|

市場調査レポート

商品コード

1685806

イネ種子治療:市場シェア分析、産業動向、成長予測(2025年~2030年)Rice Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イネ種子治療:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

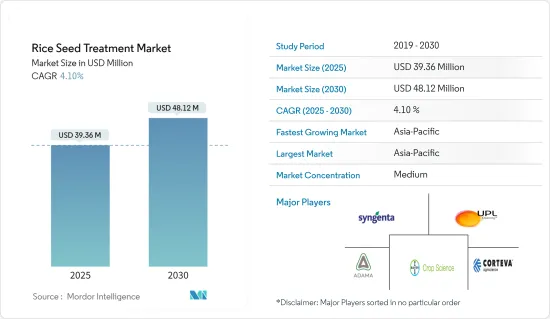

イネ種子治療市場規模は2025年に3,936万米ドルと推計され、2030年には4,812万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは4.10%です。

種子治療は、種子や土壌を媒介とする病気や害虫から種子や苗を保護し、作物の出芽や成長に影響を与えます。稲作農家がこの治療を世界的に採用するには、適切な化学農薬/生物農薬や機器へのアクセス、種子処理方法や処理後の処理手順に関する知識など、効果的な普及戦略が必要です。稲作では、化学種子処理は主に種子の強化と保護のために使用されます。

種子治療は、発芽から作物サイクル全体を通して病害虫から保護する製品を使用し、病害虫のない種子を生産するために世界的に実施されています。米国農務省のデータによると、2023~2024年度のコメ総生産量は5億2,270万トンに達しました。中国がこの生産量の28%を占め、次いでインドが26%、バングラデシュが7%、インドネシアが6%、ベトナムが5%となっています。

米国農務省の報告によると、2024~2025年会計年度の世界のコメ生産量は過去最高の5億3,370万トン(精米ベース)に達し、1,100万トン増加すると予測されています。アルゼンチン、ブラジル、台湾の生産量が上方修正された一方で、オーストラリア、コスタリカ、キューバ、欧州連合、ホンジュラス、ネパール、パナマ、フィリピン、韓国の予想が下方修正されました。2024~2025年度の世界のコメ消費量と残留使用量は5億3,030万トンに達すると予想され、前年度から620万トン増加します。米種子治療市場の成長は、主食としての米消費の増加、高品質種子の採用率の上昇、種子産業における政府の支援、米の病気や害虫の侵入を減らすための種子治療の技術進歩によってもたらされます。

イネ種子治療市場の動向

高品質種子の需要と採用の増加

農家は、良質な種子への高額な投資を保護する方法として、種子治療を認めるようになってきています。望ましい農学的形質を備えた高品質の種子に対する需要の増加により、種子のコストは上昇しています。企業も農家も、高価な高品質の種子を保存するために、種子処理ソリューションに余分な出費をする用意があります。

GM種子の導入は種子に高い付加価値を与え、種子のコストは高く、非GM種子の2倍になることもあります。以前は、種子の一部が腐ったり虫にやられたりするため、農家は85%の成長を見込んでいた。動向が変化し、生産者が不利な条件下でも100%の種子出芽を期待するようになったため、種子治療は必要不可欠なものとなりました。新興国市場の主なプレーヤーは、近代的な育種技術によって優れた品質の種子を開発することに常に注力しており、それによって種子のコストが上昇しています。

市場の主要企業は、近代的育種技術による優れた品質の種子の開発に注力しており、それによって種子コストが上昇しています。発芽不良や虫害による種子の植え替えにはコストがかかります。さらに、必要な労働コストが高いことも、全体的なコストに関連しています。食糧農業機関によると、2022年の穀物の総収量は4,182.4kg/haで、前年の4,152.2kg/haを上回りました。従って、農家は増大する需要を満たすために、限られた収穫面積で収量を高めるために、よく処理された高品質の種子を必要としています。

アフリカ諸国は十分な米を生産しておらず、輸入に頼っています。そのような国のひとつがシエラレオネです。それゆえ、自給自足を目指して、同国政府はいくつかの戦略を採用しています。有望な解決策は、アフリカの新米(ネリカ)のような高収量品種の普及です。ネリカは、アジア米の遺伝的特質(高収量)とアフリカ米の遺伝的特質(干ばつや病気に強い)を兼ね備えているため、アフリカの稲作農家にとって奇跡の作物として知られるようになりました。しかし、現在の推定では、アフリカの農民の2%しかネリカを使用していないです。これは、改良品種のコストが従来のものより40~100%高いためで、貧しい農家がネリカを導入する際の大きな障壁となっています。したがって、こうしたハイブリッド品種はコストが高いため、水田農家には手頃なコストで処理済み種子を使用する機会があります。このことが、今後数年間のイネ種子処理市場のプラス成長につながると予想されます。

アジア太平洋が市場を独占

アジア太平洋は、稲が主要な主食であり、最も栽培されている作物であることに牽引され、2023年にイネ種子処理分野で最大の市場シェアを占めました。中国がこの地域最大の急成長市場に浮上し、インドと日本がこれに続いた。中国は米国に次いで世界第2位の種子市場であり、2021年の年間作付け種子量は1,200万トン、市場価値は190億米ドルです。米国農務省のデータによると、2022年の世界のハイブリッド米種子生産量は16万8,000トンに達し、平均収量は2,160kg/haです。

中国農業省の報告によると、稲の種子産業は、特にいもち病抵抗性に関して、現在の高収量低抵抗性品種の限界に対処するため、差別化された商業品種を優先しています。中国は種子の価値向上に重点を置いているため、ハイブリッド品種の開発が増加しています。コメは依然として中国の主要作物であり、FAOのデータによると、2022年の生産量は2,970万ヘクタールで2億1,000万トンです。同国のコメ生産の拡大と食糧需要の増大は、引き続きイネ種子処理市場の成長を牽引しています。

インドは世界第2位の生産国であり、主要なコメ輸出国でもあります。同国の多様な標高と気候条件は、広範な稲作を支えています。ITC Trade Mapのデータによると、インドは2023年に1,050万トンのコメを輸出し、世界の輸出量の32.5%を占め、世界有数のコメ輸出国となっています。同国の良好な気候と農業慣行が米の生産を増加させ、イネ種子処理剤の需要を強化しています。地域のイネ種子処理市場は、食糧需要の増加と革新的な製品を開発するための継続的な研究開発努力に支えられ、安定した成長を維持すると予測されます。

イネ種子治療産業の概要

イネ種子処理市場は統合されており、2023年には少数の大手企業が市場シェアを独占します。Bayer AG、Syngenta International AG、UPL Limited、Adama Agricultural Solutions Ltd、Corteva Agriscienceが市場で事業を展開する主要企業です。これらの企業は主に新製品の発売、提携、買収に注力しています。研究開発への投資と革新的な製品ポートフォリオの開拓は、市場成長のために不可欠な戦略であり続けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高品質種子の需要の増加と採用

- 作物保護産業における技術開発

- 種子治療に対する政府支援の増加

- 市場抑制要因

- 環境問題の高まり

- 農場レベルでの種子治療における限界

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- ケミカル

- ノンケミカル/バイオ

- 機能

- 種子保護

- 種子強化

- その他の機能

- 用途技術

- 種子コーティング

- 種子ペレット化

- シードドレッシング

- その他の用途技術

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- アフリカ

- 南アフリカ

- その他の地域とアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Adama Agricultural Solutions Ltd

- Yara International ASA

- Bayer AG

- Indofill Industries Limited

- Dhanuka Agritech Limited

- Corteva Agriscience

- Croda International(INCOTEC)

- Crystal Crop Protection Limited

- UPL Limited

- Nufarm Limited

- Syngenta AG

第7章 市場機会と今後の動向

The Rice Seed Treatment Market size is estimated at USD 39.36 million in 2025, and is expected to reach USD 48.12 million by 2030, at a CAGR of 4.10% during the forecast period (2025-2030).

Seed treatment protects seeds and seedlings from seed and soil-borne diseases and insect pests that affect crop emergence and growth. The global adoption of this practice among rice farmers requires effective extension strategies, including access to appropriate chemical pesticides/bio-pesticides and equipment, along with knowledge of seed treatment methods and post-treatment handling procedures. In rice cultivation, chemical seed treatment is primarily used for seed enhancement and protection.

Seed treatment is implemented globally to produce pest and disease-free seeds using products that protect against pests and diseases throughout germination and the crop cycle. According to USDA data, total rice production reached 522.7 million metric tons during MY 2023-2024. China contributed 28% of this production, followed by India at 26%, Bangladesh at 7%, Indonesia at 6%, and Vietnam at 5%.

USDA reports indicate that global rice production for MY 2024-2025 is projected to reach a record 533.7 million metric tons (milled basis), an increase of 11 million metric tons. While Argentina, Brazil, and Taiwan received upward production revisions, forecasts were reduced for Australia, Costa Rica, Cuba, the European Union, Honduras, Nepal, Panama, the Philippines, and South Korea. Global rice consumption and residual use in MY 2024-2025 is anticipated to reach 530.3 million metric tons, increasing by 6.2 million metric tons from the previous year. The rice seed treatment market growth is driven by increasing rice consumption as a staple food, higher adoption of high-quality seeds, government support in the seed industry, and technological advancements in seed treatment for reducing rice diseases and pest infestation.

Rice Seed Treatment Market Trends

Increasing Demand and Adoption of High-Quality Seeds

Farmers are increasingly acknowledging seed treatment as a mode to protect high investments made in good quality seeds. Owing to the increasing demand for high-quality seeds with desirable agronomic traits, the cost of seeds is increasing. Both companies and farmers are ready to spend extra on seed treatment solutions to save costly high-quality seeds.

The introduction of GM seeds added high value to seeds, with the cost of seeds being high and sometimes being twice as much as that of non-GM seeds. Earlier, a growth of 85% was anticipated by farmers as some seeds would rot or be destroyed by insects. With changing trends and 100% seed emergence expectations by growers even in unfavorable conditions, seed treatment has become a necessity. The key players in the market are constantly focusing on developing superior-quality seeds through modern breeding techniques, thereby increasing the cost of the seeds.

Top players in the market are focusing on the development of superior quality seeds through modern breeding techniques, thereby increasing the seed cost. Replanting seeds due to poor germination and insect attack is expensive. Moreover, the high cost of labor requirements is associated with overall cost. According to the Food and Agriculture Organization, the total crop yield of cereals accounted for 4,182.4 kg/ha in 2022, which is higher than the previous year at 4,152.2 kg/ha. Hence to meet the growing demand, farmers need quality seeds that are well-treated to enhance the yield in limited harvested areas.

African countries do not produce enough rice and are reliant on imports. One such country is Sierra Leone. Hence, to become self-sufficient, the country's government is adopting a few strategies. A promising solution is the dissemination of high-yielding rice varieties, such as the New Rice of Africa (NERICA), which have become known as the miracle crop for African rice farmers because they combine the genetic qualities of Asian rice (high yielding) and African rice (high resistance to drought and disease). However, current estimates suggest only 2% of farmers in the country use NERICAs. This is due to the cost of improved varieties that cost 40-100% more than traditional ones, representing a significant barrier to adoption among poor farmers. Hence, due to the high cost of these hybrid varieties, there is an opportunity for paddy farmers to use treated seeds at an affordable cost. This, in turn, is anticipated to lead to the positive growth of the rice seed treatment market in the coming years.

Asia-Pacific Dominates the Market

The Asia-Pacific region held the largest market share in the rice seed treatment sector in 2023, driven by rice being the primary staple food and most cultivated crop. China emerged as the region's largest and fastest-growing market, followed by India and Japan. China represents the world's second-largest seed market after the United States, with an annual seed planting volume of 12 million metric tons and a market value of USD 19 billion in 2021. According to USDA data, global hybrid rice seed production reached 168,000 metric tons in 2022, with an average yield of 2,160 kg/ha.

The Chinese Ministry of Agriculture reports that the rice seed industry is prioritizing differentiated commercial varieties to address the limitations of current high-yield, low-resistance varieties, particularly regarding rice blast resistance. China's emphasis on seed value enhancement has resulted in increased hybrid rice variety development. Rice remains China's primary crop, with FAO data showing production of 210 million metric tons in 2022 across 29.7 million hectares. The country's expanding rice production and growing food demand continue to drive the rice seed treatment market growth.

India maintains its position as the world's second-largest producer and primary rice exporter. The country's diverse altitude and climatic conditions support widespread rice cultivation. ITC Trade Map data indicates that India exported 10.5 million metric tons of rice in 2023, accounting for 32.5% of global export volume and ranking as the world's leading rice exporter. The country's favorable climate and agricultural practices have increased rice production, strengthening the demand for rice seed treatment chemicals. The regional rice seed treatment market is projected to maintain steady growth, supported by increasing food demand and ongoing research and development efforts to develop innovative products.

Rice Seed Treatment Industry Overview

The rice seed treatment market is consolidated, with a few major players dominating the market share in 2023. Bayer AG, Syngenta International AG, UPL Limited, Adama Agricultural Solutions Ltd, and Corteva Agriscience are the key companies operating in the market. These companies primarily focus on new product launches, partnerships, and acquisitions. Investment in research and development and the development of innovative product portfolios remain essential strategies for market growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand And Adoption Of High-Quality Seeds

- 4.2.2 Technological Developments In The Crop Protection Industry

- 4.2.3 Rising Government Support For Seed Treatment

- 4.3 Market Restraints

- 4.3.1 Rising Environmental Concerns

- 4.3.2 Limitations Across Farm-Level Seed Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Chemical

- 5.1.2 Non-chemical/Biological

- 5.2 Function

- 5.2.1 Seed Protection

- 5.2.2 Seed Enhancement

- 5.2.3 Other Functions

- 5.3 Application Techniques

- 5.3.1 Seed Coating

- 5.3.2 Seed Pelleting

- 5.3.3 Seed Dressing

- 5.3.4 Other Application Techniques

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Adama Agricultural Solutions Ltd

- 6.3.2 Yara International ASA

- 6.3.3 Bayer AG

- 6.3.4 Indofill Industries Limited

- 6.3.5 Dhanuka Agritech Limited

- 6.3.6 Corteva Agriscience

- 6.3.7 Croda International (INCOTEC)

- 6.3.8 Crystal Crop Protection Limited

- 6.3.9 UPL Limited

- 6.3.10 Nufarm Limited

- 6.3.11 Syngenta AG