|

市場調査レポート

商品コード

1683166

北米の種子処理市場:市場シェア分析、産業動向、成長予測(2025~2030年)North America Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の種子処理市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 173 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

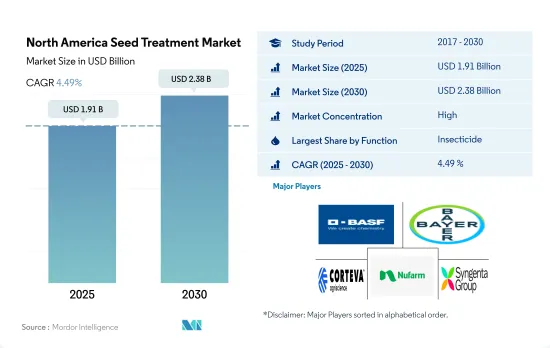

北米の種子処理市場規模は2025年に19億1,000万米ドルと推定・予測され、2030年には23億8,000万米ドルに達し、予測期間(2025~2030年)のCAGRは4.49%で成長すると予測されています。

健全な苗の保護と定着における種子施用技術の利点に対する認識の高まりが市場を後押ししています。

- 北米の種子処理産業は著しい成長を遂げています。市場規模は2020年と比較して2022年には9.8%増加しました。この成長の原動力は、健全な苗の保護と定着における種子施用技術の利点に対する認識の高まりと、全体的な生産性向上の必要性です。

- 米国とカナダは、さまざまな菌類病害や害虫から作物を守るために種子処理剤を広く使用している主要な農業国です。この2カ国は、この地域で種子処理剤の大きな市場シェアを占めています。米国はこの地域の市場額の約82.6%を占め、カナダは市場シェアの約3.7%を占めています。

- 重要な初期生育期間中に、病害虫や不確実な土壌条件に対する先進的保護機能を備えた種子処理製品が入手可能なため、効果が向上し、それが消費を促進し、市場の成長に寄与しています。

- 種子処理市場は、2023~2029年の予測期間中に36.2%の成長が見込まれます。この成長の主要要因は、人口増加のニーズを満たすための食糧生産需要の高まりです。作物の収量を最適化し、病気や害虫による損失を最小限に抑えるため、農業従事者はますます種子処理を採用するようになっており、これは苗の活力と作物全体の生産性を向上させる上で重要な役割を果たしています。

- したがって、種子処理の利点に関する意識の高まり、革新的な製品の利用可能性、種子処理の採用率の上昇は、予測期間中の市場の成長を促進すると予想されます。

農業従事者は作物の健康増進における種子処理の価値を認識するようになっており、これが市場の拡大につながっています。

- 北米の種子処理市場は、農業従事者が作物の健康と生産性の向上における種子処理の価値を認識するようになっているため、種子処理の消費が増加しており、急速に拡大しています。

- 種子処理市場には幅広い作物が含まれます。中でも穀物・穀類は2022年の市場シェアの43.8%を占めています。病害虫の発生率の上昇がこれらの作物に悪影響を及ぼしており、これが穀物・穀類における種子処理剤の採用を促進しています。

- 米国は北米最大の種子処理市場で、2022年には82.6%のシェアを占めます。同国は、食糧安全保障に対する需要の増加や種子処理製品の採用増加といった要因によって大幅な成長を遂げています。

- 同地域の市場額は2017~2022年にかけて30.8%増加しました。サステイナブル農業の推進と食糧増産を目的とした政府の取り組みが、米国とカナダを中心にこの地域の種子処理市場を押し上げました。例えば、国立食糧農業ラボ(NIFA)は、その資金提供イニシアティブを通じて、サステイナブル農業の推進に重要な役割を果たしました。そのひとつが持続可能農業調査・教育(SARE)プログラムで、農業従事者や生産者、農村コミュニティを大きく支援してきました。

- 種子処理剤市場の成長に寄与しているもう一つの要因は、サステイナブル農業プラクティスの拡大です。種子処理は、病害虫に対する標的を絞った保護を提供するため、広範囲な殺虫剤への依存を減らし、環境への影響を最小限に抑えることができます。

- そのため、予測期間中(2023~2029年)の同市場のCAGRは4.8%を記録すると予想されます。

北米の種子処理市場動向

土壌伝染性病害や線虫による主要作物の作物損失の増加により、より高用量の種子処理剤の使用が必要となっています。

- 北米では、1ヘクタール当たりの種子処理剤消費量が顕著に増加し、2017年の数値と比較して2022年には53グラムの増加を記録しました。この消費量の大幅な伸びは、この地域の農業プラクティスに影響を与えたいくつかの要因に起因しています。重要な要因のひとつは気候変動の影響であり、その結果、気象パターンが変化し、農業従事者にとって新たな課題が出現しました。こうした変化の結果として、作物の健康状態や収量に対する予測不可能な天候の悪影響を軽減するための、効果的な種子処理製品に対するニーズが高まっている

- さらに、真菌や線虫の蔓延が農作物にとって大きな脅威となっており、植物の健康を守り、最適な収量を確保するために、より高い散布率で種子処理剤を使用する必要が生じています。

- 種子処理剤の消費量の増加は、北米の農業情勢の変化への対応です。農業従事者は予防措置として種子処理ソリューションを積極的に採用しています。この地域の主要農業国である米国とカナダは現在、植物寄生性線虫、土壌伝染性病害、その他さまざまな害虫がもたらす重大な課題に取り組んでいます。

- 大豆、トウモロコシ、綿花、うもろこしは、この地域で栽培されている主要作物であるが、様々な線虫や土壌伝染性病害による大きな課題に遭遇しています。これらの課題には、根粒線虫、根腐れ病、フザリウム種、穀類シスト線虫、大豆シスト線虫、リゾクトニア、ピシウム種、ホモ病、苗立枯病などが含まれます。これらの病害や線虫による処理が増加しているため、より高用量の種子処理剤が必要とされています。

種子処理に対する需要の高まりは、有効成分の価格を押し上げると予想されます。

- 北米で一般的に利用されている種子処理剤の有効成分には、シペルメトリン、メタラキシル、マラチオン、アバメクチン、アゾキシストロビンなどがあります。種子処理は、種子播種時に防御層を形成することで、種子や幼苗を病害虫から初期保護します。この保護バリアは、種子が土壌中で生育を開始する際に、潜在的な害から種子を保護します。

- 殺虫剤としてのCypermethrinは、主に処理された種子や植物の表面に留まり、幅広い害虫に対する迅速なノックダウン作用のための保護バリアを形成しました。その価格は2022年に1トン当たり2万1,000米ドルとなりました。シペルメトリンの作用機序は昆虫の神経系を混乱させ、麻痺を引き起こし、最終的には死に至らしめる。

- マラチオンの全身作用により、アブラムシ、オオヨコバイ、アザミウマ、ウロコバチ、特定のイモムシなど、幅広い害虫の駆除に成功しました。2022年の価格は1トン当たり12万4,000米ドルでした。マラチオンは昆虫の神経機能に不可欠な酵素であるアセチルコリンエステラーゼを阻害し、昆虫を無力化します。

- アバメクチンはイベルメクチン系に属し、線虫に対して高い固有活性を持っています。トウモロコシ、大豆、綿花の生産において、根を攻撃する線虫から若い植物を守るために使用されます。2022年の価格はトン当たり8,800米ドルです。

- メタラキシルを種子処理剤として散布することで、農業従事者は植物のライフサイクルの最初から、病害の問題に積極的に対処することができます。この早期介入は、より健全で活力ある苗立ちを確実にし、作物収量の向上につながります。Metalaxylの2022年の価格はトン当たり4,400米ドルでした。

北米の種子処理産業概要

北米の種子処理市場はかなり統合されており、上位5社で76.44%を占めています。この市場の主要企業は、BASF SE、Bayer AG、Corteva Agriscience、Nufarm Ltd、Syngenta Groupです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 殺虫剤

- 殺線虫剤

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Albaugh LLC

- BASF SE

- Bayer AG

- Corteva Agriscience

- Nufarm Ltd

- Sharda Cropchem Limited

- Syngenta Group

- Upl Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 56637

The North America Seed Treatment Market size is estimated at 1.91 billion USD in 2025, and is expected to reach 2.38 billion USD by 2030, growing at a CAGR of 4.49% during the forecast period (2025-2030).

The market is fueled by increasing awareness of the benefits of seed-applied technologies in protecting and establishing healthy seedlings

- The seed treatment industry in North America is experiencing significant growth. The market value increased by 9.8% in 2022 compared to 2020. This growth is driven by growing awareness of the benefits of seed-applied technologies in protecting and establishing healthy seedlings and the need to improve overall productivity.

- The United States and Canada are leading agricultural nations that extensively use seed treatment chemicals to safeguard their crops against various fungal diseases and pests. These two countries hold a significant market share for seed treatments in the region. The United States constitutes approximately 82.6% of the regional market value, while Canada contributes around 3.7% of the market share.

- The availability of seed treatment products with advanced protection against pests, disease, and uncertain soil conditions during the critical early growth period results in improved effectiveness, which drives consumption, thereby contributing to the growth of the market.

- The seed treatment market is expected to witness a growth of 36.2% during the forecast period of 2023-2029. This growth is primarily driven by the rising demand for food production to meet the needs of a growing population. In order to optimize crop yields and minimize losses due to diseases and pests, farmers are increasingly adopting seed treatment, which plays a crucial role in improving seedling vigor and overall crop productivity.

- Therefore, growing awareness about the benefits of seed treatment, the availability of innovative products, and the rising adoption rate of seed treatment are expected to fuel the growth of the market during the forecast period.

Farmers are increasingly recognizing the value of seed treatments in improving crop health, which is leading to the expansion of the market

- The North American seed treatment market is expanding rapidly due to the rising consumption of seed treatment as farmers increasingly recognize the value of seed treatments in improving crop health and productivity.

- The seed treatment market includes a wide range of crops. Among all, grains and cereals accounted for 43.8% of market share in 2022. The rising incidence of pests and diseases is negatively affecting these crops, which is driving the adoption of seed treatments in grains and cereals.

- The United States is the largest seed treatment market in North America, accounting for a share of 82.6% in 2022. The country has been witnessing substantial growth driven by factors such as increasing demand for food security and rising adoption of seed treatment products.

- The market value increased in the region by 30.8% between 2017 and 2022. Government initiatives aimed at promoting sustainable agriculture and increasing food production boosted the seed treatment market in the region, mainly in the United States and Canada. For instance, the National Institute of Food and Agriculture (NIFA), through its funding initiatives, played a crucial role in advancing sustainable agriculture. One such program is the Sustainable Agriculture Research and Education (SARE) program, which has significantly supported farmers, growers, and rural communities.

- Another factor contributing to the growth of the seed treatment market is the growing sustainable agricultural practices. Seed treatments offer targeted protection against pests and diseases, reducing the reliance on broad-spectrum pesticides and minimizing the environmental impact.

- Therefore, the market is expected to register a CAGR of 4.8% during the forecast period (2023-2029).

North America Seed Treatment Market Trends

Increased crop losses in major crops due to soilborne diseases and nematodes necessitate the use of seed treatments with higher dosages

- North America experienced a noteworthy upsurge in seed treatment consumption per hectare, with a recorded increase of 53 grams in 2022 compared to the figures from 2017. This substantial growth in consumption can be attributed to several factors that have influenced agricultural practices in the region. One significant factor is the impact of climate changes, which have resulted in shifts in weather patterns and the emergence of new challenges for farmers. As a consequence of these changes, there has been a greater need for effective seed treatment products to mitigate the adverse effects of unpredictable weather on crop health and yield.

- Additionally, the rise in fungal and nematode infestations has posed significant threats to crops, necessitating the use of seed treatments at higher application rates to safeguard plant health and ensure optimal yields.

- The increase in seed treatment consumption is a response to the changing agricultural landscape in North America. Farmers are proactively adopting seed treatment solutions as a precautionary measure. The United States and Canada, as major agricultural countries in the region, are currently grappling with significant challenges posed by plant parasitic nematodes, soil-borne diseases, and various other insect pests.

- Soybeans, maize, cotton, and corn are the prominent crops grown in the region, but they encounter significant challenges from various nematodes and soilborne diseases. These challenges include root-lesion nematodes, root rots, fusarium species, cereal cyst nematodes, soybean cyst nematodes, rhizoctonia, pythium species, phomosis, seedling blights, and others. The increasing damage by these diseases and nematodes necessitates the seed treatment application method with higher dosages.

The growing demand for Seed treatment is anticipated to fuel the prices of the active ingredients.

- In North America, commonly utilized active ingredients for seed treatment chemicals include cypermethrin, metalaxyl, malathion, abamectin, and azoxystrobin. Seed treatment offers initial protection to seeds and young plants from pests and diseases by establishing a defensive layer upon seed sowing. This protective barrier shields the seed from potential harm as it begins its growth in the soil.

- Cypermethrin, as an insecticide, remained primarily on the surface of treated seeds or plants, forming a protective barrier for quick knockdown action against a wide range of insect pests. Its price stood at USD 21.0 thousand per metric ton in 2022. The mode of action of Cypermethrin involves disrupting the nervous systems of insects, leading to paralysis and, ultimately, their death.

- Malathion's systemic effect allowed for the successful management of a wide range of insect pests, such as aphids, leafhoppers, thrips, scales, and specific caterpillar types. It was priced at USD 124 thousand per metric ton in 2022. Malathion inhibits acetylcholinesterase, a vital enzyme for nerve function in insects, leading to their incapacitation.

- Abamectin belongs to the Ivermectin chemical class and has high intrinsic activity against nematodes. It is used to protect young plants from the root-attacking nematodes in corn, soybeans, and cotton production. It was priced at USD 8.8 thousand per metric ton in 2022.

- By applying metalaxyl as a seed treatment, farmers can proactively address disease issues right from the start of the plant's life cycle. This early intervention helps ensure healthier and more vigorous seedling establishment, which can lead to improved crop yields. Metalaxyl was priced at USD 4.4 thousand per metric ton in 2022.

North America Seed Treatment Industry Overview

The North America Seed Treatment Market is fairly consolidated, with the top five companies occupying 76.44%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Albaugh LLC

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Nufarm Ltd

- 6.4.6 Sharda Cropchem Limited

- 6.4.7 Syngenta Group

- 6.4.8 Upl Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms