|

市場調査レポート

商品コード

1685833

種子治療:市場シェア分析、産業動向、成長予測(2025年~2030年)Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 種子治療:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 319 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

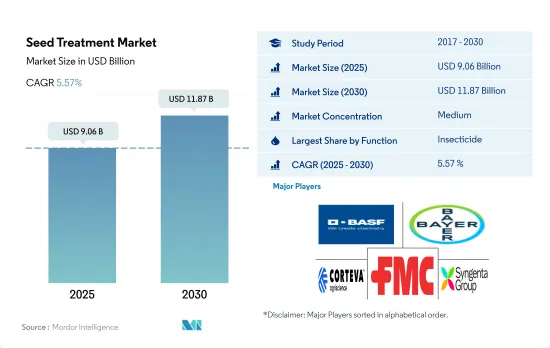

種子治療市場規模は2025年に90億6,000万米ドルと推定され、2030年には118億7,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは5.57%で成長する見込みです。

農家の意識の高まりが種子治療需要を牽引

- 2017年から2022年の間に、世界の化学殺菌剤種子処理市場は18.3%の大幅な成長を示しました。いもち病のような真菌病は、最大30%の世界の米の収量損失と深刻な経済的損害を引き起こします。これらの損失を減らすことを目的とした治療は、より高い殺菌性種子処理剤の必要性を増加させました。殺菌性種子処理剤の有効成分としては、メタラキシル、カルベンダジム、チラム、キャプタンが最も多く使用されています。

- 殺虫性種子処理剤は、アブラムシ、アザミウマ、ヨトウムシ、カイガラムシなど、作物のライフサイクルの初期段階で種子や苗を加害するさまざまな害虫を駆除する上で、高い標的特異性を有しています。さらに、殺虫性種子治療は散布量が少なくて済むため費用対効果が高く、ごく初期の段階で適切な予防措置を講じることで、作物の後期段階における葉面散布への依存度を下げることができます。これらの要因により、予測期間中(2023年~2029年)のCAGRは4.5%で市場を牽引すると予想されます。

- イミダクロプリド、クロチアニジン、チアメトキサム、フィプロニル、クロルピリホスなどの有効成分は、化学殺虫剤種子処理において非常に重要です。イミダクロプリド、クロチアニジン、チアメトキサムはアブラムシ、コナジラミ、ヨコバイなどの幅広い吸汁害虫に効果があり、フィプロニルやクロルピリホスは土壌棲息害虫に作用します。

- 線虫の蔓延は世界的に増加しており、農作物に深刻な損失をもたらしています。収量減を克服するためのさまざまな代替手段に関する農家の知識が広まったことで、過去期間中に4.6%の大幅な伸びを示しました。

種子治療は、干ばつや熱波に対する植物の生物的ストレス耐性を向上させる。

- 収穫前の段階で初期の作物の病気や害虫から種子や苗を保護する必要性に関する農家の意識の高まりは、種子処理製品の利用を高め、作物が均一な定着と成長でさらに成長する力を与えます。世界の種子処理市場は80億5,000万米ドルを占め、2022年の消費量は75万6,700トンです。

- 2022年には、南米が世界種子処理市場の26.3%を占める第2位の市場であり、市場価値は21億2,000万米ドルです。南米地域の優位性は、主に気候条件の変化に起因しています。近年の干ばつや熱波は作物生産を妨げています。種子治療は、干ばつや熱波のような悪条件に対する植物の耐性を高め、より高い利用率をもたらします。2022年、ブラジルは南米最大の市場として圧倒的な地位を占め、同地域の市場シェアの77.9%を占めました。同国の目覚ましい拡大は、食糧安全保障に対するニーズの高まりや、大豆などの作物における種子処理製品の利用拡大など、いくつかの要因によるものです。

- 北米の種子処理市場は20.8%を占め、2022年の市場価値は16億7,000万米ドルです。米国は最大の種子処理市場で、2022年には82.6%のシェアを占める。同国は、食糧安全保障に対する需要の増加と、種子処理によって播種率を下げ収益性を高めることができるため、大豆のような主要な栽培作物で種子処理製品の採用が増加していることを背景に、大幅な成長を遂げています。

世界の種子治療市場動向

作物サイクルの初期における真菌の蔓延の増加と、これらの問題に対処するための殺菌剤処理の有効性により、殺菌剤種子処理剤の需要が増加する可能性があります。

- 2022年の種子処理剤の世界平均消費量は、農地1ヘクタール当たり3.4kgと記録されました。種子処理剤の使用量は、作物保護における種子処理の重要性に対する世界の農家の意識の高まりとともに増加しています。

- 殺菌性種子処理剤の使用は、いもち病などの真菌性病害がもたらす大きな脅威のため、あらゆる農薬の中でも人気が高く、世界的に大幅な収量損失をもたらしています。これらの病害は、6,000万人分の食糧に相当するコメの生産量に最大30%の損失をもたらし、深刻な経済的損害をもたらします。トリシクラゾール75 WPを3g/kgで種子処理することで、この種子を媒介とする病害を後期段階でも効果的に予防・防除できます。

- イミダクロプリド、クロチアニジン、チアメトキサム、フィプロニル、クロルピリホスは種子処理用化学殺虫剤の重要な有効成分です。ワイヤワーム、種角ウジ虫、グラブ、土壌棲息昆虫、イモムシ、カミキリムシなど、幅広い害虫に対して高い効果を示します。

- 南米は2022年に農地1ヘクタール当たり1,959グラムを消費し、種子処理剤のヘクタール当たり消費量が最も多く、次いで欧州が同619.0グラム、北米が同583.0グラムです。

- 調査によれば、イネ種子に殺虫剤を散布することで、イネミズゾウムシの幼虫数を効果的に減少させることができました。これらの治療は90%を超える防除効率を示し、南米では最大25%の大幅な収量向上をもたらしました。このような要因から、この地域および世界的に種子治療の導入が進んでいます。

メタラキシルを種子治療に使用すると、土壌伝染性病原体から種子と苗を早期に保護することができます。

- 種子治療は、種子に直接塗布する特殊な化学薬品で、病害虫からの保護を強化し、発芽率を向上させ、植物の健全な生育を確保することで、作物の生産性向上と持続可能な農法に貢献します。

- 非全身殺虫剤であるシペルメトリンは、主に処理した種子や植物の表面に残ります。ターゲット害虫と接触することで、保護バリアを形成します。シペルメトリンは広範な害虫に対する迅速なノックダウン効果で知られ、種子処理用途で重宝されています。2022年の価格は1トン当たり2万1,100米ドルでした。

- マラチオンの全身作用により、植物のさまざまな部位を食害する害虫を防除できます。アブラムシ、オオヨコバイ、アザミウマ、鱗翅目、特定の青虫など、処理した作物に侵入する可能性のあるさまざまな害虫駆除に効果的です。マラチオンの2022年の価格はトン当たり1万2,500米ドルでした。

- メタラキシルを使用すると、種子や苗を土壌伝染性病原体から早期に保護し、立枯病や種子の腐敗といった病気を防ぐことができます。ピシウム、フィトフトラ、べと病などの病原菌に効果があります。2022年の価格はトン当たり4,400米ドル。

- アゾキシストロビンの全身活性により、処理された植物に吸収され、維管束系内に移行し、新芽や葉を含む植物のさまざまな部分に拡大した保護を提供します。2022年の価格はトン当たり4,500米ドル。

- 世界各国の政府は、種子処理の採用を促進するために、普及サービス、補助金、啓発キャンペーン、業界内の協力を通じて、種子処理の実践を推進しています。

種子治療業界の概要

種子治療市場は適度に統合されており、上位5社で61.96%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- チリ

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- メキシコ

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- ウクライナ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 殺虫剤

- 殺線虫剤

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他の南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- Mitsui & Co. Ltd(Certis Belchim)

- Nufarm Ltd

- Syngenta Group

- Upl Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 48283

The Seed Treatment Market size is estimated at 9.06 billion USD in 2025, and is expected to reach 11.87 billion USD by 2030, growing at a CAGR of 5.57% during the forecast period (2025-2030).

Growing awareness among farmers is driving the demand for seed treatments

- During 2017-2022, the global chemical fungicide seed treatment market witnessed a substantial growth of 18.3%. Fungal diseases like rice blast cause up to 30% global rice yield loss and severe economic damage. The aim to reduce these losses increased the need for higher fungicidal seed treatments. Metalaxyl, carbendazim, thiram, and captan are the most used active ingredients in fungicidal seed treatment products.

- Insecticidal seed treatments have high target specificity in controlling a range of pests that attack seeds or seedlings, such as aphids, thrips, wireworms, and beetles at the initial stage of the crop's life cycle. Moreover, insecticidal seed treatments are cost-effective alternatives as they require low application rates and can help reduce the reliance on foliar sprays in the later stages of the crop by providing proper preventive measures at the very initial stages. These factors are expected to drive the market at a CAGR of 4.5% during the forecast period (2023-2029).

- Active ingredients such as imidacloprid, clothianidin, thiamethoxam, fipronil, and chlorpyrifos are highly important in chemical insecticide seed treatment. Imidacloprid, clothianidin, and thiamethoxam are effective against a wide range of sucking insects, such as aphids, whiteflies, and leafhoppers, while fipronil and chlorpyrifos act against soil-dwelling insect pests.

- There is an increasing incidence of nematode infestations globally with severe crop losses. The growing knowledge among farmers about the various alternatives to overcome yield losses led to a significant growth of 4.6% during the historical period.

Seed treatment improves the plant abiotic stress tolerance towards droughts and heatwaves.

- The growing awareness among farmers regarding the need to protect seeds and seedlings from early crop diseases and insect pests in the preharvest stage raises the utilization of seed treatment products, which will give more strength to the crop to grow further with uniform establishment and growth. The global seed treatment market accounted for USD 8.05 billion, with a consumption volume of 756.7 thousand metric tons in 2022.

- In 2022, South America is the second largest market with 26.3% of the global seed treatment, with a market value of USD 2.12 billion. The dominance of the South American region is majorly attributed to the changing climatic conditions. Recent droughts and heat waves have hampered crop production. Seed treatment increases the plant's tolerance to adverse conditions like drought and heatwaves, resulting in higher utilization. In 2022, Brazil held the dominant position as the largest market in South America, representing 77.9% of the region's market share. The country's remarkable expansion can be attributed to several factors, including the growing need for food security and the escalating utilization of seed treatment products in crops like soybeans.

- The North America seed treatment market holds a 20.8% and a market value of USD 1.67 billion in 2022. The United States is the largest seed treatment market, accounting for a share of 82.6% in 2022. The country has been witnessing substantial growth driven by increasing demand for food security and rising adoption of seed treatment products in major grown crops like soybeans, as seed treatment can reduce the seeding rate and increase profitability.

Global Seed Treatment Market Trends

Growing fungal infestations in early crop cycle and effectiveness of fungicide treatment in addressing these issues may lead to a rise in the demand for fungicide seed treatments

- The global average consumption of seed treatment chemicals was recorded at 3.4 kg per hectare of agricultural land in 2022. The usage of seed treatment chemicals is growing with the rising awareness among farmers globally about the significance of seed treatment in crop protection.

- The usage of fungicidal seed treatments is more popular among all pesticides due to the significant threat posed by fungal diseases such as rice blasts, leading to substantial yield losses globally. These diseases can result in up to a 30% loss in rice production, equivalent to feeding 60 million people, causing severe economic damage. Treating seeds with tricyclazole 75 WP at 3g/kg effectively prevents and controls this seed-borne disease even in later stages.

- Imidacloprid, clothianidin, thiamethoxam, fipronil, and chlorpyrifos are crucial active ingredients in chemical insecticides for seed treatment. They exhibit high efficacy against a broad spectrum of pests, including wireworms, seed-corn maggots, grubs, soil-dwelling insects, caterpillars, and beetles.

- South America is the highest per-hectare consumer of seed treatment chemicals, with 1,959 grams per hectare of agricultural land in 2022, followed by Europe and North America, with consumption of 619.0 and 583.0 grams per hectare of seed treatment chemicals, respectively, in the same year.

- Research indicates that the application of insecticides on rice seeds effectively reduced the larval population of rice water weevil. These treatments displayed control efficiency surpassing 90% and resulted in significant yield improvements of up to 25% in South America. Such factors are leading to higher adoption of seed treatments in the region and globally.

Metalaxyl, when used as seed treatment, offers early protection to seeds and seedlings from soil-borne pathogens

- Seed treatments are specialized chemicals applied directly to seeds, offering enhanced protection from pests and diseases, promoting better germination rates, and ensuring healthier plant establishment, contributing to increased crop productivity and sustainable farming practices.

- As a non-systemic insecticide, cypermethrin remains primarily on the surface of treated seeds or plants. It forms a protective barrier that acts in contact with the target pests. Cypermethrin is known for its quick knockdown effect on a wide range of insect pests, making it valuable in seed treatment applications. In 2022, it was priced at USD 21.1 thousand per metric ton.

- Malathion's systemic action enables it to provide protection against pests that feed on different parts of the plant. It is effective in controlling a variety of insect pests, such as aphids, leafhoppers, thrips, scales, and certain caterpillar species that may infest the treated crops. Malathion was priced at USD 12.5 thousand per metric ton in 2022.

- Metalaxyl, when used, offers early protection to seeds and seedlings from soil-borne pathogens, preventing diseases like damping-off and seed rot. It is effective against pathogens such as pythium, phytophthora, and certain downy mildew. In 2022, it was priced at USD 4.4 thousand per metric ton.

- Azoxystrobin's systemic activity allows it to be absorbed by treated plants and translocated within their vascular system, providing extended protection to different parts of the plant, including new growth and foliage. It was priced at USD 4.5 thousand per metric ton in 2022.

- Governments worldwide are promoting seed treatment practices through extension services, subsidies, awareness campaigns, and collaborations within the industry to encourage the adoption of seed treatments.

Seed Treatment Industry Overview

The Seed Treatment Market is moderately consolidated, with the top five companies occupying 61.96%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Crystal Crop Protection Ltd

- 6.4.6 FMC Corporation

- 6.4.7 Mitsui & Co. Ltd (Certis Belchim)

- 6.4.8 Nufarm Ltd

- 6.4.9 Syngenta Group

- 6.4.10 Upl Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms