|

市場調査レポート

商品コード

1693377

北米の建築用接着剤・シーラント:市場シェア分析、産業動向、成長予測(2025~2030年)North America Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の建築用接着剤・シーラント:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 196 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

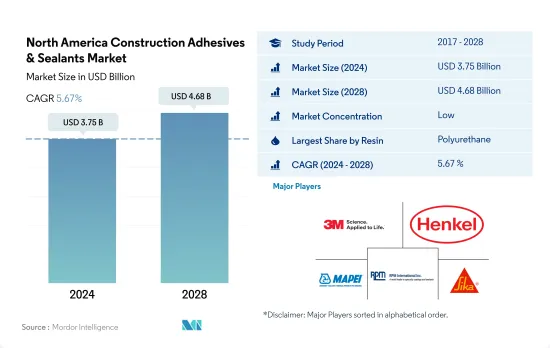

北米の建設用接着剤・シーラント市場規模は2024年に37億5,000万米ドルと推定・予測され、2028年には46億8,000万米ドルに達し、予測期間(2024~2028年)のCAGRは5.67%で成長すると予測されます。

同地域における新設床面積の増加が接着剤・シーラントの需要を牽引

- 樹脂は、特定の用途に使用できる接着剤に、耐紫外線性、耐熱性、引張強度など、必要な物理的特性や化学的特性を付与します。新築面積は、2021年の71億平方フィートから、2022年には74億平方フィートまでの成長が見込まれています。

- 建築用接着剤・シーラントは、2021年に数量ベースで5.8%の急成長を示しました。これは、景気回復、原料の定期的な供給、米国、カナダ、メキシコなど、2020年に発生したCOVID-19の影響を受けた多くの国々での生産施設の再開によるもので、各国でのロックダウンが生産施設の停止を招き、北米での接着剤の着実な成長をもたらしました。

- これらの接着剤は異なる樹脂にセグメント化され、ポリウレタンとアクリル樹脂ベースの接着剤は、建設用途で広く使用されています。これらの接着剤は構造用接着剤として知られ、5~8N/mm2の範囲で高い引張強度を記載しています。そのため、装飾的な床材やセラミックタイルの接着、金属部品のコンクリートへの封入、ドア枠の石積みへの接着、その他多くの用途に使用されています。

- 米国は、同国における住宅と非住宅建設の需要が高まっているため、北米市場の70%近くを占め、建設用接着剤とシーラントの最も高い消費国です。国の新しい建物の建設は、2028年までに71億ユニットに達し、したがって、将来の北米の接着剤とシーラントの需要を促進するであると考えられます。

グリーンイニシアチブの高まりと従来の建物の代替ソリューションが、この地域における建築用接着剤・シーラントの需要を促進します。

- 接着剤・シーラントは北米で主に、接合部の接着やシーリング、建物の内外装、ドアや窓枠のシーリングなど、様々な建設用途向けに生産されています。これらの建設用接着剤とシーラントの生産は、主に北米の建設生産高に依存しています。新しい建物や建築物は、2021年の71億平方メートルから2022年には74億平方メートルに達すると予想されています。

- これらの接着剤とシーラントの生産量は、景気回復と、2020年のCOVID-19パンデミックの影響により貿易交流のための国際国境が閉鎖されていた国々で再開されたことにより、北米のいくつかの国々で生産施設の閉鎖、サプライチェーンの混乱、ロックダウンを引き起こし、同年の成長率が鈍化したため、2021年に突然4,900万トン増加しました。

- 北米では、米国が建設用接着剤・シーラントの消費量で最大を占めています。同国の年間建設産業生産高は1兆4,000億米ドルに達し、GDPの4.2%に寄与しています。多くの多国籍企業を含む国内の100以上のメーカーは、建設産業からの需要の増加に対応するために、これらの接着剤やシーラントを生産しています。同地域で最も急成長している国であり、予測期間2022~2028年のCAGRは5.78%を記録すると予想されています。

- 米国におけるグリーンビルディングの増加、カナダにおける木造住宅の動向、メキシコにおけるプレハブ建築部品の製造増加などが、北米における接着剤・シーラントの需要を牽引すると予想されます。

北米の建築用接着剤・シーラント市場動向

建設産業を支えるインフラ開発に対する政府の取り組み

- 北米は、アジア太平洋、中東・アフリカに次いで建設活動が盛んな第3位の地域です。北米の一人当たりGDPは2万9,010米ドルで、2022年には前年比3.6%の成長が見込まれています。建設産業部門は北米のGDPの7%近くを占めています。北米の建設産業に影響を与える要因は、新規投資、住宅・非住宅建設、政府の施策などです。

- 2020年、建設産業はCOVID-19パンデミックの影響により多くの課題に直面しました。鉄鋼、銅、アルミ、石材、建具などの原料の供給はこの1年間で縮小しました。米国では、世界各国でロックダウンが発生したため、鉄鋼の輸入が2019年の240億米ドルから187億米ドルに減少しました。

- 建築・建設セクタは、貿易交流のための国際国境の再開、サプライチェーンの正規化、その他多くの要因により、2021年には成長率5.6%で再び回復しました。北米では住宅建設が増加しています。例えば、カナダにおける2021年の新設住宅着工戸数は2億7,188万戸で、これは2020年より20%多いです。

- 2022年3月、米国運輸省(USDOT)は、米国再建のためのインフラ(INFRA)プログラムにより、2022~2026年度に72億5,000万米ドルを全州・地域に分配し、国または地域にとって重要な複合一貫輸送貨物・高速道路プロジェクトを建設すると発表しました。これらの要因によって、北米地域の建設活動は将来的に上昇し、2030年までに建設生産高は2.7%変化します。

北米の建設用接着剤・シーラント産業概要

北米の建設用接着剤・シーラント市場は細分化されており、上位5社で36.96%を占めています。この市場の主要企業は、3M、Henkel AG & Co. KGaA、MAPEI S.p.A.、RPM International Inc.、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 建築・建設

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

- 技術

- ホットメルト

- 反応性

- シーラント

- 溶剤型

- 水性

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92432

The North America Construction Adhesives & Sealants Market size is estimated at 3.75 billion USD in 2024, and is expected to reach 4.68 billion USD by 2028, growing at a CAGR of 5.67% during the forecast period (2024-2028).

Rising new floor area in the region to drive the demand for adhesives and sealants

- Resins impart the required physical properties and chemical properties such as UV resistance, heat resistance, tensile strength, and others in the adhesives that can be used in specific applications. The new construction area is expected to register a growth of up to 7.4 billion square feet in 2022 from 7.1 billion square feet in 2021.

- The construction adhesives and sealants have shown a sudden growth of 5.8% in terms of volume in 2021. This has happened due to the economic recovery, regular supply of raw materials, and reopening of production facilities in many countries, such as the United States, Canada, and Mexico, which were impacted by the COVID-19 outbreak in 2020 where lockdowns in countries caused a shutdown of production facilities and steady growth of adhesives in North America.

- These adhesives are segmented into different resins in which polyurethane and acrylic resin-based adhesives are widely used in construction applications. These adhesives are known as structural adhesives, which offer high tensile strength in the range of 5 to 8 N/mm2. So that they are used in construction to bond decorative floor coverings and ceramic tiles adhesives, seal metal parts into concrete, bond a door frame into masonry, and many other applications.

- The United States is the highest consumption country of construction adhesives and sealants, accounting for nearly 70% of the North American market because of the rising demand for residential and non-residential construction in the country. The new building constructions in the country will reach 7.1 billion units by 2028 and hence will drive the demand for North American adhesives and sealants in the future.

Rising green initiatives and alternative solutions for conventional buildings to propel the demand for construction adhesives and sealants in the region

- Adhesives and sealants are majorly produced in North America for various construction applications like bonding and sealing joints, the interior and exterior of buildings, and doors and window frame sealing. The production of these construction adhesives and sealants mainly depends on North America's construction output. The new buildings and constructions were expected to reach 7.4 billion square footage in 2022 from 7.1 billion in 2021.

- Production of these adhesives and sealants suddenly increased in 2021 by 49 million tons in volume owing to the economic recovery and the reopening of international borders for trade exchange in the countries that were closed due to the impact of the COVID-19 pandemic in 2020, which caused a shut down of production facilities, supply chain disruptions, and lockdowns in several countries of North America and resulted in a slow growth rate in the same year.

- In North America, the United States accounts for the highest consumption of construction adhesives and sealants. The annual construction industry output in the country amounts to USD 1.4 trillion, contributing 4.2% of the GDP. More than 100 manufacturers in the country, including many multinational companies, are producing these adhesives and sealants to cater to rising demand from the construction industry. It is the fastest-growing country in the region and is expected to record a CAGR of 5.78% during the forecast period 2022-2028.

- The rising number of green buildings in the United States, the wooden housing trend in Canada, and the increasing manufacturing of prefabricated building parts in Mexico are expected to drive the demand for adhesives and sealants in North America.

North America Construction Adhesives & Sealants Market Trends

Government initiatives for infrastructure developments to support the construction industry

- North America is the third largest region in performing construction activities after Asia-Pacific and MENA regions. North America has a GDP of 29,010 USD per capita, with an expected growth rate of 3.6% y-o-y in 2022. The construction industry sector contributes nearly 7% of North America's GDP. The factors affecting the North American construction industry are new investments, residential and non-residential constructions, government policies, and others.

- In 2020, the construction industry faced many challenges due to the impact of the COVID-19 pandemic. The supply of raw materials such as steel, copper, aluminum, stone, and fixtures was shrunk during the year. In the United States, the import of iron and steel was reduced to USD 18.7 billion from USD 24 billion in 2019 due to the lockdowns in many countries across the world.

- The building and construction sector recovered again in 2021 with a growth rate of 5.6% owing to the reopening of international borders for trade exchange, regularized supply chains, and many other factors. Residential construction is increasing in North America. For instance, the number of new housing starts in Canada was 271,880 thousand in 2021, which is 20% more than in 2020.

- In March 2022, the US Department of Transportation (USDOT) announced that the Infrastructure for Rebuilding America (INFRA) program would distribute USD 7.25 billion for FY 2022-2026 to all states and regions to build multimodal freight and highway projects of national or regional significance. These factors will raise the construction activities in the North American region in the future, with a construction output change of 2.7% by 2030.

North America Construction Adhesives & Sealants Industry Overview

The North America Construction Adhesives & Sealants Market is fragmented, with the top five companies occupying 36.96%. The major players in this market are 3M, Henkel AG & Co. KGaA, MAPEI S.p.A., RPM International Inc. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Canada

- 4.2.2 Mexico

- 4.2.3 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Huntsman International LLC

- 6.4.7 Illinois Tool Works Inc.

- 6.4.8 MAPEI S.p.A.

- 6.4.9 RPM International Inc.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms