|

市場調査レポート

商品コード

1692580

欧州の建設用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の建設用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 199 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

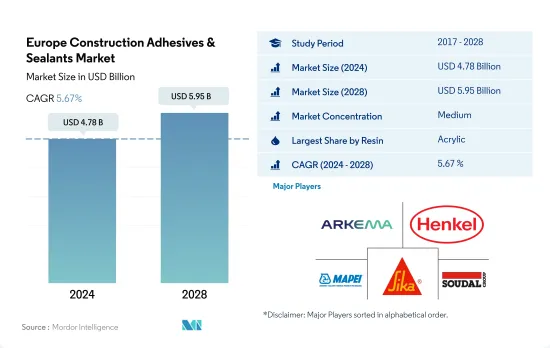

欧州の建設用接着剤とシーラント市場規模は2024年に47億8,000万米ドルと推定・予測され、2028年には59億5,000万米ドルに達し、予測期間(2024-2028年)のCAGRは5.67%で成長すると予測されます。

欧州の建設用接着剤とシーラントの成長を支える政府の政策とイニシアティブ

- 建設業界では、カーペットの敷き詰め、床材、木材、プレハブパネルの接合、壁の被覆、ウェザーシール、屋根などの目的で接着剤とシーラントが必要とされます。EURO CONSTRUCTのレポートによると、建設業界は西欧で2022~2024年のCAGRが6.1%、中東欧で2022~2024年のCAGRが6.4%を記録すると予想されています。このため、予測期間中に建設用接着剤とシーラントの需要が増加することが予想されます。

- 欧州委員会は、エネルギー効率指令(Energy Efficiency Directive)や建設物のエネルギー性能(Energy Performance of Buildings)などの枠組みにより、住宅インフラをエネルギー効率の高いデジタル資源性能に移行させる政策を策定しています。こうした取り組みにより、既存の建物の改修が必要となり、予測期間2022~2028年には建設に必要な接着剤とシーラントの需要増につながります。

- 屋根材、床材、窓の取り付けなど、さまざまな用途の建設産業で使用されるファスナーは、優れた強度を保持する建設用接着剤とシーラントで防ぐことができる故障が発生しやすいです。建設における効率的な資源計画の開発により、建設用接着剤とシーラントの需要は2022-2028年に増加すると予想されます。

- アクリル樹脂は、機械的接合や異なる基材との接着剤として、また収縮しやすい材料のシーラントとして幅広く使用されているため、2021年時点で欧州の建設用接着剤とシーラント市場の金額シェアで最大のシェアを占めています。これらの用途により、接着剤とシーラントは建設業界で広く使用されており、予測期間中に需要が拡大すると予想されます。

アイルランド、スペイン、スロバキアの建設生産高増加が建設用接着剤とシーラントの需要を高める

- 2020年、建設生産高が全体的に4.4%減少したのは、COVID-19パンデミックが欧州全土に広がり、全国的なロックダウン、サプライチェーンの混乱、社会的距離の強制規制等につながったためです。これらの要因により、2020年の建設に必要な接着剤とシーラントの需要は減少しました。その他欧州の地域セグメントでは、建設生産高が前年比16.8%減を記録したスロバキアなどの国々で大規模な景気後退が発生したため、減少幅は最大となりました。

- 建設用接着剤とシーラントの需要は2021年に大幅に増加したが、これは、次世代EUのような2020年のCOVID-19による全体的な景気減速に対するEU委員会の回復計画のためです。建設用接着剤とシーラントの需要における全体的な成長は、デンマークなどの北欧諸国が前年比17.8%増を記録したため、その他欧州セグメントの2021年が最も高かったです。

- 欧州の建設用接着剤とシーラント市場における金額シェアは、その他欧州セグメントが最も高く、シェアの半分近くを占めています。これは、アイルランドなどの国々の建設生産高全体が2021年に15.1%、次いでスペインが14.3%、スロバキアが13.5%の成長が見込まれるためです。

欧州の建設用接着剤とシーラント市場動向

改修ニーズの高まりとともに新築の急増が業界を牽引

- 2020年の建設業全体の収益は、COVID-19によるパンデミック状況の影響から急減を示し、全体的な回復の鈍化と作業現場における社会的距離の措置につながりました。

- 欧州の建設セクター全体の売上高は驚異的な伸びを示し、2021年の前年比成長率は2020年に比べて最も高くなりました。これは、「次世代EU」と名付けられたCOVID復興計画の下、全セクターに7,500億ユーロを投入するなどのEU委員会の取り組みや対策が奏功したためです。次世代EU計画では、建設物のグリーン化とデジタル化という欧州の目標が既存の建設物や構造物の年間改修率の増加につながったため、建設部門が最大の投資を受けました。

- EUROCONSTRUCTの報告書によると、EUの政治的地域に基づくセグメントのうち、中東欧のCAGRは6.4%、次いで西欧のCAGRは6.1%と予想されています。

- 欧州連合(EU)および国家レベルの政策立案者は、「建設物のエネルギー性能に関する指令(Energy Performance of Buildings Directive)」をはじめとするさまざまな政策を通じて、新規建設物の建設や既存建設物のエネルギー効率化を優先しています。こうした政策により、予測期間中の建設全体の収益が増加するとみられます。

欧州の建設用接着剤とシーラント産業の概要

欧州の建設用接着剤とシーラント市場は、上位5社で51.69%を占め、適度に統合されています。この市場の主要企業は以下の通り。 Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 建設・建設

- 規制の枠組み

- EU

- ロシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

- テクノロジー

- ホットメルト

- 反応性

- シーラント

- 溶剤型

- 水性

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Construction Adhesives & Sealants Market size is estimated at 4.78 billion USD in 2024, and is expected to reach 5.95 billion USD by 2028, growing at a CAGR of 5.67% during the forecast period (2024-2028).

Government policies and initiatives to support the growth of construction adhesives and sealants in Europe

- The construction industry requires adhesives and sealants for purposes such as carpet layering, flooring, timber, prefabricated panels joining, wall covering, weather-sealing, and roofing. The construction industry is expected to record a 6.1% CAGR in 2022-2024 in Western Europe and a 6.4% CAGR in 2022-2024 in Central and Eastern Europe, per the EURO CONSTRUCT report. This is expected to increase demand for construction adhesives and sealants in the forecast period.

- The European Commission has framed policies to transit the residential infrastructure to energy-efficient and digital resource performance with frameworks such as the Energy Efficiency Directive and Energy Performance of Buildings. These initiatives will require the renovation of existing buildings, leading to an increase in demand for adhesives and sealants required for construction in the forecast period 2022-2028.

- The fasteners used in the construction industry for different applications, such as roofing, flooring, and window fitting, are prone to failures that can be prevented with good strength holding construction adhesives and sealants. With the development of efficient resource planning in construction, the demand for construction adhesives and sealants is expected to increase in the period 2022-2028.

- Acrylic resin accounted for the maximum share of the European construction adhesives and sealants market value share as of 2021 because of its wide usage as an adhesive for mechanical joining and with different substrates and as a sealant for materials prone to shrinkage. These applications make them widely used in the construction industry, and their demand is expected to grow over the forecast period.

Rising construction output from Ireland, Spain, and Slovakia to raise the demand for construction adhesives and sealants

- In 2020, the overall decline in construction output by 4.4% was due to the COVID-19 pandemic spreading across Europe, which led to nationwide lockdowns, supply chain disruptions, mandatory social distancing regulations, etc. These factors led to declining demand for adhesives and sealants required for construction in 2020. The decline was maximum for the Rest of Europe regional segment because of the huge recessions in countries such as Slovakia, which recorded a 16.8% Y-o-Y decline in its construction output.

- The demand for construction adhesives and sealants increased tremendously in 2021 because of the EU Commission's recovery plan for an overall economic slowdown due to COVID-19 in 2020 such as Next Generation EU, in which the maximum fund allocation was done for the construction sector to make European buildings environmentally benign with decreased wastage of resources. The overall growth in demand for construction adhesives and sealants was highest in 2021 for the Rest of Europe segment because of Nordic countries, such as Denmark, which registered a growth of 17.8% Y-o-Y in construction output.

- The value share in the European construction adhesives and sealants market is highest for the Rest of Europe segment, which accounts for nearly half of the share because the overall construction output from countries such as Ireland is expected to grow by 15.1%, followed by Spain with 14.3%, and Slovakia with 13.5%, as published in a report by EURO CONSTRUCT in 2021.

Europe Construction Adhesives & Sealants Market Trends

Rapid growth of new construction along with rising need for renovation activities will drive the industry

- The overall revenue of construction showed a steep decrement in 2020 because of the impact of the pandemic situation due to COVID-19, which led to an overall recovery slowdown and social distancing measures on work sites.

- The overall revenue of the construction sector in Europe grew tremendously, with the highest year-on-year growth in 2021 compared to that of 2020 because of the initiatives and measures taken by the EU Commission, such as the infusion of EUR 750 billion for all sectors under the COVID recovery plan named Next Generation EU. Under the Next Generation EU plan, the construction sector received the maximum investment because of the European objective of green and digital transition in buildings which led to growth in the annual renovation rate of existing buildings and structures.

- As per the EUROCONSTRUCT report, among the segments of the European Union based on political geography, Central and Eastern Europe are expected to register a CAGR of 6.4%, followed by Western Europe at a CAGR of 6.1% in 2022-2024.

- The policymakers at European Union and national level are prioritizing the construction of new buildings and conversion of existing buildings to be energy efficient through various policies including Energy Performance of Buildings Directive and others. These policies will lead to an increase in overall revenue for construction in the forecast period.

Europe Construction Adhesives & Sealants Industry Overview

The Europe Construction Adhesives & Sealants Market is moderately consolidated, with the top five companies occupying 51.69%. The major players in this market are Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 H.B. Fuller Company

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Illinois Tool Works Inc.

- 6.4.6 MAPEI S.p.A.

- 6.4.7 RPM International Inc.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms