few countries in Europe and South America because of the increased volatility of financial markets and increased interest rates by central banks of countries like Argentina.

- In 2020, the demand for construction adhesives and sealants declined by up to 27% in a few countries, but the global impact was not severe as construction activities were deemed essential in a few countries like South Africa and Brazil, among others. In a few countries, like Russia, construction sites were the first to reopen after the pandemic. These factors cushioned the COVID-19 pandemic's impact on the global market, restricting the decline to 7.6%.

- In 2021, due to relief packages and support schemes in countries like the United States, Australia, and EU countries, construction activities quickly reached their pre-pandemic levels, thus boosting the demand for construction adhesives and sealants. Infrastructure construction adhesives and sealants are expected to witness the largest growth among other construction adhesives and sealants types during the forecast period because of increased investments and budget allotments in European, South American, and Asia-Pacific countries.

Global Construction Adhesives & Sealants Market Trends

Growing residential and infrastructural development to thrive the construction sector

- The building and construction industry witnessed steady growth, with a CAGR of 2.6% from 2017 to 2019. This growth was driven by the upswing in global economic activity and increasing demand for single-family homes. In 2020, the COVID-19 pandemic had a major impact on the global building and construction industry. Constraints in labor supply, disruptions in construction finances and the supply chain, and economic uncertainty negatively impacted the global building and construction industry.

- Though the industry showed positive growth in 2021, the pandemic's effect on supply chains, which resulted in a hike in raw material prices, is still plaguing the industry. However, as the construction industry heavily influences a nation's economy, countries in Europe, North America, and Asia-Pacific have used the construction industry to restart their economic cycles by offering support schemes. Some support schemes include the Homebuilder Programme in Australia and the economic recovery plan of EU countries.

- The Asia-Pacific region experiences the highest volume of construction activities, and it is expected to remain the largest construction market till 2028 due to its huge population, increasing urbanization, and increasing investments in infrastructural development in countries like China, India, Japan, Indonesia, and South Korea.

- Increasing emphasis on green buildings and efforts to reduce emissions from global construction activities are expected to result in more sustainable operational procedures during the forecast period. For example, France has sanctioned EUR 7.5 billion for the construction industry to transform itself into a low-carbon energy economy.

Construction Adhesives & Sealants Industry Overview

The Construction Adhesives & Sealants Market is fragmented, with the top five companies occupying 27.89%. The major players in this market are Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 Water-borne

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co..Ltd.

- 6.4.3 Arkema Group

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 Illinois Tool Works Inc.

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Momentive

- 6.4.11 RPM International Inc.

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Sika AG

- 6.4.14 Soudal Holding N.V.

- 6.4.15 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms