アジア太平洋地域の建設用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia-Pacific Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 219 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692579

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

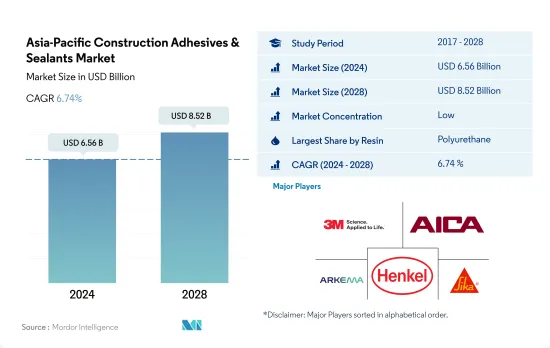

アジア太平洋地域の建設用接着剤とシーラント市場規模は、2024年に65億6,000万米ドルと推定され、2028年には85億2,000万米ドルに達すると予測され、予測期間中(2024~2028年)のCAGRは6.74%で成長する見込みです。

中国と日本の建設用接着剤とシーラントの成長を支えるインフラ・プロジェクト

- ポリウレタンおよびアクリル樹脂ベースの接着剤とシーラントは、過去期間(2017~2021年)および基準年(2021年)において、他の樹脂タイプの中で最も使用されています。これらの樹脂は強力な接着力と構造用接着剤としての適用性から、予測期間中最も使用される樹脂タイプになると予想されます。アジア太平洋では、2021年にアクリル系建設接着剤の約49%が水性技術で製造され、ポリウレタン系は主にシーラント技術で製造されました。

- 地域別では、2019~20年の間に、建設用接着剤とシーラントの需要は約13%成長し、予測期間(2022~2028年)には約4.6%の成長が見込まれます。すべての樹脂タイプの中で、シリコーン樹脂ベースの接着剤とシーラントは、予測期間(2022年~2028年)に約5%の最大のCAGRで推移すると予想されます。

- 建設用接着剤とシーラントの世界需要では、中国が最大のシェアを占めています。2021年、中国から生み出された需要は12億キログラムであり、2028年までにCAGR 6.9%で18億キログラムに達すると予想されます。ポリウレタン、アクリル、シリコン樹脂ベースの接着剤とシーラント製品は、中国の建設業界が生み出す総需要の50%以上を占めると予想されます。日本は建設用接着剤の第2位の消費国であり、2021年のシェアは約12%で、予測期間(2022~2028年)のCAGRは約2.7%と予想されます。日本では超高層ビルや高層ビルの建設プロジェクトが増加しており、これが接着剤需要の主な要因となっています。

建設投資の増加が将来の接着剤とシーラントの需要を押し上げる可能性が高いです。

- アジア太平洋は建設用接着剤の活況市場です。COVID-19パンデミックがアジア太平洋諸国に影響を及ぼしたため、2020年前半には建設・不動産活動が減速したもの、2021年には急速に回復し、予測期間2022-2028年を通じて堅調な成長を維持すると予想されます。アジア太平洋地域は最も重要な建設・不動産市場となり、2030年までに世界の生産額の約40%を占めると予想されます。

- 予測期間2022-2028年には、中国が世界の建設・不動産業界をリードし、地域の成長に拍車をかけると予想されます。数十年にわたる中国のインフラ拡張への多額の投資、急増する都市人口、国内の産業施設への大規模な外国直接投資(FDI)が、中国の建設部門の台頭に大きく寄与しています。COVID-19の発生により、中国は2020年上半期に住宅・非住宅建設物の落ち込みに見舞われたが、消費者と企業の信頼が回復したため急速に回復しました。金属や木材を含む建設資材価格の世界の高騰に伴い、中国の建設企業は製造コストの大幅な上昇を目の当たりにしているが、それでも最終顧客にはこうしたコストを転嫁できています。

- COVID-19パンデミック後の建設・不動産業界の復活には、政府のインフラ投資が欠かせないです。中国、インド、日本、その他の地域リーダーで計画されている大規模投資は、アジア太平洋市場の成長を短期から中期にかけて押し上げると予想されます。このような要因はすべて、予測期間中に地域全体の建設用接着剤とシーラントの需要を増加させると予想されます。

アジア太平洋地域の建設用接着剤とシーラントの市場動向

インフラ活動拡大のための投資増が業界規模を拡大

- アジア太平洋地域は、中国、日本、インドといった世界の主要経済国によって牽引されています。中国は継続的な都市化のプロセスを推進中で、2030年の目標率は70%です。都市化の進展によって都市部で必要とされる居住スペースが増加し、都市部の中間所得層が生活環境の改善を望むようになることで、住宅市場に影響を与え、それによって国内の住宅建設が増加する可能性があります。

- 非住宅インフラは大幅に拡大する可能性が高いです。中国政府は2019年に約1,420億米ドルに相当する26のインフラプロジェクトを承認し、2023年に完了する予定です。同国は世界最大の建設市場を有しており、全世界の建設投資の20%を占めています。2030年までに、政府は13兆米ドルを超える建設投資を計画しています。このため、建設市場は予測期間中(2022~2028年)に4.48%のCAGRで推移すると予想されます。

- 建設産業はアジア太平洋地域最大の産業の1つであり、2019年には有望な成長を記録しました。同地域はベトナム、マレーシア、インドネシア、タイ、その他の南アジア諸国など多くの新興諸国を構成しているため、同産業は成長を続けています。しかし、COVID-19パンデミックのために、建設部門は、インド、中国、日本、ASEAN諸国を含む発展途上国に深刻な影響を与えた地域全体の政府によるロックダウンのために大幅な減少を示しました。

- アジア太平洋地域でも、建設分野への海外投資家の関心が高まっています。発展途上諸国が投資家により良い利益と機会を提供するため、建設開発セクターへの外国直接投資(FDI)が増加しています。

アジア太平洋地域の建設用接着剤とシーラント産業の概要

アジア太平洋の建設用接着剤とシーラント市場は断片化されており、上位5社で17.60%を占めています。この市場の主要企業は以下の通りです。 3M, Aica Kogyo, Arkema Group, Henkel AG & Co. KGaA and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 建設・建設

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

- テクノロジー

- ホットメルト

- 反応性

- シーラント

- 溶剤型

- 水性

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Aica Kogyo Co..Ltd.

- Arkema Group

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- THE YOKOHAMA RUBBER CO., LTD.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92416

The Asia-Pacific Construction Adhesives & Sealants Market size is estimated at 6.56 billion USD in 2024, and is expected to reach 8.52 billion USD by 2028, growing at a CAGR of 6.74% during the forecast period (2024-2028).

Infrastructure projects to support the growth of construction adhesives and sealants in China and Japan

- Polyurethane and Acrylic resin-based adhesives and sealants are the most used among other reins types during the historical period, 2017-2021, and base year, 2021. They are expected to be the most used resin types during the forecast period because of the strong bonds and their applicability as structural adhesives. In Asia-Pacific, about 49% of the acrylic-based construction adhesives were manufactured in water-borne technology in 2021 and polyurethane based products were manufactured majorly in sealant technology.

- Regionally, during 2019-20, the demand for construction adhesives and sealants grew by about 13% and is expected to grow by about 4.6% during the forecast period (2022 - 2028). Among all the resin types, silicone resin-based adhesives and sealants are expected to register the largest CAGR of around 5% during the forecast period (2022 - 2028).

- China occupied the largest share of the demand for construction adhesives and sealants globally. In 2021, the demand generated from China was 1.2 billion kilograms and the demand is expected to reach 1.8 billion kilograms with a CAGR of 6.9% by 2028. Polyurethane, acrylic, and silicon resin-based adhesives and sealants products are expected to occupy more than 50% of the total demand generated by China's construction industry. Japan is the second-largest consumer of construction adhesives, and it had about 12% of shares in 2021, is expected to register a CAGR of about 2.7% during the forecast period (2022 - 2028). Japan is seeing an increased number of skyscraper and high-rise building projects, which has been the major source of the demand for adhesives.

Rising construction investments likely to propel the demand for adhesives & sealants in the future

- Asia-Pacific is a booming market for construction adhesives. Despite a slowdown in construction and real estate activities during the first half of 2020 as the COVID-19 pandemic affected Asia-Pacific countries, the area rebounded fast in 2021 and is expected to maintain solid growth throughout the forecast period 2022-2028. The Asia-Pacific region is expected to be the most important construction and real estate market, accounting for roughly 40% of global production value by 2030.

- Over the forecast period 2022-2028, China is expected to be the leading global construction and real estate industry, fueling regional growth. Decades of substantial Chinese investments in infrastructure expansions, a fast-rising urban population, and extensive foreign direct investment (FDI) into industrial facilities in the nation have contributed significantly to the rise of the Chinese construction sector. Due to the COVID-19 outbreak, China suffered a drop in residential and non-residential buildings in the first half of 2020 but recovered quickly as consumers' and corporate confidence returned. With the global surge in building material prices, including metals and wood, Chinese construction businesses are seeing a significant increase in manufacturing costs but are still able to pass these costs on to final customers.

- Government infrastructure investment is critical to the building and real estate industries' revival following the COVID-19 pandemic. Major investments planned in China, India, Japan, and other regional leaders are expected to boost the Asia-Pacific market's growth in the short to medium term. All such factors are expected to increase the demand for construction adhesives and sealants across the region over the forecast period.

Asia-Pacific Construction Adhesives & Sealants Market Trends

Raising investment to expand infrastructural activities will augment the industry size

- Asia-Pacific is driven by the world's major economies, such as China, Japan, and India. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from increasing urbanization and the desire of middle-income urban residents to improve their living conditions may impact the housing market and, thereby, increase the residential constructions in the country.

- Non-residential infrastructure is likely to expand significantly. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country has the largest construction market globally, accounting for 20% of all worldwide construction investments. By 2030, the government plans to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

- The construction industry is one of the largest industries in Asia-Pacific and recorded promising growth in 2019. The industry continues to grow as the region constitutes many developing countries such as Vietnam, Malaysia, Indonesia, Thailand, and other South Asian countries. However, due to the COVID-19 pandemic, the construction sector witnessed a significant decline owing to lockdowns by governments across the region, which severely affected developing countries, including India, China, Japan, and ASEAN countries.

- The Asia-Pacific region is also witnessing significant interest from international investors in the construction space. Foreign Direct Investment (FDI) in the construction development sector is increasing as developing countries provide better returns and opportunities for investors.

Asia-Pacific Construction Adhesives & Sealants Industry Overview

The Asia-Pacific Construction Adhesives & Sealants Market is fragmented, with the top five companies occupying 17.60%. The major players in this market are 3M, Aica Kogyo Co..Ltd., Arkema Group, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Australia

- 4.2.2 China

- 4.2.3 India

- 4.2.4 Indonesia

- 4.2.5 Japan

- 4.2.6 Malaysia

- 4.2.7 Singapore

- 4.2.8 South Korea

- 4.2.9 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co..Ltd.

- 6.4.3 Arkema Group

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Momentive

- 6.4.7 Shin-Etsu Chemical Co., Ltd.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 THE YOKOHAMA RUBBER CO., LTD.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋地域の建設用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 219 Pages

- 納期

- 2~3営業日